Top 5 No Medical Life Insurance Plans in Canada

The first question isn’t which no medical product to choose. It’s whether you should be in this category at all.

Parvesh Benning, Licensed Life Insurance Broker · Serving Canadians since 2007

No medical life insurance gives Canadians who can’t easily get fully-underwritten coverage another path to family protection. Some applicants need it because of health concerns, occupation risk, or a recent decline. Others land here without realizing fully-underwritten coverage at standard rates was already available, which is the first thing a broker should check before recommending any product on this list.

Updated: May 6, 2026

Top 5 No Medical Life Insurance Plans in Canada

The first question isn’t which no medical product to choose. It’s whether you should be in this category at all.

Parvesh Benning, Licensed Life Insurance Broker · Serving Canadians since 2007

No medical life insurance gives Canadians who can’t easily get fully-underwritten coverage another path to family protection. Some applicants need it because of health concerns, occupation risk, or a recent decline. Others land here without realizing fully-underwritten coverage at standard rates was already available, which is the first thing a broker should check before recommending any product on this list.

Updated: May 6, 2026

No medical life insurance gives Canadians who can’t easily get fully-underwritten coverage another path to family protection. Some applicants need it because of health concerns, occupation risk, or a recent decline. Others land here without realizing fully-underwritten coverage at standard rates was already available, which is the first thing a broker should check before recommending any product on this list.

This guide covers the five no medical and accelerated-underwriting paths a Canadian broker actually uses, what each one costs at typical age and coverage profiles, and how to think about whether you need a no medical product at all or whether fully-underwritten coverage at standard rates would serve you better.

Five no medical paths covered in this guide

Tap any carrier name to jump to the full section. Three of these five plans accept applications up to age 75 or 80, so older applicants and Canadians with health concerns are not limited to one option.

RBC YourTerm with Express Underwriting

Healthy applicants up to age 50 can qualify for up to $2 million with no medical exams, no tele-interview, and instant approval. Fast issue at standard fully-underwritten rates.

Sun Life Term with Non-Paramedical Pathway

Brand-name term insurance with no paramedical exam required. Available up to $1 million for ages 18 to 50, and up to $500,000 for ages 51 to 70.

Assumption Life Platinum Protection Term

Highest simplified-issue coverage cap on this list. Up to $750,000 for ages 18 to 50 and up to $500,000 for ages 51 to 75. Day-one coverage with 19 health questions.

Canada Protection Plan Simplified Elite Term

Term lengths of 10, 20, or 25 years depending on issue age. Day-one coverage with 13 health questions. Issue ages run 18 to 70 on the 10-year plan and 18 to 60 on the 20-year plan.

Issue ages from 6 months to 80. The four-step model accepts a wider range of health profiles than other simplified products. Step 1 is true guaranteed acceptance with no health questions, capped at $50,000 for healthy adults under 50.

What’s inside:

- How no medical life insurance works in Canada

- How a broker routes no medical applications across these 5 carriers

- Canada Protection Plan (CPP) Simplified Elite Term

- Sun Life Term with non-medical pathway

- RBC YourTerm with Express underwriting

- Assumption Life Platinum Protection Term

- iA Access Life

- Frequently asked questions

How no medical life insurance works in Canada

No medical life insurance is a category that covers three different underwriting approaches. The shared feature is that no paramedical exam is required at application time. The differences underneath that surface determine cost, coverage limits, and how soon coverage actually pays out at claim.

The advantage is access. Applicants who would be declined or postponed under fully underwritten policies because of health, occupation, or extreme activity risks can still get coverage. Some carriers also offer non-medical pathways inside their standard term products, which means a healthy applicant can skip the paramedical exam without paying a simplified-issue premium markup.

The trade-off is cost and coverage limits. Simplified-issue and guaranteed-issue premiums typically run about 50% higher than fully underwritten standard rates, with 10 to 20% being the low end on the cheapest simplified products. Most simplified carriers also cap face amounts between $500,000 and $750,000.

Accelerated underwriting from major carriers splits the difference. Standard fully-underwritten pricing, no paramedical for healthy applicants who meet the carrier’s eligibility window. The five plans below span all three categories.

