Segregated Funds in Canada: Advantages, Real Costs, and Who They Suit

By Parvesh Benning, Licensed Life Insurance and Investment Broker

A segregated fund is not an expensive mutual fund with an insurance badge on it. It’s a different product that does something mutual funds and GICs structurally cannot do.

Updated: April 24, 2026

Segregated Funds in Canada: Advantages, Real Costs, and Who They Suit

By Parvesh Benning, Licensed Life Insurance and Investment Broker

A segregated fund is not an expensive mutual fund with an insurance badge on it. It’s a different product that does something mutual funds and GICs structurally cannot do.

Updated: April 24, 2026

Segregated fund contracts sit in a quiet corner of the Canadian investment market. Most bank clients have never been offered one, because most bank advisors are not licensed to sell them. This guide covers what a segregated fund is, what the guarantees actually protect, what they cost, how they compare to mutual funds and GICs, and when one belongs in a plan, written from the broker desk, not a product brochure.

Quick answer

Should you put your money in a segregated fund?

A segregated fund is an insurance contract that holds investments and protects 75 to 100 percent of your principal at maturity or on death. It belongs in a plan when you want market growth with a downside floor, or when you want money to pass directly to a beneficiary outside your estate.

It is not the right tool for money you need within a year, and the higher fees only make sense if the contract earns its keep through the guarantees, the estate planning advantages, or the broker advice that comes with it.

Segregated funds in Canada: jump to section

- What are segregated funds

- How segregated funds work

- Advantages of segregated funds

- Disadvantages and costs of segregated funds

- Segregated funds vs mutual funds vs GICs

- How to choose the right seg fund contract

- Is a segregated fund the right tool for your situation

- How segregated funds are taxed in Canada

- Common questions about seg funds

What Are Segregated Funds

Most of the time when someone calls me about a segregated fund, the first thing I do is slow the conversation down. It’s not just the investment itself. It’s the overall plan. There are multiple paths to success to get to your ultimate goal, and it’s not that one is always better than the other. The disappointment comes from when we don’t see value.

So before we get to what a segregated fund is, here is what it does. A segregated fund is an insurance contract that holds investments. It protects 75 to 100 percent of the money you put in, either at maturity or on death, and it lets you name a beneficiary so the proceeds pass directly to that person and skip the estate. That is the short version. The longer version is what the rest of this guide is for.

The word “segregated” comes from the fact that the money sits in a pool that is legally separate from the insurance company’s own assets. It is not commingled with the insurer’s books. If the insurer ran into trouble, the contract is also backstopped by Assuris, the industry-funded protection plan that covers Canadian policyholders if a life insurance company becomes insolvent.

| Feature | What it means in plain language |

|---|---|

| Insurance contract | Issued by a life insurance company, not a mutual fund company or a bank |

| Principal protection | 75% or 100% of what you invested is guaranteed at maturity or on death |

| Named beneficiary | Money passes directly to the person you choose, outside your estate |

| Underlying investments | Stocks, bonds, balanced funds, sometimes index exposure depending on the contract |

| Where to buy one | Only through a licensed life insurance broker or advisor — not at a bank teller window |

Most bank clients have never been offered a segregated fund. The reason is simple. Bank advisors are typically licensed for mutual funds and GICs. They are not licensed to sell insurance contracts. So if your money is sitting at a bank, the segregated fund option is not in front of you. You have to go to an independent broker to get access. That alone is the gap most clients don’t know exists.

One more thing. The intake matters more than the product. The more I know about a client, what they own, what they owe, who depends on them, what they are trying to protect, the better the advice gets. A segregated fund is one tool. It is not the answer to every question. The right answer comes after the conversation, not before it.

How Segregated Funds Work: Guarantees, Resets, and Withdrawals

You put money into a segregated fund contract, and that money is allocated to one or more underlying funds you choose with your broker. The unit value moves with the market, same as a mutual fund. What is different is the contract sitting on top of the units. The contract is what gives you the guarantee.

The guarantee comes in three flavours, and the choice between them is one of the few real decisions a client makes when setting up the contract.

Tier 1

75 / 75

75% of what you invest is guaranteed at maturity. 75% is guaranteed on death. The cheapest option. Suits younger clients with a long time horizon and less concern about death-benefit protection.

