·

·

What’s A Life Insurance Broker?

Getting life insurance is easier with the help of a life insurance broker!

13 minute read

Originally published: August 2, 2022

Updated: June 14, 2023

What’s A Life Insurance Broker?

Getting life insurance is easier with the help of a life insurance broker!

12 minute read

Originally published: August 2, 2022

Updated: June 14, 2023

When shopping for life insurance, you might be wondering: “What’s a life insurance broker?” There are many reasons why working with a life insurance broker is more beneficial than working with a captive life insurance agent. There are also many things you need to know about life insurance brokers as they offer completely free services and they must be licensed to sell insurance in Canada. This blog will explain what you need to know about life insurance brokers, why you should work with life insurance, how a life insurance broker gets paid, what a life insurance broker is, how working with a life insurance broker is beneficial, and more!

In this article:

- The basics of buying life insurance

- What is a life insurance broker?

- What kinds of life insurance can life insurance brokers help you purchase?

- Life insurance broker vs Captive life insurance agent

- How do life insurance brokers get paid?

- Why you should work with a life insurance broker

- Frequently Asked Questions (FAQs) about life insurance brokers

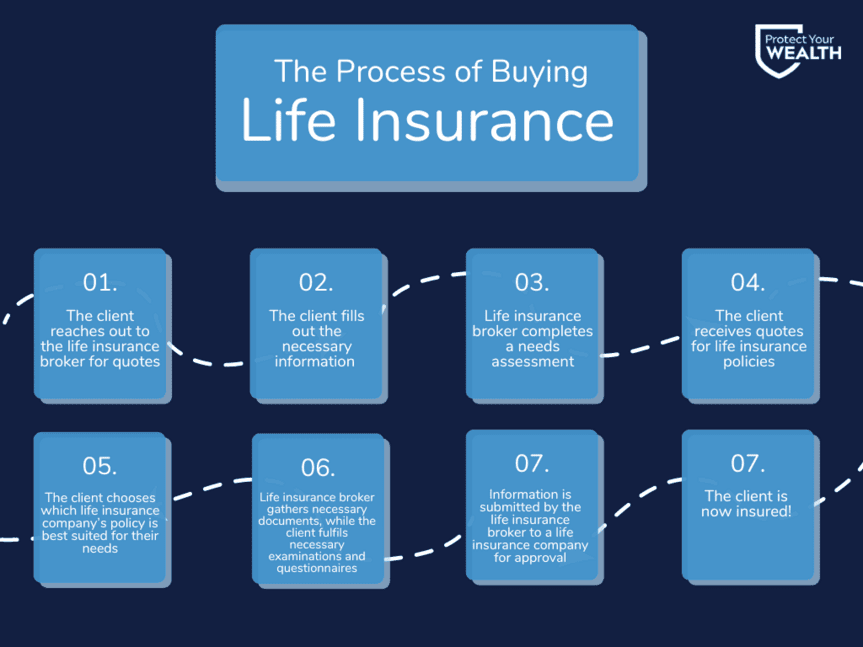

The basics of buying life insurance

Buying life insurance does not have to be a stressful ordeal, rather it can be very simple if you choose to work with experienced life insurance brokers. Basically, the process of finding life insurance with a broker goes like this:

- The client reaches out to the life insurance broker for quotes

- The client fills out the necessary information

- Life insurance broker completes a needs assessment

- The client receives quotes for life insurance policies from various companies

- The client chooses which life insurance company’s policy is best suited for their needs with the help of the life insurance broker

- Life insurance broker gathers necessary documents, while the client fulfils necessary examinations and questionnaires (eg: attending physician statements, health history, criminal record checks etc)

- Information is submitted by the life insurance broker to a life insurance company for approval

- The client is now insured!

This process sounds simple but can be difficult if a life insurance expert isn’t available to help you through these processes. A life insurance broker is knowledgeable about all the steps that are needed and, thus they can assist you in case of any hiccups on the road to getting your life insurance policy. A life insurance broker can also do a needs assessment which will find out how much life insurance coverage you need, what needs are necessary in your life insurance policy (riders), how much life insurance you are capable of affording, and what needs you require in your life insurance policy.

What is a life insurance broker?

