How to Get the Best Life Insurance Policy and Rates in Canada

Saving on life insurance pays off in the long run, learn how to get the best rate for yourself.

13 Minute read

Originally published: June 21, 2021

Updated: November 8, 2023

How to Get the Best Life Insurance Policy and Rates in Canada

What to look for when considering insurance companies and how to prepare for a medical exam.

13 Minute read

Originally published: June 21, 2021

Updated: November 8, 2023

Life insurance is an important investment to protect families and loved ones from financial burdens in the event of a tragedy. It’s important to know the different situations for why you might need life insurance and what it offers, and how to get the best life insurance policy coverage at an affordable rate for your situation. There is a life insurance plan out there for everyone: if you are older, if you have a health condition, if you live an unhealthy lifestyle, if you have a criminal conviction, if you are a newcomer and many more.

In this article:

Why Do You Need Life Insurance in Canada?

Life insurance is designed to protect a person and their family from the financial burdens of an unexpected death. There are many kinds of insurance (including both disability and critical illness insurance) however, the basic and most important is considered to be life insurance. Death in the family can lead to heart-breaking emotions and additional stress. Although nobody can be replaced, life insurance provides financial peace of mind for dependents in case of premature death.

Life insurance can help the family meet expenses for a while, protect dependent parents, or secure the children or spouse. It can also secure other financial obligations which could include funeral expenses, unsettled medical bills, mortgages, business commitments, meeting the college expenses of the children, and so on.

What happens if you have no life insurance? Your financial obligations, expenses, dependents, and any other loved ones are left with a financial burden while they’re grieving. It’s an important investment for families to protect their loved ones in the case of a tragedy: while we hope it’ll never happen, it’s important to be prepared for it.

Just as everyone’s situations are different, there are different reasons for why a person would need life insurance. Below is a list of 10 reasons why a person would need life insurance.

Family protection for expenses

Pay off estate and death duties

To earn savings or pension

Life insurance can have a savings or pension component that provides for you during or before retirement. It be used as apart of a retained earnings strategy which allows for tax free growth of cash value within a corporately owned account or used as an alternate tax free vehicle to a Tax Free Savings Account (TFSA) or Registered Retirement Savings Plan (RRSP).

Additional protection for spouse or children

Financial assets

Creditor proof assets

Covering funeral expenses

Protection for life

Protecting your business

Maintaining your family’s lifestyle

As an important part of your financial plan, life insurance provides peace of mind for any uncertainties in life. Insurance is vital to good financial planning and security but you would need to assess your personal risk and long term commitments.

10 Factors to Consider to Get the Best Term Life Insurance Policies

When searching for a life insurance policy for your needs, there are several factors to consider when looking for the best policy for you. While the premium of the policy is very important to consider for your budget, there are other considerations to take into account. Below are 10 factors we consider when recommending policies:

Underwriting Requirements

Given most would rather (if given an option) avoid providing urine, blood and vitals for a life insurance application, one major factor of comparing carriers relates to underwriting requirements. Depending on the age and face amount of the policy, an applicant may qualify for this type of accelerated underwriting. Manulife Insurance for example allows those aged 45 and under to apply up to 1M of life insurance without a medical exam. Almost all carriers have some form of non-medical insurance, which is most often a simplified life insurance policy.

