How much does a 20-year term cost?

What factors affect the cost of life insurance? Plus more answers to all of your questions about the cost of a 20-year term policy.

15 Minute read

Originally published: April 22, 2022

Updated: May 24, 2023

How much does a 20-year term cost?

What factors affect the cost of life insurance? Plus more answers to all of your questions about the cost of a 20-year term policy.

15 Minute read

Originally published: April 22, 2022

Updated: May 24, 2023

The term length dictates the length of your policy and will also have a direct impact on the cost of your premiums. The term length you need will be determined by your age, income level and overall health and medical history. The best life insurance companies will offer a number of different terms in order to satisfy the demand. Shorter policies tend to be cheaper but could add up depending on the policy extension regulations associated with your policy. It is important to consider your financial goals prior to deciding on a specific term length.

In this article:

What are life insurance premiums?

Life insurances measure how much a client is expected to pay in order to achieve their desired policy and amounts of coverage. They dictate how much your life insurance will cost you on a monthly, quarterly or yearly basis. The duration will differ depending on the policy and type of life insurance you choose to pursue.

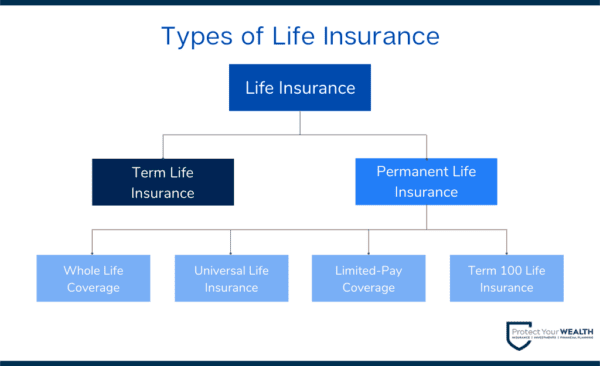

The two types are term life insurance and permanent life insurance. Term life insurance typically pertains to paying only the premium during the course of your determined term. Permanent life insurance, on the other hand, will offer coverage over the entire period, but you usually are expected to pay for the duration where the life insurance policy is active; with few exceptions.

What happens if I don’t pay my premiums?

If your premiums are not paid, the life insurance companies reserve the right to cancel your policy and/or deny you the benefit amount when the time comes. This may not be the case based on the terms and conditions of your specific agreement, but standard policies will be terminated in the event of a missing payment.

A permanent policy is one example of a possible exception to this. Some permanent policies contain a clause relating to a cash value. The money present in the cash value account is susceptible to being used to help pay your premiums.

Another exception is a grace period where your policy will not be terminated despite a missing payment. This clause is present in some policies, but it is rare and should be communicated beforehand.

How are premiums used by insurers?

Life insurance companies will use your premiums for a variety of financial endeavors. It is important to find a reputable life insurance company that will manage your payments properly and ensure their ability to pay the guaranteed death benefit. Premiums are usually used to:

Cover liabilities

The key role of life insurance companies is to offer your loved ones a death benefit, to help them stay afloat upon your passing. This means they need to set themselves in a proper financial position that can guarantee the payout on claims. Most reliable insurance companies have a large amount of money set aside in order to cover outstanding liabilities and ensure beneficiaries receive the money owed to them.

Cover business expenses

Life insurance companies also have their own expenses they need to cover in order to operate. A portion of your life insurance premiums will go towards these operating expenses and help companies pay salaries, buildings and all other expenses.

Invest

Life insurance companies may choose to invest money in order to gain a competitive advantage by offering lower costs on their policies. This promotes greater financial stability and extra assurance for policyholders. This is also how they offer whole life insurance policies, which guarantee an increase in the cash value of your premiums.

What factors affect the cost of life insurance?