Tier 2

75 / 100

75% guaranteed at maturity. Up to 100% guaranteed on death. The middle ground. Often the right choice when leaving money behind matters but the maturity floor is less critical.

Tier 3

100 / 100

100% maturity guarantee. 100% death benefit guarantee. The most expensive option. Most appropriate for older clients who want full principal protection at both endpoints.

The reset feature is where the contract earns its keep

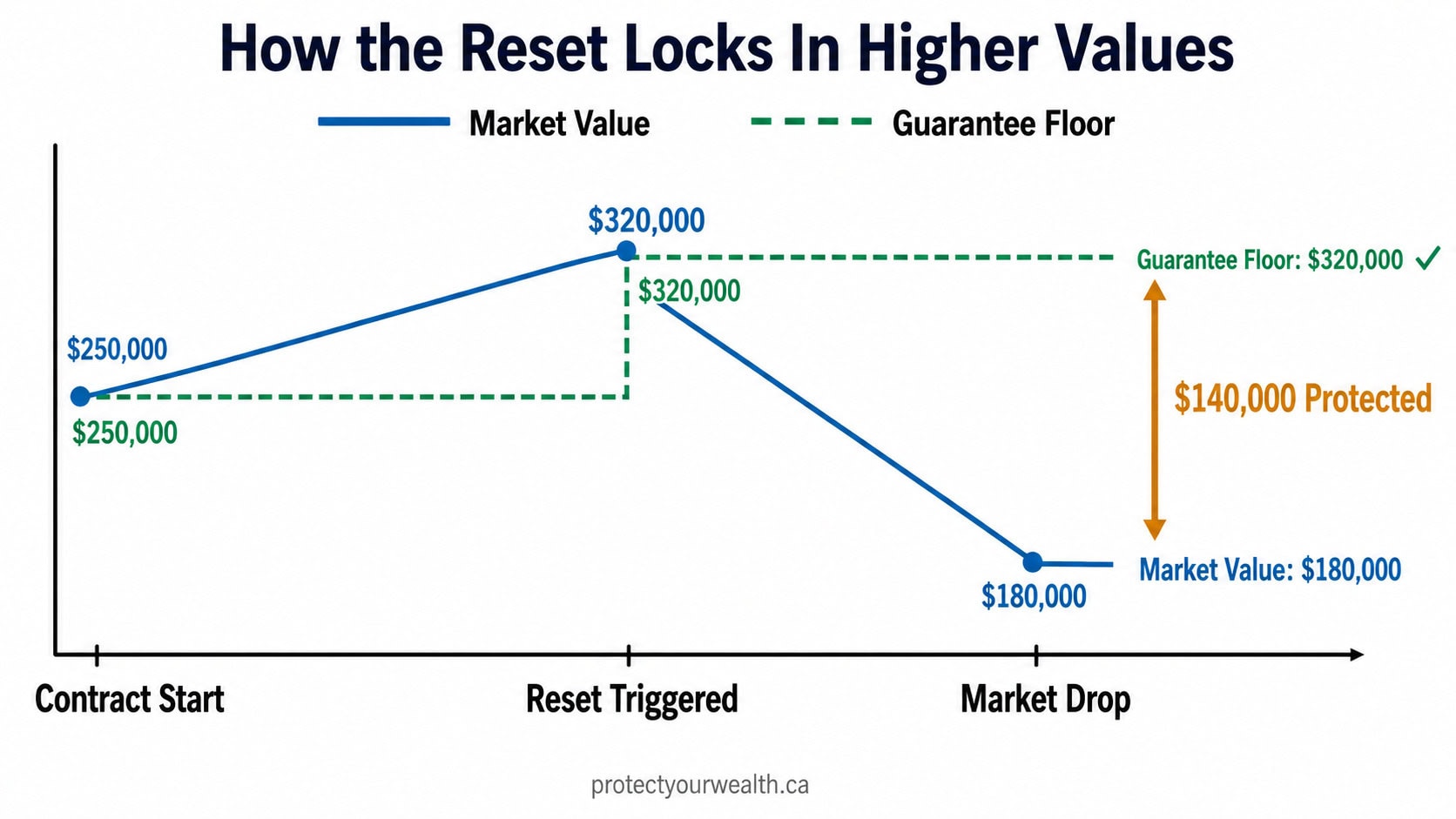

Most segregated fund contracts let you reset values and lock in higher values. Here is what that means in practice. You start with 100,000 dollars. The market goes up and your contract is now worth 130,000 dollars. You trigger a reset. From that point, the new guaranteed amount is 130,000 dollars, not the original 100,000 dollars.