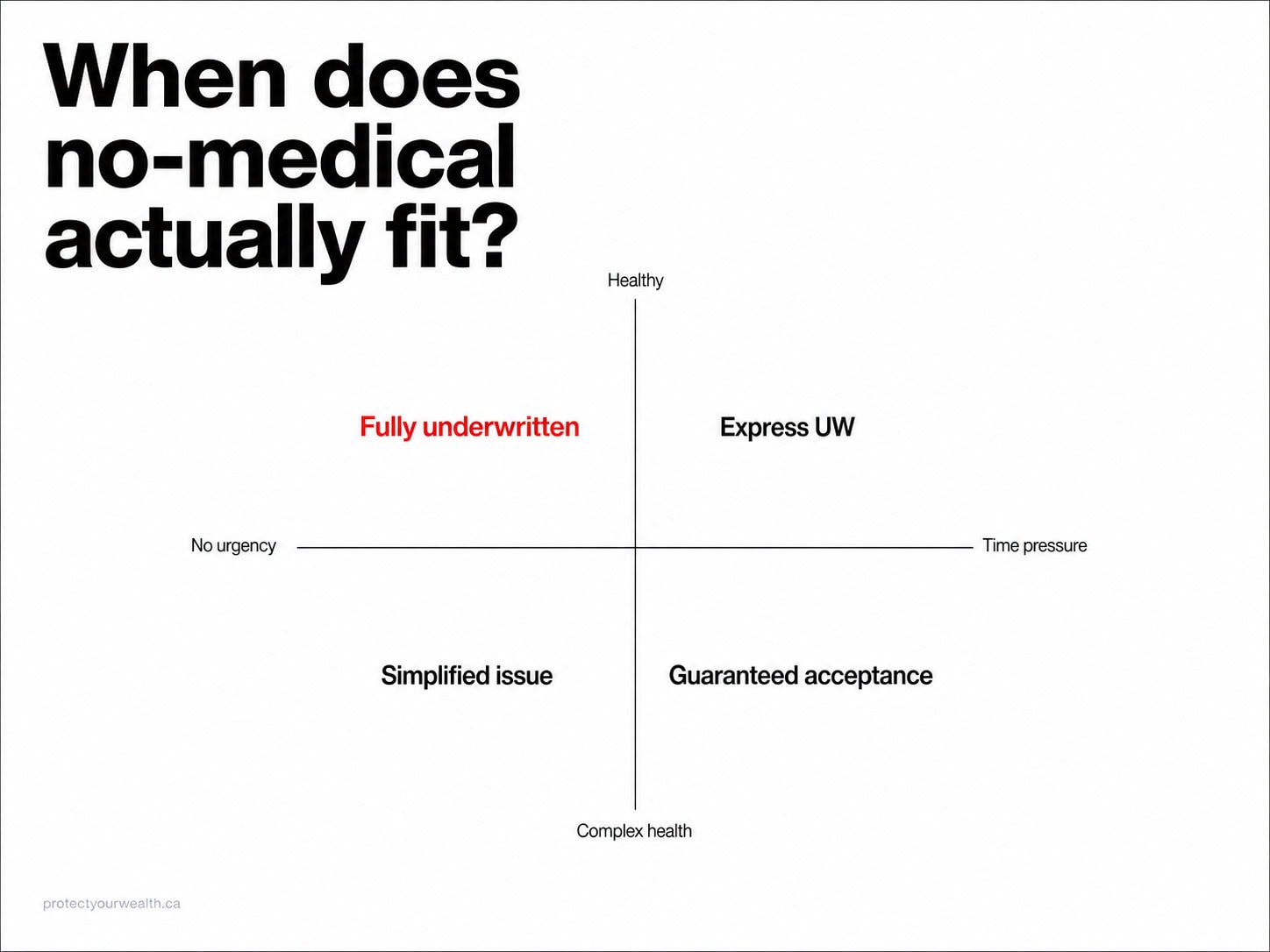

Who Actually Needs No-Medical Life Insurance?

No medical life insurance is usually worth considering when a client has a health history, occupation risk, travel concern, recent decline, or urgent deadline that makes regular fully-underwritten coverage harder to place. It can also help when coverage needs to be issued quickly and there is no time to wait for medical evidence, lab work, or attending physician statements.

That said, no-medical coverage should not be the default starting point for every applicant. Many Canadians with controlled conditions, stable medication, clean follow-up, and no major complications may still qualify for standard fully-underwritten rates. A broker should check that path first before recommending a simplified-issue or guaranteed-issue product.

