Canada Protection Plan Review: CPP Life Insurance Explained

By Parvesh Benning, Licensed Life Insurance Broker

Most Canadians treat Canada Protection Plan as a last resort. Experienced brokers often go there first.

Canada Protection Plan sits in a category of its own in the Canadian market. It’s not the cheapest option for healthy applicants and it’s not trying to be. What it does better than any other carrier is get coverage in place fast, without risking a full underwriting process that could surface something and close other doors later.

Updated: March 31, 2026

Canada Protection Plan Review: CPP Life Insurance Explained

By Parvesh Benning, Licensed Life Insurance Broker

Most Canadians treat Canada Protection Plan as a last resort. Experienced brokers often go there first.

Canada Protection Plan sits in a category of its own in the Canadian market. It’s not the cheapest option for healthy applicants and it’s not trying to be. What it does better than any other carrier is get coverage in place fast, without risking a full underwriting process that could surface something and close other doors later.

Updated: March 31, 2026

Canada Protection Plan sits in a category of its own in the Canadian market. It’s not the cheapest option for healthy applicants and it’s not trying to be. What it does better than any other carrier is get coverage in place fast, without risking a full underwriting process that could surface something and close other doors later.

CPP holds an “A” (Excellent) rating from AM Best and is backed by Foresters Financial, one of North America’s oldest fraternal benefit societies. Their focus is narrow by design: no-medical and simplified issue coverage for Canadians who need protection now, not after a six-week underwriting process.

This review covers who CPP is genuinely right for, how their tier system works from a broker’s perspective, and where other options should be considered first.

Is Canada Protection Plan worth it?

Short Answer: Canada Protection Plan is best suited for Canadians with health conditions, previous declines, or urgent coverage needs. For healthy applicants, fully underwritten life insurance will almost always offer lower premiums and better long-term value.

Key Facts:

| Factor | Details |

|---|---|

| Approval Time | 1 to 3 business days on most plans |

| Medical Exam | Not required on most plans |

| Coverage Amount | Up to $1,000,000 depending on health profile |

| Best For | Health conditions, previous declines, urgent coverage needs |

| Not Ideal For | Healthy applicants seeking the lowest possible premium |

In this guide:

- Who Is Canada Protection Plan and Who Underwrites Them

- What Is No Medical Life Insurance (and What Does It Actually Skip)?

- Who Qualifies for Simplified Issue Coverage at CPP

- Pros and Cons of Canada Protection Plan

- How CPP’s Qualification System Actually Works (Most Clients Get This Wrong)

- What Foresters Member Benefits Come With Every CPP Policy

- How Financially Secure Is Canada Protection Plan

- Should You Choose CPP or Traditional Insurance?

- CPP Term Life Insurance Options and Coverage Limits

- CPP Permanent Life Insurance Options and Who Each Plan Suits

- Term vs. Permanent: Which Is Right?

- How CPP Final Expense Insurance Works and Who It Makes Sense For

- Critical Illness Coverage Through Canada Protection Plan

- CPP Product Comparison: Express, Simplified and Deferred

- How Canada Protection Plan Underwrites Health Conditions and Lifestyle Risks

- What Canadians Say About Canada Protection Plan

- Frequently Asked Questions: Canada Protection Plan

Who Is Canada Protection Plan and Who Underwrites Them

Canada Protection Plan (CPP) is a no medical and simplified issue life insurance provider founded in 1992 and headquartered in Toronto. They operate in a specific lane: coverage for Canadians who need protection quickly, without a medical exam, regardless of health history.

CPP is underwritten by Foresters Life Insurance Company, which holds an “A” (Excellent) rating from AM Best. All plans are protected by Assuris, the not-for-profit organization that guarantees Canadian policyholders receive at least 85% of their benefits if an insurer fails. For a no-medical carrier, that backing matters.

A few things set CPP apart from other simplified issue providers. They allow credit card payment on annual premiums, which is rare in the Canadian life insurance market. When you hold a CPP policy you also become a Foresters Financial member, which comes with a package of benefits that have nothing to do with the insurance itself. And for applicants with pre-existing conditions, their tiered qualification system means there is almost always a coverage option available, even when other carriers have said no.

That said, CPP is not the right choice for every client. For healthy applicants under 50 with no complicating health factors, fully underwritten coverage will almost always cost less. The question a broker asks first is not “should we use CPP” but “does this client’s situation call for simplified or fully underwritten,” and then comparing all options within that category.