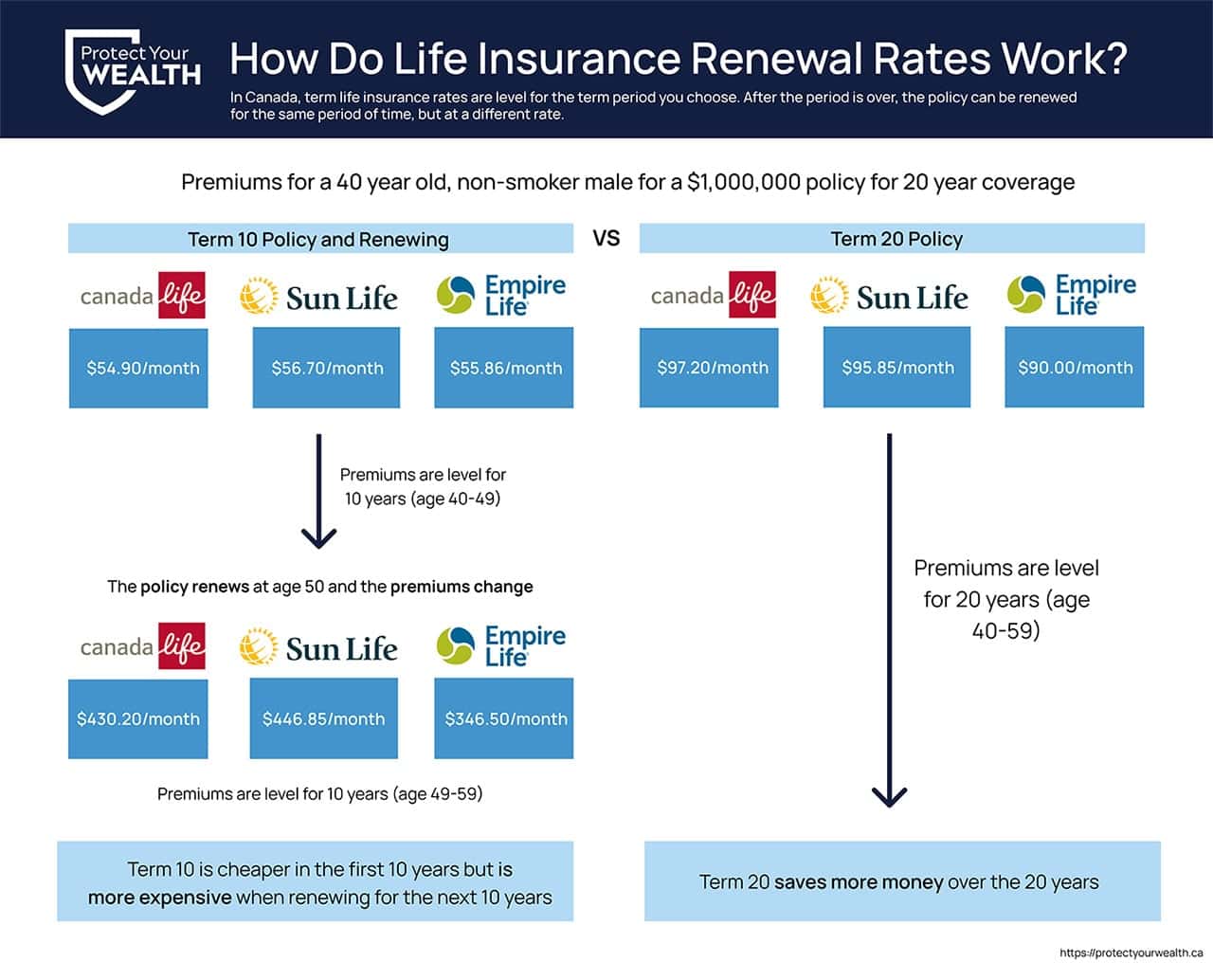

Renewal Rates

Have Excellent Permanent Life Insurance Products

Have Better Preferred Rates

More Likely to Offer Preferred Rates

Have Unique Value Added Features at No Additional Cost

Have Unique Product Features for Future Benefit

Ask Less Questions Within Their Applications

Have Better Customer Service

Strength and History of Company

Perhaps, knowing Foresters Financial maintains an extremely high capital reserve against insolvency is extremely important to you. Or knowing that Canada Life has been paying policy dividends since 1848 is reassuring. Or recognizing brands such as Sun Life Insurance and Manulife gives peace of mind. Or knowing that Ivari is an insurance company owned by a company owned 100% by the Canada Pension Plan. Whatever the circumstances, history and strength of the company can play a factor in choosing the right life insurance company to apply.