A life insurance broker is a licensed professional with a focus on selling life insurance policies from various insurance companies. A life insurance broker represents several insurance companies, giving them more options to find you the most suitable coverage. In contrast, a captive agent only sells insurance from one company, thus having a limited amount of life insurance options you can choose from. A life insurance broker is someone who is also much more concerned with your best interests in mind rather than just making a sale. Since life insurance brokers are independent, they do not have to worry about appealing to a specific company. They also require legal contracts such as the LIRD form, and must be licensed in Canada, which means that they must work in your favour. Working with a life insurance broker is important also because of the fact that there are life insurance scams in Canada, so for your own safety, it is wise to work with a licensed life insurance advisor.

What kinds of insurance can life insurance brokers help you purchase?

A licensed life insurance broker can help you purchase several forms of insurance. Being that they are your friendly insurance experts, they can help you purchase any type of product that you’re looking for such as term life insurance, permanent life insurance, simplified life insurance, no-medical life insurance, critical illness insurance, disability insurance, mortgage insurance, senior life insurance and more.

We have the capability to help each step of the way if you are new to getting life insurance coverage or if you already have life insurance coverage and want to buy another insurance product. This being said, here is a description of the different kinds of insurance that we can help you purchase:

Term life insurance

Term life insurance is a type of life insurance that pays out to your beneficiaries if you die during the term of your policy. You can specify how long your term policy will last. Insurance companies provide term life insurance for Canadians and those legally residing in Canada for 10, 15, 20, 25 or 30 years, and some offer other term lengths. Once the term expires, you will be able to renew your policy, but there will be an increase in the premiums you pay.

To give an example of a term life policy in action: if you purchase a 10-year term life insurance policy and you die during those ten years, the people you name as your beneficiaries will receive a tax-free payment (also called a death benefit).

Permanent life insurance

Permanent life insurance is also known as whole life insurance because it covers you for the rest of your life. It also provides your beneficiaries with a tax-free payment after your death. Some plans have the ability to accumulate cash value over time. Permanent insurance costs are typically guaranteed not to rise from the time the policy is purchased. Furthermore, some permanent insurance plans allow you to pay for a limited period of time and then never again. Certain types of permanent life insurance include universal life and participating life.

Guaranteed issues/No-medical life insurance

These plans don’t ask any questions and don’t require any medical exams. Guaranteed issue insurance or no-medical insurance which is intended for people with serious health problems or who are older and do not qualify for underwritten or simplified insurance. Many insurers will also require a 24-month deferral period for guaranteed life acceptance insurance, meaning if you pass away during the first 24 months, your beneficiaries will only receive the premiums you paid and not the entire death benefit. Because it is also a type of permanent life insurance, guaranteed issue insurance coverage generally has a maximum of $50,000, with some insurers covering less, and has the highest premium of the three.

Simplified life insurance

Simplified life insurance is offered in permanent life and term life insurance forms. A medical exam is not required for simplified issue insurance policies, but you must answer certain health-related questions as part of your application. In return for no medical exam, premiums tend to be higher than traditional insurance. The number of questions asked varies by insurer and also by whether or not the policy is deferred. Simplified issue insurance is typically used for term life insurance products and is an option for those who want faster approval or do not want to take a medical exam. With simplified plans, you’ll have smaller coverage amount options and higher monthly premiums than traditional fully underwritten plans.

Mortgage insurance

Your family’s biggest investment is likely your home, which should be protected by mortgage insurance. Mortgage insurance is a type of protection that, in the event of your passing, could pay out all or a certain portion of your mortgage’s principal to up to 8 beneficiaries. This insurance, which includes options for serious illness or disability, is provided by a number of insurers and is occasionally included by your financial institution as part of your mortgage.

Critical illness insurance

Critical Illness Insurance will provide a predetermined lump sum payment if you are found to have a serious illness. You have the freedom to use that lump sum payout however you see fit to help you get by while you’re sick, whether that be for medical costs, non-medical expenses like lost income, travel/transportation costs, etc., recovery therapies, and more. The specifics of your policy’s coverage will be outlined in your personalized contract; examples include cancer, heart attack, stroke, and more.

Disability insurance

The financial and psychological effects of your loss of income can be significant while you’re recuperating from a severe illness or injury, being hospitalized, or dealing with a mental illness. Disability insurance is there to make this challenging time easier for you by providing you with a monthly payment to put toward your recovery and monthly expenses. This will free up your attention to concentrate on what’s most crucial—your health. In the event of a disability or death, disability insurance offers financial security for you and your family. It is

significantly less expensive than whole life insurance plans. Flexible policy terms that can be tailored to your needs and your rates won’t alter once you’ve locked in your policy. A death benefit that is assured and peace of mind knowing your family is safe.