Simplified vs Guaranteed Issue: Which Type Each Plan Falls Under

Most readers searching for no medical insurance assume there is one product category. There are three, and the five plans on this list span all of them. Knowing which one a plan belongs to changes how its price compares against fully underwritten coverage and what happens at claim time.

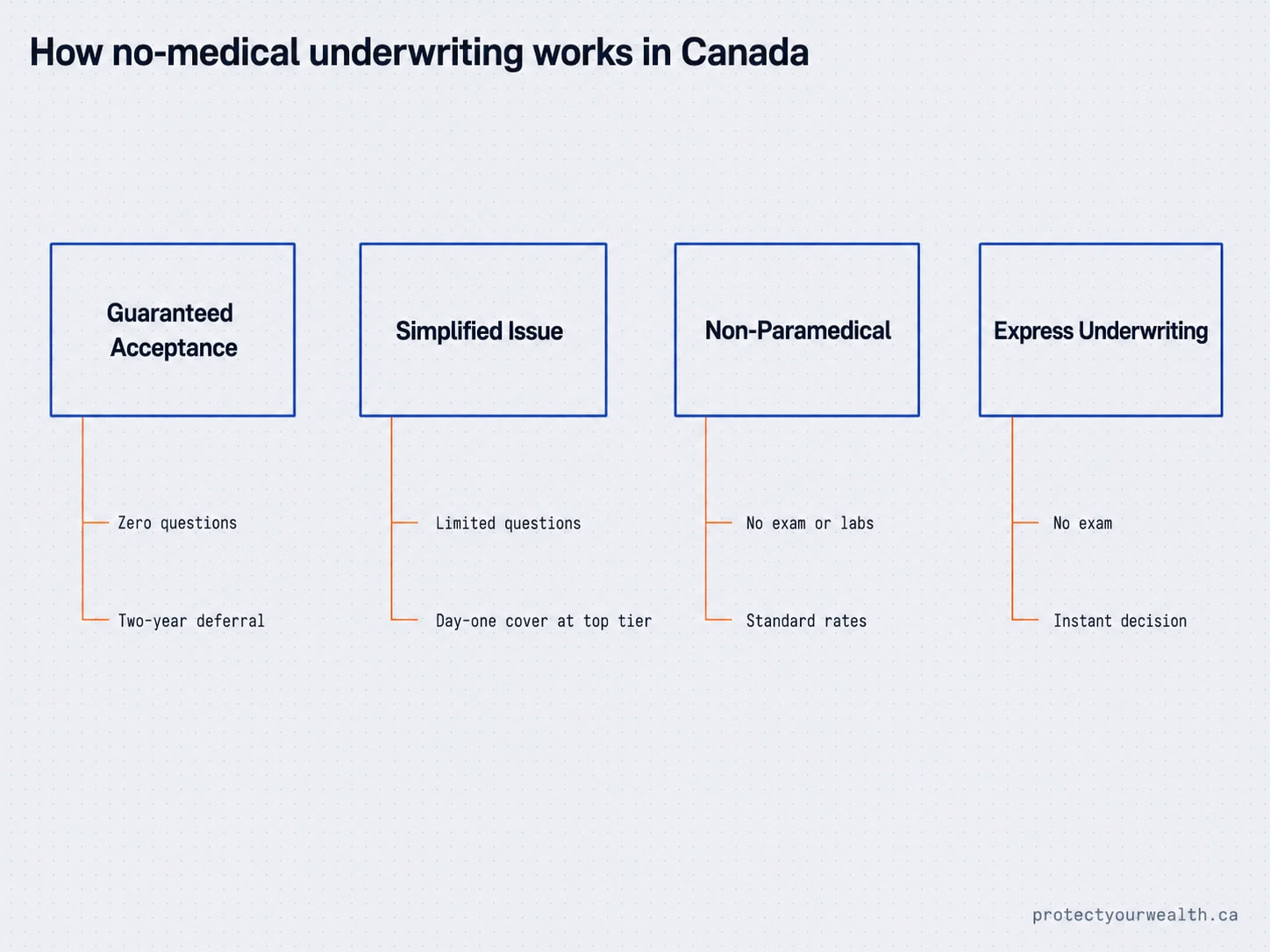

Type 01 · Simplified issue

Health questions, no exam, day-one coverage

The application asks a series of health questions but no medical exam or paramedical visit is required. Coverage starts day one for healthy applicants who clear the questions. There is no waiting period at claim.

