What to know when buying life insurance in Canada

Types of life insurance, saving money on life insurance and more!

20 minute read

Originally published: June 30, 2022

Updated: September 27, 2023

What to know when buying life insurance in Canada

Types of life insurance, saving money on life insurance and more!

20 Minute read

Originally published: June 30, 2022

Updated: September 27, 2023

Finding out what to know when buying life insurance in Canada shouldn’t be a hard decision. There are plenty of great life insurance companies in Canada which have specifically designed well-rounded life insurance policies that are suitable for people coming from all walks of life. When thinking of choosing the right life insurance policy there are a couple of things that you should always keep in mind: the type of life insurance policy, the rating and premiums you receive, the flexibility of the life insurance policy, the financial stability of the life insurance company you plan to be insured by, and a few more important factors. This blog will be covering everything about what to know when buying life insurance in Canada.

In this article:

- Do I need life insurance?

- What type of life insurance is right for me?

- What is a life insurance rating

- How to get a better rating on your life insurance policy

- How much life insurance do you need?

- The cost of life insurance premiums

- How to save on your life insurance policy

- Is your life insurance policy flexible?

- Is your life insurance company financially stable?

- Questions to ask your life insurance advisor?

- Frequently Asked Questions (FAQs) about things to know when buying life insurance

Do I need life insurance?

To put it simply, life insurance is not for everyone. As useful as it is to have life insurance coverage, it might not be needed if you are someone who doesn’t have a family, dependants, debts or financial obligations, a mortgage or a business. In most cases, those who do have a family or a mortgage consider life insurance coverage because it is one of the most important precautionary efforts to protect your loved ones from financial instability in the case of your death. Life insurance has many pros too, besides protecting your family from financial instability, but there are multiple things that a life insurance death benefit can be used for. In many cases this money can be used towards funeral expenses, paying off a mortgage, paying for their children’s education, or simply just keeping the money for their savings and day to day spending.

Life insurance policies like permanent life insurance have a cash value with them which can be accumulated throughout your life. The accumulated cash amount can be then used toward investing, paying off your premiums, it can be added to your death benefit, and it can be used to supplement your retirement income. There are many questions that you can ask yourself if you are wondering whether or not you should get life insurance:

- Will my loved ones (partner, children, and dependents) need extra financial assistance to be able to care for themselves if I die?

- Is there anyone else who relies on me, such as my parents, grandparents, or siblings?

- Do I want my mortgage to be paid off if I die?

- Do I want to set aside money for my children’s education?

- Do I want to leave any money to family members or organizations?

- Will I leave unpaid debts behind that will reduce the value of my estate or burden my family?

- Would you like to supplement your retirement income with a permanent life insurance policy?

If your answer is “yes” to any of these questions, then it is likely that life insurance would be a good idea for you!

What type of life insurance is right for me?

Understanding the different types of life insurance is crucial when shopping for a life insurance policy. There are many kinds of life insurance, the most popular being fully underwritten insurance like term life insurance, then permanent life insurance. There are some other life insurance types such as simplified life insurance and guaranteed life insurance but these aren’t fully underwritten and offer lower coverage amounts.

FULLY UNDERWRITTEN | SIMPLIFIED ISSUE | GUARANTEED ISSUE | |

Cost of Premiums | |||

Medical Underwriting | Full medical history disclosed. | Limited medical questions. May differ by insurance company. | No medical questions asked. |

Visit from nurse or paramedical company | Most often yes. Sometimes substitued with physicians report. | No vist from nurse or paramedical company. | No vist from nurse or paramedical company. |

Speed of approval process | Longest process, may take few days to several weeks. | Typically within a few hours to a few days. | Typically within a couple hours to a couple of days. |

Maximum amount of coverage | No specified maximum. | Depends on company, age and health history. Can be up to 1M in coverage. | Depends on company and age. Most often between 25K and 50K maximum. |

What is term life insurance?

Term life insurance is a type of life insurance that pays out to your beneficiaries if you die during the term of your policy. You can specify how long your term policy will last. Insurance companies provide term life insurance for Canadians and those legally residing in Canada for 10, 15, 20, 25 or 30 years. Once the term expires, you will be able to renew your policy but there will be an increase in the premiums you pay. For example, if you purchase a 10-year term life insurance policy and you die during those ten years, the people you name as your beneficiaries will receive a tax-free payment (also called a death benefit).