Monthly Term Life Insurance Rates

10-year term, $500 000 coverage | Canadian smokers & non-smokers

| Age | Male | Female | ||

|---|---|---|---|---|

| Smoker | Non-Smoker | Smoker | Non-Smoker | |

| 20 | $55.35 | $39.60 | $37.80 | $30.15 |

| 25 | $55.80 | $40.50 | $39.15 | $31.50 |

| 30 | $59.85 | $40.50 | $44.10 | $32.40 |

| 35 | $69.30 | $40.50 | $51.75 | $36.00 |

| 40 | $97.20 | $48.60 | $85.50 | $39.60 |

| 45 | $169.65 | $66.15 | $156.60 | $53.55 |

| 50 | $325.80 | $98.55 | $270.45 | $78.75 |

| 55 | $523.80 | $170.55 | $386.55 | $138.60 |

| 60 | $913.95 | $317.25 | $571.50 | $206.55 |

| 65 | $1 424.25 | $486.00 | $782.55 | $328.05 |

| 70 | $2 547.00 | $905.40 | $1 198.35 | $603.45 |

protectyourwealth.ca

What Is No Medical Life Insurance (and What Does It Actually Skip)?

No medical life insurance is coverage that skips the physical exam, blood work, and report from your doctor. Instead of traditional underwriting, these policies use simplified health questionnaires to assess eligibility and set your premium.

The trade-off is real. Because the insurer is taking on more unknown risk, premiums run higher than fully underwritten coverage for the same face amount. For a healthy 35-year-old, that difference can be significant. But for someone with diabetes, a history of heart disease, or a previous decline, no medical coverage isn’t a compromise. It’s often the only realistic path to meaningful protection.

What CPP does that most no-medical providers don’t is offer multiple tiers within the no-medical space. You’re not just choosing between “qualified” or “not qualified.” Depending on how you answer the health questions, you land in a tier that determines your coverage amount, your premium, and how quickly the full death benefit kicks in. The healthier your profile, the better the tier, and the better the terms.

For Canadians who assume a health condition means they can’t get covered, that’s rarely true. Controlled diabetes, managed high blood pressure, even a history of cancer depending on how long ago and what type, these don’t automatically close the door. They just determine which door you walk through.

Who Qualifies for Simplified Issue Coverage at CPP

Most Canadians between 18 and 80 can apply for at least one CPP product. The tier you land in depends on how you answer the health questions, not on whether you qualify at all. That distinction matters more than most people realize going in.

CPP’s simplified issue products are commonly used by Canadians who:

- Have a history of controlled conditions like diabetes, high blood pressure, or heart disease

- Have been declined or rated by a traditional carrier

- Work in high-risk occupations or engage in extreme sports

- Want fast approval without a medical exam or blood work

- Are temporary residents with a valid work or study permit (coverage available up to $250,000)

Coverage ranges from $5,000 on Guaranteed Acceptance plans up to $1,000,000 on Preferred plans, depending on your health profile. The right tier is determined by working through the application questions section by section. See the FAQ for common eligibility questions.

Pros and Cons of Canada Protection Plan

CPP Pros

- Anyone can apply, regardless of medical history or current health.

- No medical exams for most plans, including Express Elite and Simplified Elite tiers.

- Fast approvals – many policies offer same-day or next-day decision timelines.

- Foresters member benefits included at no extra cost: scholarships, wellness tools, legal document preparation via LawAssure, and more.

- Coverage available for higher-risk conditions like diabetes, heart disease, or a history of declines.

- Annual premium credit card payment accepted, with approximately 9% discount over monthly – rare in the Canadian market.

CPP Cons

- Higher premiums than traditional life insurance for healthy applicants.

- Coverage caps at $1,000,000, lower than fully underwritten plans which often go to $2,000,000 or higher.

- No participating or universal life options – not suitable for estate planning or cash value accumulation strategies.

- Coverage ends at age 80, compared to age 85 for most traditional Canadian carriers.

- Limited term flexibility – the 30-year term is only available on Express Elite, not across all product lines.