Type 02 · Guaranteed issue

No questions, two-year deferral on natural-cause claims

The application asks no health questions at all. The trade-off is a deferral period (typically two years) during which non-accidental death pays back premiums plus modest interest rather than the full face amount. Accidental death pays the full amount from day one.

A full breakdown of the three underwriting categories covers this in more detail.

Type 03 · Accelerated underwriting

Standard rates, no paramedical for qualifying applicants

A non-medical path inside fully underwritten products. The applicant answers a health and lifestyle questionnaire instead of a paramedical exam. Day one coverage. Standard rates. Available only to applicants who fit the carrier’s risk profile for the requested face amount.

How each plan maps to the categories

Some carriers route across multiple types within a single application. Others have lineups that span all three.

Fully underwritten product. No paramedical at standard class for healthy applicants up to $2M.

Fully underwritten product. No paramedical at standard class for healthy applicants up to $1M, ages 18 to 50.

Sections A through D route applicants between simplified issue and guaranteed acceptance within a single application. CPP Express Elite Term is the carrier’s separate accelerated-underwriting pathway.

Platinum Protection Term is simplified issue with tiered question routing across Silver, Golden, and Platinum levels. Assumption’s broader lineup also covers accelerated underwriting and guaranteed acceptance products.

Step 1 is guaranteed acceptance with a two-year deferral. Steps 2 to 4 are simplified issue with progressive question counts of 5, 9, and 13.

How a broker routes no medical applications across these 5 carriers

When someone calls me about no medical insurance and tells me they have controlled blood pressure on stable medication, a hazardous occupation that previously triggered a postponement, or some other manageable concern, my goal is to align the product solution with the best in market based on premium, underwriting, and conversion options. None of those concerns would automatically eliminate standard fully-underwritten coverage or access to competitive market pricing. MIB does not drive the decision in that kind of file. The client should usually be assessed first for standard fully-underwritten coverage, because controlled blood pressure on stable medication does not automatically make someone a no-medical applicant.

The first question isn’t “which no medical product?” It’s “do you need to be in this category at all?”

Two situations where simplified or accelerated underwriting earns its place

Reason 01

Speed, not health

A client needed $500,000 in place same-day for a collateral loan assignment. We placed a Beneva policy in under 60 minutes, written and issued. RBC YourTerm, Canada Life, and Empire Life now offer instant approvals on standard underwriting with policy and documents produced in under 24 hours.

Reason 02

Coverage exceeds a single simplified cap

When pre-existing health concerns are genuine and coverage need exceeds what one simplified carrier will issue. Most cap between $500,000 and $750,000 per insured. I have placed $1.5 million by stacking three simplified plans together. You can have more than one policy.

Speed varies by carrier and is constantly improving, so the right answer at any given moment depends on who can actually deliver in your timeframe. I have also revisited stacked simplified plans later when time allowed and replaced them with better-priced coverage.

When the choice is genuinely between simplified-issue carriers, here is the decision tree I work with

Assumption

Platinum Protection Term

Wins on

Coverage cap and price.

Goes to $750,000 and typically prices lower than the others at simplified-issue rates.

Canada Protection Plan

Simplified Elite Term

Wins on

25-year term availability.

The others don’t offer that length. CPP also tends to come out cheaper on Term to 100 and on permanent whole life.

iA

Access Life

Wins on

Complex health situations.

Questions tend to be more lenient, and the four-step model routes the application to the highest tier the client can clear.

The form does most of the routing on simplified products. Block by block, the longer the application can answer “no,” the better the tier and price the client lands on. What the form can’t do is decide whether to use simplified at all. That part is a broker call, and it depends on what the client actually needs and what the alternatives look like.

Canada Protection Plan (CPP) Simplified Elite Term

Canada Protection Plan is the most established no medical specialist in the Canadian market, owned by Foresters Financial. Simplified Elite is the top tier of CPP’s simplified-issue line and the only tier that pays the full death benefit from day one with no claim deferral. Healthy applicants who clear all sections of the application land here directly.