Pros of term life insurance

In the event of your death or disability, you and your family will have financial security

Significantly less expensive than whole life insurance policies

Policy terms that can be tailored to your specific requirements

Your rates will never change once you’ve locked in your policy

Death benefit is guaranteed

What is permanent life insurance?

Permanent life insurance is also known as whole life insurance because it covers you for the rest of your life. It also provides your beneficiaries with a tax-free payment after your death. Some plans have the ability to accumulate cash value over time. Permanent insurance costs are typically guaranteed not to rise from the time the policy is purchased. Furthermore, some permanent insurance plans allow you to pay for a limited period of time and then never again. Other types of permanent life insurance to consider include universal life and participating life.

Pros of Permanent life insurance

Permanent Life Insurance is a policy that lasts your entire life

Additional key benefits include fixed premiums for the lifetime of the policy

Cash value that can be used to borrow against your policy and investment

Three types of permanent life insurances to choose from depending on your needs: whole life insurance, universal life insurance, and participating life insurance

What is simplified issue life insurance

Simplified life insurance is offered in permanent life and term life insurance forms. Medical exam is not required for simplified issue insurance policies, but you must answer certain health-related questions as part of your application. In return for no medical exam, premiums tend to be higher than traditional insurance. The number of questions asked varies by insurer and also by whether or not the policy is deferred. Simplified issue insurance is typically used for term life insurance products and is an option for those who want faster approval or do not want to take a medical exam. There are less coverage amounts and there are also higher monthly premiums with simplified plans.

Pros of simplified issue life insurance

No medical exam needed

Offered in term life insurance and whole life insurance options

People who have health issues and high risk lifestyles can get insured

Comparable coverage rates to term life and whole life insurance plans

What is guaranteed life insurance (no-medical life insurance)

These plans don’t ask any questions and don’t require any medical exams. Guaranteed issue insurance is intended for people with serious health problems or who are older and do not qualify for underwritten or simplified insurance. Many insurers will also offer a 24-month deferral period for guaranteed life acceptance insurance. Because it is also a type of permanent life insurance, guaranteed issue insurance coverage generally has a maximum of $50,000, with some insurers covering less, and has the highest premium of the three.

Pros of guaranteed life insurance

No medical exam needed

All health conditions and risky lifestyles are accepted

Easy to obtain

Can offer up to $50,000 which is great for those who are rejected from underwritten policies

What is a life insurance rating

You will have to go through an underwriting process as part of the application process for life insurance, which may result in a rating. Underwriting is the process by which an insurer calculates your risk factor as an individual by rating you. Each of Canada’s major life insurance carriers has its own underwriting guide, which is essentially a guide that explains how applicants are evaluated.

Medical exams are a component of the underwriting process that examines an applicant’s medical history as well as any unusual events in the applicant’s immediate family’s medical history. Underwriters may request a more comprehensive examination depending on the amount of insurance, age, and preliminary investigations. Although most medical exams are straightforward there is a chance that they might need to conduct some tests including a blood test, urine tests, an attending physician’s statement (APS), and other questionnaires.

Insurers may classify the applicant a rating, which affects the policy premiums. If the insurer determines that the applicant is in poor health, they are assigned a high risk level. However, there is a moderately wide range that is considered standard. If the applicant’s health is better than average, they may be offered a preferred (lower) rate. These ratings change what types of insurance plans you are eligible for as well as the price you will be paying for your premiums.

")

How to get a better rating on your life insurance policy

This can be tough depending on your situation especially if the reason you have a higher rating is because of something that is out of your control. This being said, if the issue is in your control then it is best to look into fixing or working on the issue that you are facing. In some cases, insurance companies might not lower your premiums, but there are many cases where informing them of your positive lifestyle changes can lead to lowering your premiums and giving you a better rating as well. Here are a couple of examples of how you can better your ratings:

- If you indulge in marijuana consumption whether it be smoking joints or eating edibles, try to avoid consuming marijuana everyday, in fact try to limit yourself to consuming marijuana to only 3 times a week to receive a standard rating.

- If you are a recovering alcoholic or a recovering addict, then keep your insurance company updated on your recovery process. Let them know of how long you have been sober, and let them know of any sobriety milestones that you reach. Let them know of any recovery programs that you are attending such as alcoholics anonymous or narcotics anonymous. Also inform your insurance company about any addictions therapies or counseling you attend.

- If you are overweight, try your best to lose weight if you are looking to receive a better rating. Let the insurance company know what you are doing to lose weight. This goes for those that are underweight as well!

- If you are in a risky occupation, let them know the fine details of your work, plus, let them know of your certifications and your licenses that make you qualified for that job.