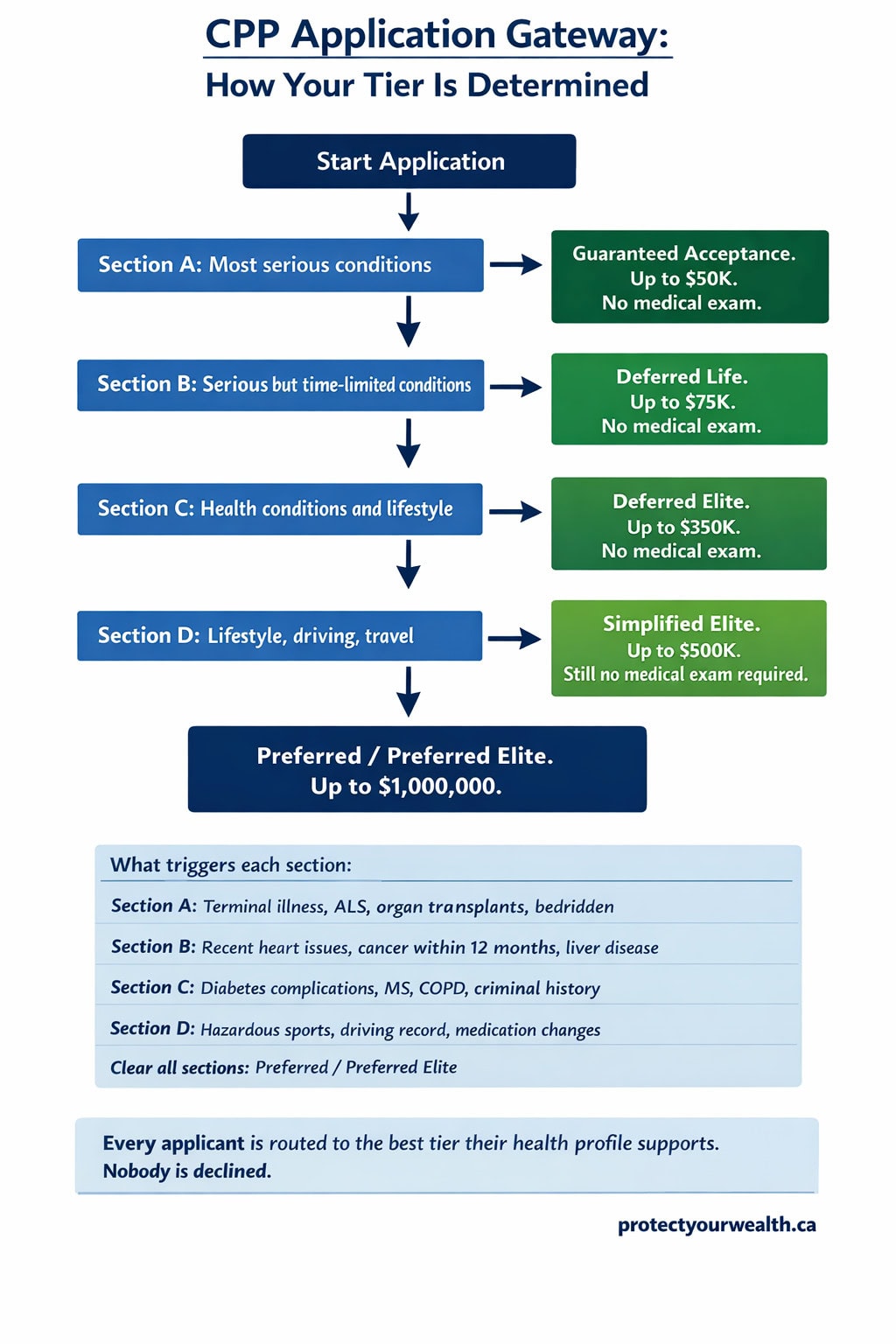

How CPP’s Qualification System Actually Works (Most Clients Get This Wrong)

Most people think applying for CPP is a pass/fail decision. It’s not. The application is structured as a series of sections, and how far you get through those sections determines which product you qualify for. The further you go without triggering a yes, the better your coverage, your rates, and your options.

Here’s how it actually works. Section A covers the most serious conditions: organ transplants, terminal illness, ALS, being bedridden, and a handful of others. If you answer yes to anything in Section A, you’re routed to Guaranteed Acceptance Life, which has a two-year modified benefit period and a maximum of $50,000. If you clear Section A with all nos, you move to Section B. Clear that and you move to Section C, then Section D. Each section you clear opens a better tier with higher coverage limits and better terms.

Clear all sections and you’re looking at Simplified Elite at up to $500,000, or Preferred plans at up to $1,000,000. Nobody gets declined. The form routes everyone to the best product they can reach based on what they disclose.

I explain it to clients this way: block by block, the longer we can answer no, the better the product we land on. That’s it. There’s no mysterious underwriter making judgment calls. The application itself does the routing.

Here’s the part most people don’t think about. Applying through CPP carries no formal decline risk with other carriers. A simplified application doesn’t generate the same kind of record that a full underwriting process does when something surfaces and gets flagged. I’ve seen this play out badly for clients who went the other way: they went through full underwriting first, something came up during the medical, and now their options on the simplified side are more complicated than they would have been if we’d gone simplified first.