Senior life insurance

Senior life insurance protects your loved ones because you can stop them from inheriting your outstanding debt (such as your mortgage, rent, credit cards, or outstanding loans). Funeral expenses can be paid for, relieving your loved ones of this burden during their difficult time. Even if your family members are not financially dependent on you, there are still things you can do to ease their burdens, like paying your grandchildren’s tuition.

Life Insurance Broker vs Captive Life Insurance Agent

Life insurance brokers are experts who act as the client’s advocate and look for the best available coverage based on the client’s requirements. They’ll work closely with their clients as they look into the best options for coverage and go through the quoting procedure. Life insurance brokers are more concerned with keeping the customer happy by fulfilling their specific needs for their policies. Brokers can assist in the search for a policy with the lowest insurance premiums while captive insurance agents frequently act in the best interests of the company that employs them.

Brokers don’t have the power to specifically change items in your life insurance coverage because they are not employed by the insurer. When you buy insurance through a broker, they can provide you with expert guidance while you look for insurance quotes. Brokers can assist you in determining an ideal price range and taking into account the options that apply to your policy.

On the other hand, a captive insurance agent directly sells the insurance products of one company to customers. They assist people in choosing the best insurance plan to purchase from the insurance provider that they work for. While independent insurance agents represent various insurance companies, captive agents typically only represent one. Since captive life insurance agents are restricted to the company they work for, insurance agents typically don’t provide as many options as brokers.

How do life insurance brokers get paid?

To keep it simple, life insurance brokers work for commission and they receive the commission from the life insurance company that their clients purchase a policy. Our life insurance brokers work for you and when you purchase a life insurance policy from us, we are paid commission directly from the life insurance company, with no cost to you.

For the same kinds of products, various insurance companies offer brokers commissions that are essentially the same. Since insurance brokers receive a commission for their work, they have an incentive to find you the best policy. Each carrier determines a different percentage that the insurer pays brokers.

The broker you’re working with might need to reimburse the insurance company for the commission they’ve received if you decide to cancel your policy. Because of this, the majority of brokers are concerned with finding you the best policy for your requirements so that you keep the coverage throughout your term. Many life insurance brokers provide their services to you for free (as they are compensated directly by the insurance company). Their complimentary services include initial consultations, quotes, and assistance through the process of getting life insurance coverage, and service after the policy has been put in force.

Why you should work with a life insurance broker

There are many reasons why working with a life insurance broker is a better choice than working with a captive life insurance agent. There is a list of things that make a life insurance broker stand out in comparison to a life insurance agent: brokers can give you insight into various options, fair and unbiased advice, free expert services, time saving service and more.

Get access to various options

Shopping around for life insurance can be extremely tedious if you don’t contact a life insurance broker. A life insurance broker who works with many companies will have access to the various options that you have available to you. If you wanted to do this yourself, you would have to call each life insurance company and get a quote from them, but a life insurance broker can give you all the information you need right away so you can figure out which company is better than the broker will help you figure out what is the best deal for you.

Fair and unbiased advice

A life insurance broker is not swayed by one company or another, they get paid on a commission basis and will not get paid if you end up cancelling your policy. This being said, they are highly dedicated to helping you find a life insurance policy that you will want to stick with. They are legally bound to provide you with information based on your best interest, thus they are not driven solely off of the pressures from a specific life insurance company.

Free expert services

Life insurance agents typically provide their services to you for free, which means you can get the free advice and services of licensed life insurance brokers who are well aware of the several intricacies of life insurance. Here at Protect Your Wealth, our services are completely free from your first consultation all the way until you sign off on your new life insurance policy, thus we do not charge whatsoever for our services.

Time saving services

As explained earlier, life insurance brokers have access to several different life insurance policies from several different life insurance companies. Going with a life insurance broker can end up saving you precious time, as the process of looking for life insurance by yourself can be very time consuming if you have to call each insurance company one by one and sift through the various policies that life insurance companies offer.

Licensed professionals

Working with a licensed professional can give you the peace of mind that you are working with someone who is a legitimate life insurance broker and someone who has your best interest in mind. There are many life insurance and insurance scams in Canada, so it is smart to work with a licensed life insurance broker so that you know your personal information and important documents are being handled by a professional. The best resource that is available in this tool is to find licensed agents in Ontario created by the Financial Services Regulatory Authority of Ontario. All you will need is either the last name of the life insurance agent, their city or town or their license number.