Senior eligibility note. Of the three CPP Simplified Elite term lengths, the 10-year term is the only one that issues past age 60. It runs to age 70. The 20-year term caps at age 60 and the 25-year term caps at age 55. Coverage maximum drops to $350,000 for ages 61 to 80.

How the CPP application routes you

The application is structured in blocks. Each section the applicant clears (answering “no” to all questions in that section) opens access to a higher product tier with better coverage and pricing. The form does the routing automatically based on what the applicant discloses.

Section A clears → Application advances to the next block. A “yes” in Section A routes to Guaranteed Acceptance Life ($50,000 cap, two-year claim deferral).

Section A + B clears → A “yes” in B lands at Deferred Life.

Sections A + B + C clear → A “yes” in C lands at Deferred Elite.

All four sections clear → Application reaches Simplified Elite, the top tier with full immediate coverage.

Simplified Elite Term at a glance

- Coverage amount: $25,000 minimum. Up to $500,000 combined across the Simplified Elite plan category for ages 18 to 60. Drops to $350,000 for ages 61 to 80.

- Term lengths and issue ages: 10-year term, ages 18 to 70. 20-year term, ages 18 to 60. 25-year term, ages 18 to 55.

- Renewable: To age 80.

- Convertible: To permanent life insurance (Term to 100 or whole life) until age 70 without new health evidence.

The reason to look at this product first is two specific scenarios. First, when a 25-year term length is on the table, since CPP and iA are the only two carriers on this list offering that length. Second, when a future conversion to permanent coverage is part of the plan. CPP’s pricing on Term to 100 and on permanent whole life conversions from this product tends to land below comparable simplified-issue competitors.

Sun Life Term with Non-Medical Pathway

Sun Life is the major-carrier exception on this list. Four of the five products covered here are simplified-issue policies; Sun Life is fully underwritten. Through the broker channel and the Sun eApp electronic application, healthy applicants can complete a brand-name term policy without a paramedical exam, without blood work, and without urinalysis. The result is standard fully-underwritten rates with immediate full coverage from day one.

This is almost always a better outcome than a true simplified-issue product when the option is available. Standard fully-underwritten rates typically run about 50% lower than simplified-issue rates for the same coverage and term length. The convenience of skipping the medical pieces is the headline benefit. The rate difference is the real one.

Non-paramedical thresholds at standard class. Ages 18 to 50 qualify for up to $1,000,000 with no paramedical and no labs. Ages 51 to 60 qualify for up to $500,000 on the same terms. Ages 61 to 70 qualify for up to $100,000 without labs. Above those amounts a tele-interview steps in for additional underwriting verification.

The catch is risk class. The non-paramedical pathway is standard class only. Applicants who would qualify for preferred or optimum non-smoker classes still need the paramedical exam and labs to access those better rates. The path works best for applicants who fit standard class anyway, or for applicants whose blood work might come back close to the preferred threshold and who would rather lock in standard rates without the lab risk.

Where this matters most is the older end of the issue age range. A 58-year-old healthy applicant looking for $500,000 of 20-year term can complete the application without scheduling a paramedical, fasting for blood work, or coordinating multiple medical appointments. That convenience matters more at 58 than at 35, which is why this pathway is one of the stronger options on this list for applicants in their fifties and early sixties.

One clarification on the Sun Life product line. Sun Life Go is a separate direct-to-consumer simplified-issue product available outside the broker channel. This post covers Sun Life’s broker-channel term insurance with the non-paramedical pathway, which is the better fit for most healthy applicants comparing options across a range of carriers.

RBC YourTerm with Express Underwriting

Express Underwriting is the broader system inside RBC Insurance, and it changes the application math for term insurance at every age band. The Team itself launched in November 2023 to cut underwriting cycle times in half on standard term applications. In December 2024, RBC extended the program to deliver instant point-of-sale approval for healthy applicants 50 and under, up to $2 million in coverage, with no medical exam, no labs, and no tele-interview, subject to RBC’s current underwriting rules and automated risk scoring. Both pieces apply, and the older-applicant value gets missed if you only read the headline.

Instant pathway: ages 50 and under

$2M

Instant approval threshold

$3M

No medicals ceiling

Zero

Exams, fluids, or interviews

5 days

Express Team turnaround

At or below $2 million, RBC’s automated risk scoring runs the application at submission and the decision lands instantly. Between $2 million and $3 million, no medical evidence is required, but the file goes through Express Team underwriting review with a turnaround of five business days or less. Above $3 million, or where automated scoring flags the file for additional review, standard underwriting applies with paramedical and labs.