My approach when there’s any doubt about qualification is to get coverage in place first through the simplified path, then revisit fully underwritten options afterward if the client wants to explore whether they can do better on price. You lock in insurability now while you’re relatively healthy. If something changes between now and when you apply for fully underwritten coverage, at least you’re covered.

That’s also why CPP isn’t always a last resort for me. A commercial helicopter pilot, for example, is someone most fully underwritten carriers will rate heavily or decline outright. I’m not going to put that client through a medical and a waiting period to find out the answer I already know. I go to simplified first, compare CPP against every other simplified provider on price and terms, and get them covered. If CPP wins that comparison, we go with CPP. If another simplified carrier is better suited, we go there instead.

Not sure which tier you’d land in or whether CPP is the right fit for your situation? Talk to a broker directly – the conversation is free and there’s no obligation.

What Foresters Member Benefits Come With Every CPP Policy

When you take out a CPP policy you automatically become a member of Foresters Financial, one of North America’s oldest fraternal benefit societies. The membership benefits kick in immediately after approval and cost nothing extra. Most clients don’t know these exist until I mention them.

The ones clients actually use most:

- LawAssure: Create wills, powers of attorney, and health directives online at no cost. For clients who have been putting off estate documents, this alone is worth something.

- Scholarship Program: Competitive tuition support for dependent family members.

- Orphan Benefit: Up to $900 monthly per child if the insured passes away.

- Volunteer Grants: Up to $1,500 for qualifying family or community activities.

- Member Events: Access to Foresters-organized community and family events across Canada.

- Lifelong Learning: Free access to professional online courses for policyholders.

These are non-contractual benefits, meaning Foresters can change or discontinue them. But they’ve been in place consistently and add real value beyond the insurance itself. For a client who is already choosing between CPP and another simplified provider at similar pricing, the membership package is a legitimate tiebreaker. You can read more in our full Foresters Financial review.

How Financially Secure Is Canada Protection Plan

CPP policies are underwritten by Foresters Life Insurance Company, which holds an “A” (Excellent) financial strength rating from AM Best. That rating reflects the insurer’s ability to pay claims over the long term, which matters more than most people think when choosing a no-medical carrier.

All CPP plans are also protected by Assuris, the not-for-profit organization that protects Canadian life insurance policyholders if an insurer becomes insolvent. Assuris guarantees at least 85% of your death benefit up to $200,000, and 100% of benefits above that threshold. For most CPP policyholders, that means full protection.

CPP publicly states a 98% claims payout rate on non-contestable claims. A claim becomes non-contestable after the policy has been in force for two years, at which point the insurer can no longer challenge it based on application information, except in cases of fraud. During that first two-year window, CPP can review a claim for misrepresentation if the insured passes away. That’s standard across all Canadian life insurance policies, not specific to CPP, but worth understanding before you apply.

The practical takeaway: CPP pays claims. The 98% figure is consistent with the Canadian industry average and reflects a carrier that has been in the no-medical space since 1992.

Should You Choose CPP or Traditional Insurance?

The honest answer is that CPP isn’t the right first call for everyone. For a healthy applicant in their 30s with no complicating health factors, fully underwritten coverage will almost always cost less for the same face amount. Sometimes significantly less. The no-medical convenience comes at a price, and if you don’t need that convenience, you’re paying for something you don’t need.

Where CPP makes sense:

- You have a health condition that would trigger a rating or decline with traditional carriers

- You’ve already been declined or rated elsewhere

- You work in a high-risk occupation where traditional carriers apply heavy loadings

- You need coverage in place quickly and can’t wait 4-8 weeks for full underwriting

- You’re a temporary resident with a valid work or study permit

- There’s genuine uncertainty about how a medical would go and you want to protect your insurability

Where traditional underwriting makes more sense:

- You’re in good health with no significant medical history

- You want the lowest possible premium for a given coverage amount

- You need coverage above $1,000,000

- You’re looking for participating whole life, universal life, or other products CPP doesn’t offer

The question I ask first isn’t “should we use CPP.” It’s “does this client’s situation call for simplified or fully underwritten coverage.” Once that’s settled, I compare every provider in that category on price, terms, and fit. CPP wins that comparison regularly in the simplified space, but it doesn’t win every time. That’s the advantage of working with a broker who isn’t tied to one carrier.

