")

What is a Tax-Free Savings Account?

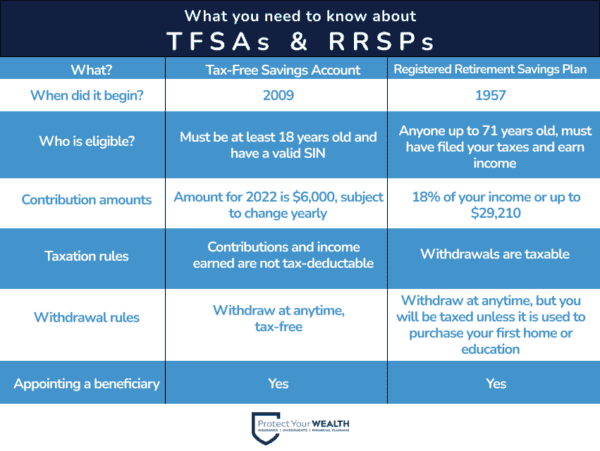

The Tax-Free Savings Account (TFSA) program began in 2009, it was introduced by the Canadian government as new kind of savings account to help residents of Canada with a Social Insurance Number (SIN) save money for various stages in their life.

The TFSA can hold various investment benefits, such as cash, stocks, bonds, GICs and mutual funds, the growth of which will not be tax-deductible.

Any contribution or any income earned in the account is generally tax-free, even when it is withdrawn. This is a great way to build you short term savings, long term savings or even an emergency fund. This is a must have savings account for all Canadians who are trying to build their financial security. Add this account to your financial plan, contact our team of financial experts and investment planners to open an account now.

Tax-Free Savings Account contribution limit for 2023

$6,500

Tax-Free Savings Account contribution limit for 2022

$6,000

What are the benefits of having a TFSA

With a TFSA you can set money aside and use it to invest in eligible investments, and your savings will grow tax-free! You can earn interest, dividends, and capital gains and if these are earned in a TFSA they are tax-free for life.

It is simple to withdrawal money from your TFSA amount at any time! Withdrawing from your account also has a tax-free withdrawal fee and you can put the money back into your account the next year to avoid impacts on your yearly contribution amount.

Tax-Free Savings Account cumulative total in 2023:

$88,000

| Year | TFSA Annual Contribution Limit | Total TFSA Limit (Cumulative) |

|---|---|---|

| 2009 | $5,000 | $5,000 |

| 2010 | $5,000 | $10,000 |

| 2011 | $5,000 | $15,000 |

| 2012 | $5,000 | $20,000 |

| 2013 | $5,500 | $25,500 |

| 2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016 | $5,500 | $46,500 |

| 2017 | $5,500 | $52,000 |

| 2018 | $5,500 | $57,500 |

| 2019 | $6,000 | $63,500 |

| 2020 | $6,000 | $69,500 |

| 2021 | $6,000 | $75,500 |

| 2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

Financial Institutions we work with

We proudly work with Canada’s largest financial institutions for your retirement planning & investment needs

Financial Institutions we work with

We proudly work with Canada’s largest financial institutions for your retirement planning & investment needs

Frequently Asked Questions (FAQs) About Tax-Free Savings Accounts (TFSAs)

The Tax-Free Savings Account (TFSA) program was introduced by the Canadian government in 2009. This program has been very successful and most financial institutions in Canada offer TFSA products and services to help you save for your future. The yearly contribution room has gone up and down, but is still continuing year after year since 2009.

A TFSA is simply a savings account. With that being said, it is up to you if you want to just put money aside in it and leave it at that, or if you want to pair it with various forms of investments which can provide growth, and have different levels of direction (investments managed by your or by your financial institution).

Yes! Tax-Free savings accounts are safe and a product offered by legitimate and credible financial institutions in Canada. The TFSA is one of the safest options for saving money for both short and long term financial plans. They have non tax-deductible features which makes the amount in your TFSA safe and secure from taxation. The TFSA is one of the best options for all Canadians to make for a safe and secure way to save.

Yes, a Tax-Free Savings Account (TFSA) is a great account for all Canadians to have. There are no fees for most TFSAs, there aren’t mandatory monthly deposits needed. A TFSA is an excellent account for all Canadians, even if they don’t have a clear savings goal in mind yet. The contribution room in your TFSA will grow if it is unused and not maxed out, therefore it will be ready for you when you want to start saving and using your TFSA. Starting a TFSA is a smart decision and is readily available. Contact a financial advisor now to learn how a TFSA will be right for you.

To be eligible to open a Tax-Free Savings Account (TFSA) in Canada, you must be a Canadian resident who is over 18 years of age, and you must have a valid Social Insurance Number (SIN). A non-resident of Canada who has a valid SIN is even eligible to have a TFSA but they will be subject to a 1% for each month their contributions stay in the account.

There are plenty of benefits to having a Tax-Free Savings Account, which is what makes it an account that every Canadian should have! These are just some of the key benefits of the TFSA:

- Tax-free withdrawals which will not affect your income tax or government benefits

- Easily access your money anytime, which makes a TFSA great for an emergency fund

- Capital gains, dividends and interest that are earned in your TFSA are 100% tax-free

- Withdrawals from your TFSA do not affect government benefits, such as the Old-Age Security (OAS) benefit or Child Tax Benefit.

- You can have a beneficiary for your TFSA, thus making it a useful account for estate planning. Many life insurance companies also allow you to appoint a beneficiary for your TFSA as well.

- The TFSA is a great vehicle for investments, whether it is a GIC or a mutual fund.