Lifetime support

Life insurance agents who are captive might contact you to review your policy every once in a while but it will usually just be a basic review. On the other hand, a life insurance broker will be there for you throughout the years, as it is common that a life insurance broker will help you if anything new comes up in your life. You can rely on a life insurance broker to help you make decisions or they will even help you with figuring out how your life insurance can play a role in every milestone in life such as: having a child, getting married, buying a home or starting a business. Not only that, but our life insurance brokers are also well versed in giving you financial advice, so if you are interested in investing through a TFSA, RESP, RRSP or a LIRA, we have got you covered!

Frequently Asked Questions (FAQs) about life insurance brokers

Life insurance brokers are simply better to work with than a captive life insurance agent because:

- Life insurance brokers can give you multiple options because they have access to multiple life insurance policies from various life insurance companies

- Life insurance brokers can make the process of purchasing life insurance fast and easy

- Life insurance brokers are indeed licensed to sell life insurance

- Life insurance brokers are unbiased because they are not loyal to one life insurance company

- Life insurance brokers can give you other financial advice such as how to save on your life insurance, how to invest, and how plan for retirement

To keep it simple, life insurance brokers work for commission and they receive the commission from the life insurance company that their clients purchase a policy from. Our life insurance brokers work for free and when you purchase a life insurance policy from them, they get some commission from the life insurance company because of the fact that they provided a client for the life insurance company.

You can get all sorts of insurance from a licensed life insurance broker including:

Yes, a life insurance broker can save you money. Although a life insurance broker does not work as an employ of a life insurance company and they cannot change the prices of your life insurance policy, they can give you great information that will save you money. Consider this, a life insurance broker is in expert in the world of life insurance, they can give you really great information such as when to buy insurance so that you save money, or how to save money when making payments for you life insurance policy. A life insurance broker can reveal several different life insurance policy options from several life insurance companies when you are in the of buying life insurance. This is especially helpful because they can curate these policies based on your needs assessment. This is also helpful because they can find the best rates for you very quickly, instead of you calling each company one by one.

Yes, seniors can definitely purchase life insurance in Canada. There are awesome term life insurance policies as well as whole life policies that are out there that can provide coverage for seniors 60 years and older. Read all about it here: Ultimate Guide to Life Insurance for Seniors in Canada.

There are so many reasons for you to get life insurance, the main being that it will protect your loved ones from any financial burdens in the event of your death, you becoming critically ill or becoming disabled. Luckily, life insurance in Canada has great rates and unique plans that can fit your lifestyle and plans that are affordable as well. Another reason to get life insurance is the fact that it can have great riders such as critical illness riders, and disability riders. These riders are important to have because life is unexpected and it is best to be protected in any event.

A general rule of thumb to find out the life insurance coverage amount that you need is your annual income multiplied by 7 or 10. This number will help your family both: sustain their current lifestyle and be protected from financial hardships. This is just a quick calculation, the best way to figure out a solid amount of coverage is by contacting a life insurance broker and assessing your needs, wants, as well as your assets and liabilities.

Finding the right life insurance plan for you

If you are looking to purchase life insurance, there’s an affordable life insurance product or package for your situation and a life insurance specialist can help you create the best plan and package for your needs.

At Protect Your Wealth, we work with and compare policies and quotes from the best life insurance companies in Canada to ensure the best solution for you and your needs. We provide expert life insurance solutions, including no medical life insurance, critical illness insurance, term life insurance, and permanent life insurance to build the best package to give you the protection you need.

Contact Protect Your Wealth or call us at 1-877-654-6119 to talk to an advisor today! We’re proudly based out of Hamilton, and service clients anywhere in Ontario, British Columbia, and Alberta including areas such as Milton, Victoria, and Edmonton.

![Life Insurance with Anemia [2025]](https://sp-ao.shortpixel.ai/client/to_webp,q_glossy,ret_img,w_500,h_383/https://protectyourwealth.ca/wp-content/uploads/2022/06/anemia-header-image-500x383.png)

![How Life Insurance Riders Work In Canada [2025]](https://sp-ao.shortpixel.ai/client/to_webp,q_glossy,ret_img,w_500,h_383/https://protectyourwealth.ca/wp-content/uploads/2022/06/life-insurance-rider-header-500x383.png)

{kind=link}

Leave A Comment