Use this comparison table to decide:

| Client Situation | Recommended Option |

|---|---|

| In excellent health, under 45 and want the lowest premium | Traditional fully underwritten insurance |

| Have a pre-existing condition (e.g., diabetes, cancer history) | CPP Simplified Elite or Deferred Elite |

| Need fast approval or can't complete a medical exam | CPP Express Elite or Simplified Elite |

| Previously declined or high-risk occupation | CPP Deferred Elite or Guaranteed Acceptance depending on health profile |

protectyourwealth.ca

CPP Term Life Insurance Options and Coverage Limits

Canada Protection Plan offers five simplified and no medical term life insurance products. They vary by health eligibility, coverage limit, and underwriting requirements. Most have no medical exam. One requires full underwriting. Which one you land on depends on how you move through the application sections.

Terms available across the product line: 10, 20, 25, and 30 years depending on the plan. Issue ages vary by term length: 10-year terms to age 70, 20-year terms to age 60, 25-year terms to age 55.

Deferred Elite Term Insurance

For Canadians with health conditions or a previous decline. CPP’s entry point for harder-to-insure applicants.

- Coverage: $25,000 to $350,000

- Terms: 10 years (ages 18-70), 20 years (ages 18-60), 25 years (ages 18-55), 25-year decreasing (ages 18-60)

- Medical Underwriting: None

- Features: Level premiums, renewable to age 80, convertible to permanent insurance to age 70, accidental death and child term riders

Simplified Elite Term Insurance

For Canadians in average health or those in high-risk professions or hobbies. More coverage than Deferred Elite with the same no-exam process.

- Coverage: $25,000 to $500,000 (ages 18-60); up to $350,000 for ages 61-70 on 10-year term

- Terms: 10 years (ages 18-70), 20 years (ages 18-60), 25 years (ages 18-55), 25-year decreasing (ages 18-60)

- Medical Underwriting: None

- Features: Level premiums, renewable to age 80, convertible to permanent to age 70, accidental death and child term riders, hospital cash rider

Preferred Term Life Insurance

For applicants in good health who want higher coverage. No medical exam required for coverage up to $500,000 for applicants under age 70.

- Coverage: $50,000 to $1,000,000

- Terms: 10 years (ages 18-70), 20 years (ages 18-60), 25 years (ages 18-55), 25-year decreasing (ages 18-60)

- Medical Underwriting: None up to $500,000 (ages 18-70); paramedical and blood work required above $500,000

- Features: Level premiums, renewable to age 80, convertible to permanent to age 70, standard riders

Express Elite Term Insurance

For healthy applicants who want fast, affordable term coverage. No medical exam, same-day approval on many applications.

- Coverage: $100,000 to $750,000 (ages 18-50); $100,000 to $500,000 (ages 51-60) on T20 only

- Terms: T20 available ages 18-60; T30 available ages 18-50 only

- Medical Underwriting: None

- Features: Convertible to permanent insurance after two years, hospital cash rider, critical illness rider

Preferred Elite Term Insurance

The only CPP term product requiring full medical underwriting. For very healthy applicants who want maximum coverage and CPP’s best available rates.

- Coverage: $500,000 to $1,000,000

- Terms: 10 years (ages 18-70), 20 years (ages 18-60), 25 years (ages 18-55)

- Medical Underwriting: Yes, paramedical exam and blood work required in all cases

- Features: Level premiums, convertible to permanent to age 70, renewable to age 80, standard riders

CPP Permanent Life Insurance Options and Who Each Plan Suits

Canada Protection Plan offers six permanent life insurance products, most with no medical exam required. All are whole life policies paid to age 100, with cash value starting in year five on most plans. The right product depends on your health profile and how much coverage you need.

One important detail across the lower tiers: Guaranteed Acceptance and Deferred Life products carry a modified death benefit in the first two years. If the insured passes away from non-accidental causes within that window, the benefit is a return of premiums paid plus interest, not the full face amount. After two years, full coverage applies. Accidental death is covered in full from day one on all plans.

Guaranteed Acceptance Life

For applicants who cannot qualify for any other plan. No health questions, no medical exam, guaranteed approval.

- Coverage: $5,000 to $50,000 (ages 18-60); $5,000 to $50,000 (ages 61-75)

- Issue Ages: 18 to 75

- Medical Underwriting: None. All applicants accepted.

- Payment Options: Pay to age 100 only (monthly or annual)

- Features: Modified death benefit first two years (non-accidental), terminal illness benefit, transport benefit, optional accidental death rider, cash value from year five

Deferred Life

For applicants with diabetes, heart conditions, recent cancer, or other serious health history who don’t qualify for higher tiers.

- Coverage: $10,000 to $75,000 (ages 18-60); $5,000 to $50,000 (ages 61-80)

- Issue Ages: 18 to 80

- Medical Underwriting: None

- Payment Options: Pay to age 100 only (monthly or annual). 20-pay not available.