For applicants over 50

The Express Team continues to handle applications past age 50, just on different mechanics. Standard underwriting requirements apply at the age and amount bands where RBC’s matrix calls for paramedical and labs, but the Express Team cuts the cycle time in half versus traditional file routing. A 58-year-old applying for $500,000 of 20-year coverage still completes the Health & Lifestyle Questionnaire on the application, still goes through paramedical and labs at that age and amount, but the file is processed through the Express Team rather than standard new business and the policy issues materially faster.

The cost case at the older end of the under-50 window: a 50-year-old healthy male non-smoker can secure $100,000 of 10-year coverage for approximately $22.68 per month; a female non-smoker on the same profile pays approximately $18.14 per month. Standard fully-underwritten rates, instant approval, documents in five days. The same age 50 client at higher amounts up to $2 million still falls inside the instant approval window provided the application clears.

Eligibility caveats. Express UW pathways issue at standard class only. Applicants who would qualify for preferred or optimum non-smoker classes still need full underwriting (paramedical and labs) to access those better rates regardless of age. Express UW also assumes the applicant clears RBC’s automated risk-scoring at point-of-sale; files flagged for review move to underwriter assessment, still inside Express Team handling, but no longer instant.

The product earns its position on this list because it removes friction from term insurance for the broadest age range of any major-carrier offering currently in market. Healthy under-50 applicants get instant brand-name coverage. Older applicants get faster turnaround through the same team handling the file. The trade-off everywhere is class: standard rates only on the express path. Whether to take that trade depends on whether the applicant would test into preferred class anyway, which is a broker conversation worth having before committing to the express route.

Product specs in brief. Coverage from $100,000 to $25,000,000. Term lengths from 10 to 40 years, customizable in one-year increments. Issue ages 18 to 70 on terms 10-15; for terms 16-40, maximum issue age = 85 minus selected term length. Convertible to permanent coverage until age 71 without new health evidence.

Assumption Life Platinum Protection Term

Assumption Life is a New Brunswick-based mutual carrier with the broadest age range of any simplified-issue option in this guide. Platinum Protection Term carries the highest simplified-issue coverage cap at $750,000 for ages 18 to 50 and $500,000 for ages 51 to 75, and on the rate samples reviewed for this guide, prices below CPP and iA on directly comparable simplified-issue applications. Pricing varies by age, sex, smoker status, term length, and coverage amount, so a broker comparison is the only reliable way to confirm the carrier ranking on a specific profile. Coverage starts day one with no claim deferral. For applicants over the term cutoff at 75, the same carrier and the same 19-question screen issue Platinum Protection Whole Life all the way to age 85.

The application uses a 19-question screen that progressively determines which product in Assumption’s simplified-issue lineup the applicant qualifies for. Answering “yes” at any block reroutes the file to a different product within the same family rather than producing a decline. Clearing all 19 reaches Platinum Protection Term (or Whole Life depending on age band) with the full benefit.

Questions 1 to 9. Establishes baseline eligibility for any Assumption simplified-issue product. The block covers build per the height-weight table, hospital admissions in the last 12 months, pending medical tests or investigations, terminal illness diagnoses, and similar high-severity criteria. Failing this block routes the application to Bronze Protection guaranteed-issue whole life (ages 18 to 80), which carries a two-year claim deferral.

Questions 10 to 13. Adds four screening questions covering moderate health conditions, recent hospitalizations, and disability status. Clearing this block keeps Golden Protection Term or Whole Life available, which is the same product family with day-one coverage but a $250,000 cap on the term version.

Questions 14 to 19. Adds six questions covering smoking history, occupation, build details, and lifestyle factors. Clearing all 19 places the applicant at Platinum Protection with the full $750,000 coverage cap and the lowest pricing tier on the simplified-issue product line.

The reason to look at Assumption first on a simplified-issue file is price. A 45-year-old healthy male non-smoker can secure $250,000 of 20-year Platinum Protection Term coverage for approximately $60.98 per month. CPP Simplified Elite at the same profile runs about $69 monthly. iA Access Life Immediate Plus at the same profile runs about $74. The advantage applies specifically to simplified-issue term; it narrows or reverses on permanent products, where CPP often comes out ahead.