A tax-free savings account earns interest! This is one of the most beneficial parts of a TFSA and this interest can vary depending on the investments you hold in the TFSA. This interest can be earned monthly depending on the type of TFSA and the bank you go with.

This breaks down to the yearly contribution amount, as well as the cumulative contribution amount.

- Cumulative TFSA room

- This all depends on what age you were in 2009. If you were age 18 or older in 2009, then in 2022 your TFSA is eligible for a lifetime accumulation of $81,500. For example, if you turned 18 in 2016 and you don’t have a TFSA, you’re eligible for $40,500 in lifetime cumulative contributions.

- Yearly TFSA room

- You are only eligible for a certain amount of contributions in your TFSA yearly, this amount can change year by year. For 2022, the maximum contribution amount for the year is $6,000. If you do not contribute the entire $6,000 to your TFSA this year, or make withdrawals from your TFSA, that contribution room will get carried over to the next year. Please refer to our graph to see the yearly contribution amounts since 2009.

- Cumulative TFSA room

| Year | TFSA Annual Contribute Limit | Total TFSA Limit (Cumulative) |

|---|---|---|

| 2009 | $5,000 | $5,000 |

| 2010 | $5,000 | $10,000 |

| 2011 | $5,000 | $15,000 |

| 2012 | $5,000 | $20,000 |

| 2013 | $5,500 | $25,500 |

| 2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016 | $5,500 | $46,500 |

| 2017 | $5,500 | $52,000 |

| 2018 | $5,500 | $57,500 |

| 2019 | $6,000 | $63,500 |

| 2020 | $6,000 | $69,500 |

| 2021 | $6,000 | $75,500 |

| 2022 | $6,000 | $81,500 |

You may have as many TFSAs as you want, but keep in mind the total contribution amount you contribute to all your TFSAs cannot be more than your available TFSA contribution room for the year.

This depends on the room you have in your TFSA based on both your age and how much room you have for that year, also if you have made deposits or withdrawals from your TFSA already. Refer to our table showing the yearly contribution amounts from 2009 to 2022.

Both are great savings accounts but there are multiple pros and cons for both and it really depends on your financial plan. They both offer great growth opportunities and are a really beneficial investment for saving. To simplify this: if you are saving for your retirement, for a house, or for any long term financial goal, an RRSP might be better for you. If you are saving for a short term financial goal, such as buying a car, going on a vacation, or another short term financial goal, then a TFSA might be right for you. Again, both are great for financial goals, and both can be effective for short and long-term goals, it just depends on you. It is strongly recommended to speak to a financial advisor before opening a TFSA or an RRSP to find out what is best suited for you, we off free consultations to discuss the right financial plan for you.

Here is a comparison to give you some basic information about TFSAs and RRSPs:

A Tax-Free Savings Account can hold these investments: cash, guaranteed investment certificates (GICs), bonds, stocks, exchange-traded funds (ETFs), mutual funds and options.

No, the contributions you make to your TFSA are not tax deductible. Income earned in the TFSA, including any capital gains, investments or interest, are also generally not tax deductible. Even administrative fees or borrowed amounts for your TFSA are not tax deductible.

No, you won’t pay income tax on withdrawal from your TFSA. TFSA withdrawals don’t count as taxable income and do not affect government benefits, including the Canada Child Benefit program, the Good and Services Tax/Harmonized Sales Tax (GST/HST) Credit, and the Age Credit. TFSA withdrawals will not affect benefits that are based on your income like Old Age Security, the Guaranteed Income Supplement and Employment Insurance benefits.

No, currently you can’t have a joint TFSA. One person can only hold A TFSA, therefore you and your spouse can open your own individual accounts.

Yes, even permanent residents and immigrants can open a TFSA. The only requirements to open a TFSA are to be over 18 years of age and have a valid social insurance number.

Yes, you can have a beneficiary for your TFSA. In fact, many life insurance companies also allow you to appoint a beneficiary for your TFSA as well.

The 5 Steps of Successful Financial Planning

An overview of 5 wealth-planning steps Protect Your Wealth takes that results in a strong financial future.

1.

Gather and AnalyzeAt Protect Your Wealth, we will work with you to create an accurate overview of your present financial situation. Using state-of-the-art software, we will complete a thorough needs analysis to assess your present expenses and project future ones while accounting for inflation. We also perform a detailed risk assessment to help ensure that you are not taking more risk in your investments than necessary.

2.

Develop Your Blueprint for SuccessAfter carefully considering all aspects of your finances and identifying ways to maximize tax efficiency, we will recommend an efficient retirement savings plan that tallies with your investment goals. You will receive a personalized Investment Policy Statement that summarizes our findings and recommends appropriate risk-managed investment options.

3.

Strategize and Implement Your PlanAfter you approve your Investment policy statement, we will present you with a Financial Planning Priorities and Strategies document outlines your financial planning priorities and your personalized wealth-building strategies that meet both your short, and long-term financial goals. Once you review and approve your plan, it will be implemented. It is important to note that this document will change over time to ensure that it always reflects your current circumstances and complies with any changes in government policy.

4.

Forecast Your Financial FutureWe use a cash flow planning analysis to create a financial forecast of your future. This analysis calculates projected outcomes, which lets you consider the consequences of financial decisions before you make them and create a stronger plan for future commitments like a child’s college fund. These forecasts are reviewed every year as your situation changes.

5.

Ongoing Monitoring and ManagementFinancial planning is a continuous process. To ensure that your investment needs continue to be met, we will remain in regular contact with you throughout the year and hold a yearly review to assess progress, make adjustments for changed circumstances, and evaluate promising new strategies. These meetings may be held in our office, by phone, or via Zoom.