- If you have any health conditions, let them know of the medication and the treatments you are receiving for your condition. This can be useful because if you are being consistent with your medication and treatments, this will positively affect your rating.

- If you are someone who takes part in extreme sports or hazardous hobbies, let them know about the specific details of your activities such as how high do you parachute from, or what kind of mountains you climb and how high you climb.

- If you are a smoker, try to quit smoking for a period of time prior to applying for life insurance

How much life insurance do you need?

When buying life insurance in Canada, deciding on how much life insurance coverage you need can vary depending on your personal situation. We strongly recommend that you contact a life insurance expert and complete a needs analysis to find an accurate measure of how much life insurance you need and what life insurance plan is best for you. Though, there are many ways that you can determine a rough estimate of how much life insurance coverage you need.

Times ten

This is one of the simplest methods to find out how much life insurance coverage you need. Basically, take your yearly income and multiply it by 10. For example: if you make $50,000 per year, multiply it by 10 (50,000 X 10 = $500,000). Therefore you will need $500,000 in life insurance coverage to ensure that your family can maintain their lifestyle without financial instability in the case of your death. You might want to add an extra $50,00-$100,000 per child as well.

DIME Formula

This is a more accurate method of calculating the amount of life insurance you need. This is a formula that a lot of life insurance experts use as well to ensure that you are getting the right amount of life insurance coverage. This is a basic rundown of what the dime formula is, essentially you want to add all these amounts together and see what the amount is to determine how much coverage is right for you.

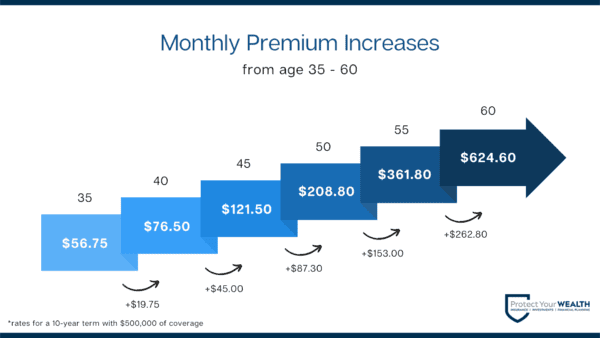

The cost life insurance premiums

Life insurance premiums vary depending on your individual circumstances, obviously, if you are someone who has a higher rating then you will be paying more per month for your life insurance, but if you are someone who has a standard or a preferred rating you are in luck. Another thing to consider about the cost of life insurance is the type of life insurance you are trying to get. The cheapest life insurance policy that is available in the market right now is term life insurance, it is both affordable and can have substantial coverage amounts. Permanent life insurance is still very popular and affordable as well but it might not be what everyone needs. Finally, on the more pricey side, you have simplified life insurance and guaranteed issue life insurance, these can still have very attractive rates for those who don’t qualify for underwritten life insurance policies.

Here is a chart which shows some of the prices that you might be paying for a term life insurance if you are a male or female, non smoker who is looking for a term life policy:

Comparing monthly life insurance rates*

Male – non-smoker

Coverage Amount | Age 25 | Age 35 | Age 45 | Age 55 | Age 65 |

$250,000 | $13.95 / mo | $14.18 / mo | $24.75 / mo | $63.23 / mo | $193.95 / mo |

$500,000 | $22.05 / mo | $22.50 / mo | $42.35 / mo | $97.83 / mo | $360.45 / mo |

$750,000 | $30.83 / mo | $30.84 / mo | $61.72 / mo | $144.95 / mo | $540.67 / mo |

$1,000,000 | $36.00 / mo | $36.90 / mo | $74.97 / mo | $188.19 / mo | $666.07 / mo |

Female – non-smoker

Coverage Amount | Age 25 | Age 35 | Age 45 | Age 55 | Age 65 |

$250,000 | $10.58 / mo | $11.03 / mo | $18.00 / mo | $43.65 / mo | $131.42 / mo |

$500,000 | $14.40 / mo | $16.65 / mo | $28.80 / mo | $74.21 / mo | $247.05 / mo |

$750,000 | $19.35 / mo | $22.15 / mo | $42.78 / mo | $109.51 / mo | $364.94 / mo |

$1,000,000 | $23.40/ mo | $27.00 / mo | $52.16 / mo | $132.66 / mo | $496.80 / mo |

How to save on your life insurance policy

With the cost of living projected to get higher and higher in Canada, it is best to save your money any way you can. Life insurance is a great way to protect yourself, but costs money and requires you to pay monthly or annually. These payments obviously add up and must be entered into your budget. Luckily, there are numerous ways to save on your life insurance policy, in fact you can get a life insurance policy that roughly costs the same as a cup of coffee a day! Here are a couple of things we recommend trying if you are looking to save money on your life insurance policy.