5 Tips for Lowering Your Insurance Costs Without Sacrificing the Coverage

Once you’ve pinpointed what you want for your coverage, it’s important to make sure you can afford it. Using a little common sense and initiative can save you some money and make life insurance more affordable. Here are our top 5 tips to help you get the cheapest and best deal available.

Work with an insurance broker

The number one tip when shopping for life insurance is to work with an insurance broker who has access to a wide range of companies and products. The factors we’ve discussed above are all factors that an insurance broker knows the ins and outs of, for a wide range of companies and products, making it easier for you to find the right insurance company for you. At Protect Your Wealth, our online life insurance quotes make it easy to compare the rates and products of some of Canada’s largest insurance companies.

Check for how you can pay for your policy

Many companies will allow you additional savings if you choose to pay for your policy on an annual basis or by direct debit straight from your bank account. It is worth checking on this because you could be able to make savings rather than paying on a weekly or monthly basis.

Take out one large policy

Where possible, instead of taking out several different smaller policies for life insurance take out just one larger one. A large policy is always the best value for money and will sell for less per amount of coverage.

Keep your policy recent

If you have held a policy for a number of years then it might be outdated and you could be paying more than you should be for the amount you are covered for. You could be paying around 2 to 3 times more than could you be if you shopped around online and compared newer policies for a better deal. Term rates in particular have fallen quite significantly in recent years and it is possible that the same coverage is much more cost effective today.

Improve your health

If you quit smoking and drinking, start exercising and lose weight if you need to, you could find that your premiums are a lot lower than those who smoke and drink etc. Several companies offer preferred premiums, which are much lower, for healthy individuals.

How to Prepare for a Life Insurance, Critical Illness or Disability Exam

Depending on your age, medical history, face amount or insurance company, a medical examination is often required as a part of the life insurance and critical illness insurance application process. These exams can be arranged either at your home or place of business, often both during and after business hours, including the weekends.

Given the results can have a direct impact on your rate classification, which helps to determine your premiums, it is important to follow a few simple rules for the best results possible.

Below are 10 tips to help you prepare:

- No strenuous exercise for at least 24-48 hours BEFORE the nurses visit

Be well rested

- If applicant has a cold or flu, reschedule the appointment

- Limit alcohol for 24 – 48 hours prior to the exam

- Limit caffeine – coffee, hot chocolate, pop or sport drinks

- Reduce Smoking

Fasting may be required

- Avoid vitamins and supplements for 24 hours

- Continue all prescribed medications

- Relax!

Avoiding small things like milk that day (contains sugar and fats) and even chewing gum (sugar) can help provide better results. While overhauling your entire routine may not be possible, following these few simple tips can help ensure the best results possible.

Do you have life insurance questions?

There are several factors to consider when looking for life insurance, and even applying for it. Working with a life insurance expert or broker can help you find the best solution for your needs.

At Protect Your Wealth, we provide award winning expert financial planning advice and life insurance solutions at the comfort of your own home or office. We would be happy to provide further analysis for you and your family’s specific circumstances. Contact Protect Your Wealth or call us at 1-877-654-6119 to speak with an advisor today. We’re proudly based out of Hamilton, and service clients anywhere in Ontario, including areas such as Ancaster, Oakville, and Waterdown.

Frequently Asked Questions (FAQs) about getting life insurance

There are many! The best life insurance for you will depend on your specific situation. See our blog, best life insurance companies in Canada for more information on each company and its specific strengths and weaknesses.

Key considerations when looking for the right life insurance for you is a low premium and a good rating. This will ensure that you will be properly protected at an affordable rate.

No. The individual being insured under the policy is required to sign the application and give consent. They also need to choose you to be a beneficiary for you to obtain any of the death benefits.

Some reasons where life insurance companies are allowed to refuse to pay the death benefit include:

- suicide

- withholding information on the application

- dangerous activities

- illegal activities

- acts of war

- living out of Canada

- fraud

- no insurable interest

- policy replacement

The most likely reason why your death benefit is not being paid is if the client missed a premium payment. This would result in a terminated policy and means you will not receive any benefits.

{kind=link}

Leave A Comment