- Features: Modified death benefit first two years (non-accidental), cash value from year five, terminal illness benefit, transport benefit, optional accidental death rider

Deferred Elite Life

For applicants with less severe health conditions who want higher coverage than Deferred Life with a flexible payment structure.

- Coverage: $10,000 to $350,000 (ages 18-60); $5,000 to $350,000 (ages 61-80)

- Issue Ages: 18 to 80

- Medical Underwriting: None

- Payment Options: Pay to age 100 or 20-pay

- Features: Modified death benefit first two years (non-accidental), cash value from year five, terminal illness benefit, transport benefit, child term and accidental death riders

Simplified Elite Life

For applicants in reasonably good health, including those in high-risk occupations or with active lifestyles. Immediate full coverage from day one.

- Coverage: $10,000 to $500,000 (ages 18-60); $5,000 to $350,000 (ages 61-80)

- Issue Ages: 18 to 80

- Medical Underwriting: None

- Payment Options: Pay to age 100 or 20-pay

- Features: Full coverage from day one, cash value from year five, terminal illness benefit, transport benefit, optional hospital cash, child term, and accidental death riders

Preferred Life

For healthy applicants who want permanent coverage up to $1,000,000. No exam required up to $500,000 for applicants under age 70.

- Coverage: $50,000 to $1,000,000 (ages 18-80)

- Issue Ages: 18 to 80

- Medical Underwriting: None up to $500,000 (ages 18-70); paramedical and blood work required above $500,000 or ages 71-80

- Payment Options: Pay to age 100 or 20-pay

- Features: Full coverage from day one, cash value from year five, terminal illness benefit, transport benefit, multiple optional riders

Preferred Elite Life

CPP’s highest-tier permanent product. Full medical underwriting required in all cases. For very healthy applicants seeking maximum coverage and best available rates.

- Coverage: $500,000 to $1,000,000 (ages 18-80)

- Issue Ages: 18 to 80

- Medical Underwriting: Paramedical exam and blood work required in all cases

- Payment Options: Pay to age 100 or 20-pay

- Features: Full coverage from day one, cash value from year five, terminal illness benefit, transport benefit, optional hospital cash, child term, and accidental death riders

Term vs. Permanent: Which Is Right?

Both term and permanent options are available through CPP across most health tiers. The right choice depends on what you’re trying to protect and for how long.

| Feature | Term Life | Permanent Life |

|---|---|---|

| Coverage Duration | 10, 20, 25, or 30 years (30-year on Express Elite only) | Lifelong |

| Premiums | Lower upfront, rise upon renewal | Locked in for life |

| Cash Value | None | Builds from year five on most plans |

| Best For | Mortgage, income replacement, short-term debt | Final expenses, estate planning, lifelong coverage |

| Conversion Option | Yes, to permanent before age 70 on most plans | Not applicable |

Not sure which direction makes more sense for your situation? Get in touch and we can work through the numbers together.

How CPP Final Expense Insurance Works and Who It Makes Sense For

Final expense insurance covers the immediate costs that come when someone passes away: funeral services, burial or cremation, outstanding medical bills, and any final debts. It’s not income replacement. It’s a specific, practical tool to make sure the people left behind aren’t dealing with financial pressure on top of everything else.

CPP offers final expense coverage through their Guaranteed Acceptance Life and Deferred Life products. Coverage ranges from $5,000 up to $50,000 depending on the plan and age at application. No medical exam required. For Guaranteed Acceptance, there are no health questions at all. You can read more in our detailed guide to CPP final expense insurance.

This type of coverage makes the most sense for:

- Seniors who no longer need large life insurance policies but want final costs covered

- People with limited savings who don’t want to leave family with an unexpected bill

- Anyone with health conditions who can’t qualify for traditional coverage

- Applicants who have been declined elsewhere and need guaranteed acceptance

One thing worth knowing: Guaranteed Acceptance Life carries a modified benefit in the first two years. If death occurs from non-accidental causes within that window, the payout is a return of premiums plus interest rather than the full face amount. After two years, the full benefit applies. For clients who are older or in poor health, getting this coverage in place sooner rather than later is the practical move.

Critical Illness Coverage Through Canada Protection Plan

Beyond life insurance, CPP offers four critical illness insurance products. These pay a tax-free lump sum on diagnosis of a covered condition, with no requirement to prove lost income or medical costs. The money goes directly to you to use however you need.