The second reason is the renewable and convertible window. Platinum Protection Term renews annually to age 90, the latest of any product on this list. The conversion option to permanent coverage runs to age 75 without new health evidence. For applicants in their fifties or sixties weighing simplified-issue against the cost of fully-underwritten coverage, Assumption holds doors open longer than the other simplified options here.

For applicants over 75

Term coverage at Assumption stops at age 75 on the 10-year term and 70 on the 20-year. Above those ages, the same carrier and the same 19-question screen issue Platinum Protection Whole Life through age 85, Golden Protection Whole Life through age 85, Silver Protection Whole Life (graded death benefit) through age 85, or Bronze Protection guaranteed-issue whole life through age 80. Of the five carriers in this guide, Assumption serves the broadest age range and is generally the simplified-issue carrier of choice for applicants in their late seventies and early eighties looking for permanent coverage rather than term.

For a broker-routed simplified-issue file under 75, Assumption is often the first quote pulled on a term application based on rate samples at common applicant profiles. CPP enters when the applicant wants a 25-year term length or when permanent conversion from a term policy is part of the plan. iA Access Life enters when health concerns push the applicant out of Platinum tier and a more lenient question set is needed. Final carrier selection always depends on quoting the specific profile against all three.

- Coverage

- $50,000 minimum for ages 18 to 44, $25,000 minimum for ages 45 to 75. Maximum $750,000 for ages 18 to 50, $500,000 for ages 51 to 75.

- Term lengths

- 10 years, issued ages 18 to 75. 20 years, issued ages 18 to 70.

- Renewable and convertible

- Renewable annually to age 90. Convertible to permanent coverage until age 75 without new health evidence.

- Whole life option (over 75)

- Platinum, Golden, and Silver Protection Whole Life issue to age 85. Bronze Protection guaranteed-issue WL issues to age 80. Same simplified-issue screen, same carrier, no medical exam.

- Annual policy fee

- $60

iA Access Life

iA Access Life is the most flexible question structure on this list and the only product that handles complex health profiles inside a single application form. The product issues from age 6 months to 80 and runs four progressive eligibility steps. Step 1 is true guaranteed acceptance with zero health questions. Steps 2 through 4 add progressive question sets that determine coverage caps and whether claim deferral applies. The applicant lands at the highest step their disclosures support, with no formal decline.

The four steps progressively expand coverage and remove waiting periods. Most broker-routed iA Access applications land at Step 3 or Step 4 because the question screens at those tiers tend to be more lenient than what Assumption or CPP would require for comparable face amounts. The trade-off is price: iA Access carries the highest simplified-issue rates of the three carriers in this guide.

Step 1Guaranteed Access

Zero health questions. Pure guaranteed acceptance. Day-one accidental death pays the full benefit; non-accidental death during the first two policy years returns premiums paid with no interest. Years three and beyond pay the full benefit on any cause of death.

Coverage caps: $50,000 ages 18-50, $25,000 ages 51 and over, $10,000 under 18. Permanent (L100) plan only.

Step 2Deferred

Five health questions covering heart failure, stroke with permanent effects, kidney dialysis, oxygen therapy, and liver cirrhosis. Two-year claim deferral on non-accidental death; premiums returned plus 3% interest if a claim falls inside the deferral window.

Coverage caps: $100,000 ages 18-70, $50,000 ages 71 and over, $25,000 under 18. Permanent (L100) plan only.

Step 3Deferred Plus

Adds four questions to Step 2: cancer or melanoma diagnosed in the past 3 years, heart attack or bypass surgery in the past 3 years, insulin-dependent diabetes diagnosed before age 18, and HIV or AIDS. Two-year claim deferral with premiums returned plus 3% interest.

Coverage caps: $350,000 ages 18-70, $150,000 ages 71 and over, $25,000 under 18. Plans: L100, T15, T20, T25.

Step 4Immediate Plus

Adds four questions to Step 3: cancer diagnosed in the past 5 years, cardiac events in the past 5 years, complications from diabetes, and Alzheimer’s or dementia. Full immediate coverage with no claim deferral, the only iA Access tier that pays full benefit from day one on any cause of death.