Get term life insurance

As stated earlier, when buying life insurance in Canada, term life insurance is on average much cheaper than permanent life insurance, simplified insurance and guaranteed issue insurance. There are awesome term life insurance products in plenty of different Canadian life insurance companies and all of these have really competitive and affordable premiums if you have a standard or preferred rating. Check out our list of the best insurance companies in Canada!

Buy life insurance when you’re younger

The younger you are, the better your rating is, thus the cheaper your premiums will be. Age plays a major role in the underwriting process when applying for life insurance. This being said, if you get life insurance coverage at a younger age you will be paying a dramatically lower rate than if you look for life insurance at an older age.

Make positive changes to your life

As stated earlier, if you are overweight, underweight, if you are a smoker, if you have a health condition that can be improved, or have any sort of lifestyle choice or circumstance that can be improved then work on it! Having a bad habit is normal and if you can kick your bad habit, insurance companies will take note of this and give you a standard rating if you have improved your lifestyle.

Pay for your premiums annually

Paying your premiums month to month might be easy, but some insurance companies offer great deals to those who pay annually. Some life insurance companies offer discounts as large as 10% off if you opt to pay annually instead of month to month.

Work with a life insurance broker

When buying life insurance in Canada, you should really think about working with a life insurance broke! At Protect Your Wealth we offer a completely free life insurance brokerage service. We have free consultations and you don’t pay us at all in the entire process of purchasing insurance. We make getting life insurance an easy process and we are experts in the field. We can showcase the multiple different rates offered by multiple different life insurance companies and then narrow down what is right for you. Purchasing life insurance is a massive decision, make sure that you are working with a professional.

Is your life insurance policy flexible?

The availability of flexibility is important when buying life insurance in Canada. Life insurance products should be an important consideration when selecting a life insurance company. Life insurance requirements change over time based on the insured’s lifestyle, profession, and medical condition. It’s a good idea to go with a life insurance company that can help you transition from one type of policy to another.

Many life insurance companies also offer “riders” with your life insurance policy, and these are basically some add-on features such as children’s insurance, critical illness insurance, disability insurance and more which can help you if you are interested in additional coverage. These are great add-ons and can really be helpful if you are looking for a stronger and personalized life insurance policy. If these add-ons are important to you, make sure that you choose a life insurance company that is flexible.

Is your life insurance company financially stable?

Although life insurance companies are financial institutions that deal with hundreds of millions of dollars, and even billions of dollars in many cases, they can still go under. Although your money is protected regardless of if your life insurance company dissolves or changes, financial stability in life insurance companies can give you the confidence to not have to worry about the transitioning your life insurance coverage to another company. We have plenty of life insurance company reviews which details the financial stability as listed by A.M. Best Company. You can check A.M. Best Company, and Better Business Bureau to find out the financial stability of your life insurance company as well.

Questions to ask your life insurance agent?

When buying life insurance in Canada, there are many different questions that you should ask your life insurance agent and these include questions about their own certifications and their expertise, but also you should ask the life insurance agent some questions regarding your own personal needs and wants. Life insurance brokers or agents are there to help you understand your life insurance options and help you make an informed decision. To give you some peace of mind, the best resource that is available to see if the life insurance agent you’re working with is registered is through using this tool created by the Financial Services Regulatory Authority, which will let you know if your life insurance agent is licensed with the FSRA.

These are some questions that you should ask your life insurance agent when you are having a consultation:

- What insurance companies do you work for?

- What types of insurance can you sell?

- Do you provide any other financial services, such as mortgage brokerage or mutual funds?

- How long have you been in operation?

- Is your Errors and Omissions (E&O) insurance up to date? (All insurance agents are required to have current E&O insurance.)

- Have you completed the required 30 hours of continuing education every two years?

- Do you have any additional professional credentials, such as Chartered Life Underwriter or Chartered Financial Consultant?

- Will you send me a letter of engagement outlining the services I can expect from you both during and after the sale?

- How are you compensated?

- Do you have any other relationships that may create actual or potential conflicts of interest?

- How/when can I contact you for advice or more information?

These are some questions that you should ask your life insurance broker regarding your personal situation:

- What amount of life insurance do I require? How did you arrive at that figure?

- What kind of coverage do I need if I have children?