What makes CPP’s critical illness lineup different from most carriers is the structure. Rather than bundling dozens of conditions into one policy, CPP separates cardiac and cancer coverage. That means a client with a history of heart disease can apply for cardiac coverage without being penalized for cancer risk, and vice versa. In some cases, clients can claim on both categories at different times.

- Cardiac Protect CI: Pays $10,000 to $50,000 on diagnosis of a heart attack, stroke, aortic surgery, coronary artery bypass, or heart valve replacement. Available to age 75.

- Cancer Protect CI: Pays $10,000 to $50,000 on diagnosis of cancer, aplastic anemia, or a benign brain tumour. Available to age 75.

- Cardiac and Cancer Protect CI: Combines both plans. If you claim on one, the other remains active with reduced premiums. Two separate potential payouts.

- Cardiac or Cancer Protect CI: Covers all listed conditions, but once you claim on one category the other is cancelled. Single payout structure.

All four plans are available without a medical exam for eligible applicants. Issue ages are 18 to 55 on most plans. These are particularly useful for clients with a family history of heart disease or cancer who want a financial buffer beyond their life insurance coverage.

")

CPP Product Comparison: Express, Simplified and Deferred

Here’s a summary of the four most commonly used CPP plans. Coverage amounts, ages, and health requirements vary by tier. The right fit depends on where you land in the application process.

Life Insurance Product Comparison

Coverage options and underwriting differences for Canadian applicants

| Product | Coverage Amount | Ages | Health Requirement | Approval Time | Ideal For |

|---|---|---|---|---|---|

| Express Elite | Up to $750,000 | 18–60 | Excellent health, short form | Same day | Healthy clients needing fast coverage |

| Simplified Elite | Up to $500,000 | 18–80 | Moderate conditions, no exam | 1–2 days | Clients with pre-existing conditions |

| Deferred Elite | $5,000 – $350,000 | 18–80 | Higher-risk or declined applicants | Few days | Hard-to-insure or recently declined |

| Guaranteed Acceptance | Up to $50,000 | 18–75 | No questions asked | 5–7 days | Terminal illness or very high-risk |

protectyourwealth.ca

How Canada Protection Plan Underwrites Health Conditions and Lifestyle Risks

CPP uses simplified health questionnaires rather than full medical underwriting, but applicants are still assessed on health, lifestyle, and behavioural risk. The questions are structured so that more serious conditions route to lower tiers automatically. Here’s how the most common categories are handled.

- Pre-existing Conditions: Conditions like diabetes, heart issues, and cancer history are not automatic declines. The application routes you to the appropriate tier based on severity and timeframe.

- Smoking and Tobacco: Any tobacco or nicotine use in the past 12 months triggers smoker rates. Marijuana is assessed separately: up to 5 times per week is classified as non-smoker on most A-Z products. CBD oil and edibles are excluded from the marijuana count entirely.

- Alcohol and Substance Use: Applicants in recovery may still qualify depending on time since treatment and stability. Recent active abuse typically routes to Guaranteed Acceptance only or results in a deferral.

- Mental Health: Depression, anxiety, and other mental health diagnoses are assessed based on hospitalization history in the past 12 months, medication stability, and whether any work has been missed. No hospitalization in the past 12 months generally keeps the application in Deferred Elite or higher.

- Occupational Risk: High-risk occupations including construction, mining, offshore work, and aviation are accepted on certain plans. The application asks for job duties, hours, and environment specifics to determine which tier applies.

- Foreign Travel: Travel outside North America, the Caribbean, the UK, the EU, Australia, or New Zealand for more than 12 consecutive weeks in the next 12 months can affect eligibility on higher tiers.

- Driving Record: A licence suspension within the past 2 years or more than 3 moving violations in the past 12 months affects Express Elite eligibility. A DUI within the past 24 months routes to Guaranteed Acceptance on A-Z products. Criminal convictions within the past 10 years route to Simplified Elite at most.

One thing CPP does that most traditional carriers don’t: they don’t ask whether you’ve ever been declined, rated, or postponed for life insurance. That application history stays off the table entirely.

How Common Health Conditions Are Routed at CPP

| Condition | Likely Tier | Notes |

|---|---|---|

| Diabetes (controlled, no complications) | Simplified Elite or Deferred Elite | Depends on type, medications, and time since diagnosis |

| Heart condition (stable, past 2+ years) | Deferred Elite or Simplified Elite | Type of event and time elapsed are key factors |

| Cancer (in remission 2+ years) | Deferred Elite or higher | Cancer type and treatment completion matter significantly |

| Recent cancer (within 12 months) | Deferred Life or Guaranteed Acceptance | Active treatment or recent diagnosis routes to lower tiers |

| High blood pressure (medicated, stable) | Simplified Elite or Preferred | Well-controlled hypertension rarely blocks higher tiers |

| Mental health (no hospitalization past 12 months) | Deferred Elite or higher | Stability and medication compliance are the key signals |

| Previous decline by another carrier | Deferred Elite or Guaranteed Acceptance | CPP does not ask about prior declines on simplified applications |

Tier outcomes are illustrative only and depend on the full application. Always work through the application with a licensed broker before assuming eligibility.