Your life insurance cost will vary depending on a variety of factors. Most of the following will be considered by your life insurance company prior to providing you with a quote:

Age

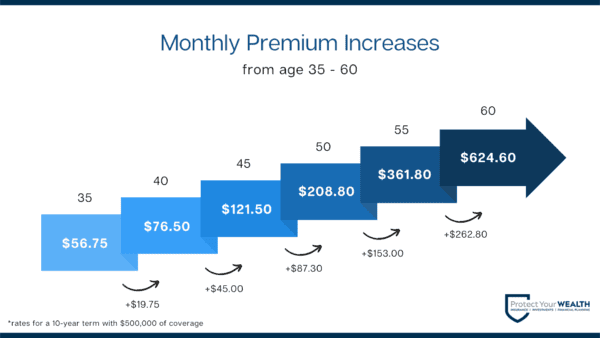

As you get older, your life insurance will also get more expensive. Insurers calculate quotes based on your specific circumstances, and your premiums will reflect how high-risk you are. As you age, your risk increases and this is reflected in the increased cost of your premiums.

Life insurance policies typically increase every year that you age. The most substantial increases occur when you become a senior, usually around age 60. This is something to consider when purchasing your policy, and it is important to plan ahead. In the event that you are purchasing a term policy, you need to consider how much your premiums will increase when your term ends. For instance, if you are a 60-year-old choosing to purchase a 20-year term policy when this term ends it will be very difficult for you to find an affordable policy as you are now 80.

Depending on your age, you may even be denied coverage by life insurance companies as many have maximum age limits. These ceilings will differ depending on the company and the type of insurance you are looking for.

Gender

Your gender is also a consideration for life insurance companies. This is because historical data has indicated that women tend to live longer on average than men. For a life insurance company, this means that women are at lower risk of insuring and this is reflected in their lower premiums. This information may be outdated, but there is currently not enough data to change the traditional underwriting guidelines.

Those who are transgender, nonbinary or genderqueer may be asked more questions regarding how they identify, but should not have a noticeable difference in premium costs. Life insurance companies are not allowed to increase rates or deny coverage due to your gender identity, hormone medication or history of gender confirmation surgery. Although they do reserve the right to postpone your application until after the surgery. Most companies do not offer gender-neutral options on their life insurance applications. Most insurers tend to operate based on the gender you were assigned at birth.

Smoking

If you are a smoker, you will face drastically higher life insurance premiums due to the health risks associated with smoking. Statistics indicating that smokers are 23 times more likely to develop lung cancer increases the risk of insuring, and the cost of your insurance will reflect that. Smokers can pay anywhere from 30%-300% more than non-smokers. While there may be no-medical insurance options that will not consider your health record; these options are already considerably more expensive than their alternatives.

In the event that you have quit smoking, your life insurance premiums may still be higher for a period of time. In order to be classified as a non-smoker, you need to have been smoke-free for at least a year. The longer you stay smoke-free, the cheaper your insurance will get over time.

Casual smoking is still considered smoking by life insurance companies due to its highly addictive nature. Even if you only smoke a single cigarette, this will count negatively toward your application. Vaping is also often considered the same as smoking to life insurance companies. Many companies have updated their policies on marijuana, but consuming it may still have a negative connotation and will vary from company to company.

Health

Health has a huge impact on life insurance premium costs as certain health conditions are considered very risky to insure. Your health and medical history will usually be obtained through a life insurance medical exam which permits access to your medical records.

Insurance companies will look at:

- Your medical history

- Height and weight (BMI)

- Risky behaviours

- Family medical history

Your family medical history is important for life insurance companies to consider due to the genetics involved. Trends in your immediate family’s mortality may indicate a higher chance of you suffering from illnesses or diseases. Illnesses and conditions that suggest a genetic predisposition include:

If it is found that you suffer from serious health conditions such as heart conditions, lung conditions and mental illnesses just to name a few. Your quote will likely be quite high; you may even be denied insurance. In these cases, you can look into no-medical life insurance options including simplified issue life insurance or guaranteed issue life insurance. Both these options are more expensive than their medical exam included counterparts but will provide you with some coverage for peace of mind.

Lifestyle

Your life insurance application will also cover information about your lifestyle. Your occupation and hobbies may reflect a high-risk lifestyle that makes it riskier to insure you. This will be considered by your insurer and may be reflected in the cost of your premiums. Some factors that they perceive as red flags include:

If your driving record showcases a history of DUIs, reckless driving convictions or suspended licenses; you are seen as a higher risk. This will increase not only your car insurance but also your life insurance as you will be perceived as a reckless driver. This makes it difficult for a life insurance company to offer you lower premiums.