- What is the best type of insurance for me?

- How does this policy address my needs and circumstances?

- Can you give me some alternatives or options?

- Will you provide me with policy examples?

- When can I expect to receive a copy of my application? What is my policy?

- Can I change the death benefit and premiums later if my personal circumstances change?

- Can I include my children in my policy?

Frequently Asked Questions (FAQs) about things to know when buying life insurance

A smoker is someone who has used any of these products in the last 12 months:

- Any tobacco products (cigarettes, nicotine base products)

- E-cigarettes, vaping device

- Marijuana (over a certain limit)

*An occasional cigar is often defined as one large cigar per week with negative cotinine results on urine tests.

Yes, recovering alcoholics can buy traditional life insurance after three years of sobriety and will pay much higher rates than people with no history of alcohol addiction.

Yes, recovering addicts can buy traditional life insurance, no medical life insurance, and simplified life insurance. This all depends on the drug used, the usage frequency, years sober and many other factors. Regardless, if you are a recovering addict there are plenty of life insurance companies that are willing to provide you coverage.

A term life insurance policy is the simplest, purest form of life insurance: You pay a premium for a period of time – typically between 10, 15, 20, 25 and 30 years – and if you die during that time a cash benefit is paid to your family (or anyone else you name as your beneficiary).

Term life insurance provides coverage for a set period of time, typically between 10 and 30 years, and is a simple and affordable option for many families. Whole life insurance lasts your entire lifetime and also comes with a cash value component that grows over time.

When buying life insurance in Canada, a 20-year term life insurance policy has a level (unchanging) premium and a specific death benefit. As long as premiums are paid, your coverage will remain intact. This helps to ensure your beneficiaries are protected if you pass away. Once you reach the end of the policy term, the policy ends.

A 10-year term life insurance policy has a level (unchanging) premium and a specific death benefit. As long as premiums are paid, your coverage will remain intact. This helps to ensure your beneficiaries are protected if you pass away. Once you reach the end of the policy term, the policy ends.

This depends on the details of your life insurance policy. If your policy is revocable, this means you can change the beneficiary on file at any time without needing to notify the previous beneficiary. Your policy could also be irrevocable, which means the owner of the policy is not able to change the beneficiary without the original individual’s consent.

No medical life insurance is a certain type of life insurance that you can buy without having to undergo a medical examination. This type of life insurance is easier to apply for and usually has a shorter application period.

There is currently no limit on how many life insurance policies you can have, and in some cases, having multiple life insurance policies may help you meet your goals for your financial future.

Yes, seniors can definitely purchase life insurance in Canada. There are awesome term life insurance policies as well as whole life policies that are out there that can provide coverage for seniors 60 years and older.

There are so many reasons for you to get life insurance, the main being that it will protect your loved ones from any financial burdens in the event of your death, you becoming critically ill or becoming disabled. Luckily, life insurance in Canada has great rates and unique plans that can fit your lifestyle and plans that are affordable as well. Another reason to get life insurance is the fact that it can have great riders such as critical illness riders, and disability riders. These riders are important to have because life is unexpected and it is best to be protected in any event.

A general rule of thumb to find out the life insurance coverage amount that you need is your annual income multiplied by 7 or 10. This number will help your family both: sustain their current lifestyle and be protected from financial hardships. This is just a quick calculation, the best way to figure out a solid amount of coverage is by contacting a life insurance broker and assessing your needs, wants, as well as your assets and liabilities.

There are a handful of things to consider when you purchase life insurance:

- Life insurance term

- Life insurance benefits, or additional riders

- Health conditions which are pre-existing or you are susceptible to based on family medical history

- Smoking status (smoker or non-smoker)

- Your age

- Children’s or dependent’s age

- Spouse’s age

- Occupation risks

- Existing loans and mortgages

Need help with buying life insurance in Canada

Buying life insurance in Canada is simple and we are here to find out about all your needs and wants to find the right life insurance policy for you!

At Protect Your Wealth, we work with and compare quotes and policies from the best life insurance companies in Canada to help find the perfect solution for your needs. We’ve been providing expert life insurance solutions since 2007, including no medical life insurance, critical illness insurance, and permanent life insurance, to build the best package to give you the protection you need.

We’re proudly based out of Hamilton, and service clients anywhere in Ontario, Albert and British Columbia, including areas such as Toronto, Edmonton, and Vancouver. Contact Protect Your Wealth or call us at 1-877-654-6119 to talk to an advisor today!

{kind=link}

Leave A Comment