What Canadians Say About Canada Protection Plan

CPP’s Google reviews are generally positive for a life insurance carrier, particularly among clients who needed coverage quickly or had been declined elsewhere. Most positive feedback centres on three things: speed of approval, ease of application, and the fact that coverage was available when other carriers had said no.

The themes that come up consistently:

- Fast approvals and simple process: Clients regularly mention same-day or next-day approval, completing the application over the phone in under 30 minutes, and no invasive medical requirements. For clients who have been through lengthy traditional underwriting before, the contrast is significant.

- Coverage when nothing else worked: A recurring theme in reviews is clients who had been declined elsewhere finding a workable option through CPP. For many, it’s not about CPP being the cheapest option. It’s about CPP being the option that actually said yes. Learn more about when no medical life insurance makes sense.

- Pricing perception: Reviews are mixed on cost. Clients who came from a decline or a heavy rating elsewhere tend to view CPP’s pricing as fair. Clients who applied without a specific health reason sometimes find the premiums higher than expected compared to fully underwritten options.

Negative reviews are relatively rare but tend to focus on premium increases at renewal and confusion about the modified benefit period on lower-tier plans. Both are worth discussing upfront with a broker before applying.

Frequently Asked Questions: Canada Protection Plan

What is no medical life insurance?

No medical life insurance is coverage that skips the physical exam, blood work, and report from your doctor. You answer a short health questionnaire instead. It’s the right fit for Canadians with pre-existing conditions, previous declines, or anyone who needs coverage in place quickly. Learn more in our guide to no medical life insurance.

How long does approval take at Canada Protection Plan?

It depends on the plan. Express Elite applications are often approved the same day. Simplified Elite and Deferred Elite typically take 1 to 3 business days. Guaranteed Acceptance can take 5 to 7 days. None of these require a medical exam.

Can I get CPP life insurance with a pre-existing condition?

Yes. Most pre-existing conditions don’t disqualify you from CPP coverage. They determine which tier you qualify for. Conditions like controlled diabetes, heart history, or a previous cancer diagnosis may route you to Deferred Elite or Simplified Elite rather than the top tier, but coverage is almost always available. The application is structured so that everyone lands somewhere.

Does applying to CPP affect my chances with other carriers later?

No. A simplified or no-medical application through CPP does not generate the same kind of record that a full underwriting process does. Applying simplified first, getting covered, and then exploring fully underwritten options later is generally the safer sequence if there’s any uncertainty about how a medical would go.

Is Canada Protection Plan a legitimate insurance company?

Yes. CPP is underwritten by Foresters Life Insurance Company, which holds an “A” (Excellent) rating from AM Best and has been underwriting CPP products since 2008. All policies are protected by Assuris. CPP has been operating in Canada since 1992 and is one of the country’s best-known no-medical carriers.

Does CPP offer permanent life insurance?

Yes. CPP offers six permanent life insurance products including Guaranteed Acceptance Life, Deferred Life, Deferred Elite Life, Simplified Elite Life, Preferred Life, and Preferred Elite Life. All are whole life policies paid to age 100. Most build cash value starting in year five.

Can I convert my CPP term policy to permanent coverage?

Yes. Most CPP term policies can be converted to permanent coverage without underwriting, up to age 70. Conversion must happen no sooner than 60 days before the second policy anniversary. The 25-year decreasing term is not convertible. Express Elite can be converted after two years.

Find a Solution That’s Right for You

Canada Protection Plan is a strong option for the right client, but it’s not the right fit for everyone. If you’d like to understand whether CPP or another carrier makes more sense for your situation, we’re happy to work through it with you.

At Protect Your Wealth, we’ve been helping Canadians find the right life insurance coverage since 2007. As independent brokers, we compare CPP against every other simplified and fully underwritten option available, so you get the best fit for your health profile, budget, and coverage needs, not just the first product that says yes.

Contact us or call us at 1-877-654-6119. We’re based in Hamilton and work with clients across Alberta, British Columbia, Manitoba, Ontario, Saskatchewan, Nova Scotia, and New Brunswick, including areas such as Dundas, Burnaby, Lethbridge, and Vaughan.

{kind=link}