Financial factors that may negatively impact your life insurance include bankruptcies. Most life insurance companies will typically deny you coverage if you have filed for bankruptcy in the last five years. Your credit score is also a risk some life insurance companies may consider because they fear you will be unable to afford the periodic premiums.

Most of the previous factors are out of your control or based on previous life decisions. But two factors you can cater to your life insurance needs include the type of life insurance you are applying for and life insurance riders.

Type of life insurance

The type of life insurance you choose will directly affect the cost of your premiums. Life insurance is split into 2 main categories: term life insurance and permanent life insurance. These categories are split further into more specific types of policies.

Term life insurance tends to be the more affordable option of the two with lower premium costs. However, these policies do come with an expiration date. Permanent life insurance guarantees coverage for your entire life, but comes at a higher price. Types of permanent life insurance include whole life insurance, universal life insurance and variable life insurance. All these policies vary in costs and the potential for the cash value of premiums growth.

Life insurance riders

Life insurance riders offer additional coverage to create a more all-around protection plan for your beneficiaries. They offer the advantage of extra financial protection beyond your traditional life insurance coverage and set you up for more unexpected circumstances. However, they do add additional costs to your policy and will result in higher premiums.

Some examples of riders include:

- Critical illness insurance riders

- Family insurance riders

- Accidental death and dismemberment insurance riders

- Benefit structure insurance riders

Riders are a great way to customize your life insurance policy to best suit your needs, but not all riders are right for you. The best way to determine what riders you need is to talk to an insurance advisor.

Contact Protect Your Wealth today to learn more about what riders suit your needs and enhance your life insurance.

What is term length?

The term length of your policy dictates how long your policy will last. The range for term life insurance policies typically runs from 10-30 years. The length of your coverage will depend on your unique financial situation.

At the end of your term, you can typically choose to:

- Renew or extend the coverage period

- Apply for a new policy

- Allow the existing policy to expire and lose coverage

How does term length affect the cost of life insurance?

The cost of life insurance differs depending on multiple factors as covered earlier, and term length is a considerable but not profound consideration. Shorter-term coverage lengths typically cost less than longer terms, but this will also be dependent on the policy itself.

When deciding on a term length you will need to consider your eligibility, as certain term lengths are no longer available at a given age. It is also vital to consider that at the end of your policy, you may be required to apply for more expensive coverage than if you had simply chosen a longer term from the start.

Contact Protect Your Wealth today to learn more about what term length is best for you.

How much does 20-year term life insurance cost?

As is the name, 20-year term life insurance pertains to coverage over a 20-year period. This is typically the shortest length policy available and by correlation the cheapest. The cost of the policies themselves will differ based on the company you choose, as well as, the amount of coverage that best suits your needs.

The differences in price are reflected in the following sections.

How much does 20-year term life insurance cost at different amounts of coverage?

100k Coverage

250k Coverage

500k Coverage

750k Coverage

1M Coverage

2M Coverage

5M Coverage

How much does 20-year term life insurance cost at different companies?

Assumption Life

BMO

Canada Life

Empire Life

Foresters

Humania

iA Industrial Alliance

Ivari

Manulife

RBC

SSQ

Sun Life

FAQs (Frequently Asked Questions)

A term life insurance policy is the simplest, purest form of life insurance: You pay a premium for a period of time – typically between 10 and 30 years – and if you die during that time a cash benefit is paid to your family (or anyone else you name as your beneficiary).

Most modern term life insurance policies do not expire until you reach age 95. Even though you may have a 10-year term life policy, your coverage will not end after 10 years. What does end, however, is the “rate guarantee” on that policy.

Finding the right life insurance for you

The term length you need will differ from person to person and may be difficult to decide on. However, different types of policies exist for your specific situation and you can work with an advisor to find the one that best suits your needs.

At Protect Your Wealth, we work with and compare policies and quotes from the best life insurance companies in Canada to create the best solution for you and your needs. We’ve been providing expert life insurance solutions since 2007, including no medical life insurance, term life insurance, and permanent life insurance, to build the best package to give you the protection you need.

Contact Protect Your Wealth or call us at 1-877-654-6119 to talk to an advisor today! We’re proudly based out of Hamilton, and service clients anywhere in Ontario, Alberta and British Columbia; including areas such as Stoney Creek, Airdrie and Nanaimo.

{kind=link}

Leave A Comment