Coverage caps: $500,000 ages 18-70, $150,000 ages 71 and over, $25,000 under 18. Plans: L100, T15, T20, T25.

The pricing on iA Access reflects the question leniency. A 45-year-old healthy male non-smoker pays approximately $73.65 per month for $250,000 of 20-year Immediate Plus coverage, the highest of the three simplified-issue carriers in this guide. Assumption Platinum runs about $61 monthly at the same profile. CPP Simplified Elite runs about $69. The price premium buys the lenient question set; for an applicant whose health history fails Assumption’s later screens or CPP’s Section D, iA’s Step 3 or Step 4 may be the only path to immediate-coverage simplified-issue at $350,000 or below.

One important caveat: the maximum face amount applies as a combined limit across all iA simplified-issue products. An applicant who already holds $200,000 of iA Access has the available cap reduced by that amount on a new application, regardless of which step the new application qualifies for.

For a broker-routed simplified-issue file where the applicant has multiple health concerns, recent hospitalizations, or anything that complicates Assumption’s 19-question screen or CPP’s Section D underwriting, iA Access Life is the alternative that keeps the file in immediate-coverage territory at Step 4. For applicants over 70 looking for small amounts of coverage, Step 1 Guaranteed Access at the $25,000 cap remains a reliable fallback when health rules out higher tiers, and Step 4 still issues to age 70 with up to $150,000 of immediate coverage at age 71 and beyond.

Product specs in brief. Issue ages 6 months to 80. Permanent option (L100) issues across all four steps. Term lengths of 15, 20, and 25 years issue at Steps 3 and 4 only, with maximum issue ages of 65, 60, and 55 respectively. Combined maximum face amount of $500,000 across all iA simplified-issue products held by the same insured.

Frequently Asked Questions About No Medical Life Insurance

1.What is no medical life insurance?

No medical life insurance is any life insurance product that doesn’t require a paramedical exam at application time. The category covers three distinct underwriting approaches: simplified issue (a question-only application with day-one coverage), guaranteed issue (no health questions but a two-year claim deferral), and accelerated underwriting (a non-paramedical pathway inside fully underwritten products at standard rates). The five products covered in this guide span all three categories.

2.What is the difference between no-medical and traditional life insurance?

Traditional life insurance is fully underwritten. An applicant completes an application, undergoes a paramedical exam, provides blood and urine samples, and sometimes the carrier requests medical records from the applicant’s doctor. The full process can take 4 to 8 weeks. No medical life insurance skips the paramedical and labs entirely; some no medical products still ask health questions (simplified issue), some ask none (guaranteed issue). The trade-off is speed and convenience against lower premiums and higher coverage caps, which traditional underwriting tends to deliver for healthy applicants.

3.Why are no medical premiums higher than fully-underwritten?

The carrier has less information about the applicant’s health profile, so the risk is priced higher to compensate. Simplified-issue and guaranteed-issue premiums typically run about 50% higher than fully-underwritten standard rates for the same coverage and term length, with 10 to 20% being the low end on the cheapest simplified products. Accelerated underwriting from major carriers like RBC and Sun Life closes that gap entirely because the rate class on the issued policy is the same as fully-underwritten standard, just without the paramedical exam.

4.Which no medical life insurance company is best in Canada?

The best fit depends on what is driving the application. Assumption Life carries the highest simplified-issue cap at $750,000 and typically prices below the others on simplified-issue term. Canada Protection Plan is the choice when a 25-year term length is needed or when permanent conversion is part of the plan. iA Access Life works for applicants with complex health profiles where lenient questions matter more than price. RBC YourTerm with Express Underwriting is the choice for healthy under-50 applicants who want brand-name fully-underwritten coverage without the medical wait. Sun Life through the broker channel is similar with a smaller age and amount window. A broker comparing all five against a specific profile finds the best fit faster than picking one in advance.

5.Can I switch from no medical to traditional life insurance later?

Yes, and it is a common broker workflow. Coverage often gets placed as no medical or simplified-issue first to address an immediate need (a mortgage closing, a collateral loan assignment, a recent decline elsewhere) and then revisited 6 to 24 months later when there is time to apply for fully-underwritten coverage at potentially lower rates. The original simplified-issue policy stays in force throughout the new application period. Once the new fully-underwritten policy is approved and issued, the simplified-issue policy can be cancelled.

Talk to a broker

{kind=link}