The reset clock for the maturity guarantee restarts when you reset, which is the trade-off. But the floor moves up. For older clients worried about market values fluctuating, there is tremendous value in being able to say that no matter what, your balance is protected, and if it goes up as we expected, we can lock in the higher returns. That alone has great value to a client.

What the guarantee actually does on a $250,000 portfolio

Numbers make this concrete. A client invests $250,000 in a segregated fund contract. The market drops and the portfolio falls to $180,000. Here is what each guarantee tier delivers.

Invested

$250,000

Market value after drop

$180,000

| Guarantee tier | At maturity | On death |

|---|---|---|

| 75 / 75 | $187,500 (75% of $250K) | $187,500 (75% of $250K) |

| 75 / 100 | $187,500 (75% of $250K) | $250,000 (100% of $250K) |

| 100 / 100 | $250,000 (100% of $250K) | $250,000 (100% of $250K) |

Without the contract, the client or beneficiary receives $180,000. With a 75/100 contract, the beneficiary receives $250,000. That is a $70,000 difference created entirely by the insurance contract sitting on top of the investment.

Now add the reset. Say the portfolio went up to $320,000 before the market dropped. The client triggered a reset at $320,000. On a 75/100 contract, the death benefit guarantee is now based on $320,000, not the original $250,000. The beneficiary receives $320,000 even though the market value is sitting at $180,000. That is $140,000 of protection the contract created. No mutual fund does this. No GIC does this.

Withdrawals reduce the guarantee proportionally

You can take money out of a segregated fund contract at any time, at the current market value. The money is liquid. What changes when you withdraw is the guaranteed amount sitting underneath. Most clients don’t realize that any withdrawal reduces the guarantee on a proportional basis. If you withdraw 20% of the contract value, the guarantee drops by 20%. The mechanism is mechanical, not punitive, but it changes the math on early withdrawals.

The 10-year hold is the rule of thumb most carrier brochures lead with. That refers to the maturity guarantee. It is the date at which the principal protection kicks in if the market value happens to be lower than what you put in. The death benefit guarantee does not require a 10-year hold. It applies whenever the contract holder passes away.

Put simply: if the money is needed within a year, a segregated fund is the wrong tool, not because the money is locked up, but because the guarantees don’t have time to do their work. For a very short term, less than a year, a GIC or a high-interest savings account makes more sense, and that is something I direct clients toward when liquidity is the priority. For longer time horizons, the guarantees and the resets start working in your favour.

Advantages of Segregated Funds That Mutual Funds Can’t Match

The advantage that matters most is structural. A segregated fund pairs market growth with a downside floor and an estate-planning tool, all in one contract. Mutual funds give you market growth. They do not give you the floor and they do not give you the estate planning. Those two pieces are what segregated funds bring to the table that other investment products cannot.

Probably the strongest feature is the maturity and death benefit guarantees. You get the ability to invest while having full principal protection in the future. That is a powerful thing for a client to know. The contract value can move with the market, but the guaranteed floor is sitting underneath.

The death benefit guarantee, in plain language

If the contract holder passes away and the principal value is lower than the 100% guarantee, or the 100% guarantee with a reset, on passing that amount is credited. The beneficiary receives the higher of the market value or the guaranteed amount. There is no estate involvement. The proceeds go directly to the named person.

That last part matters more than most clients realize. Beneficiary designations on insurance contracts bypass probate, which means faster settlement, lower estate fees, and privacy. Probate records may become part of the public record depending on the province. Insurance beneficiary designations are not.

Creditor protection for self-employed and business owners

Where a beneficiary is properly designated and the contract is structured correctly, segregated fund proceeds may be protected from the claims of creditors in the event of bankruptcy or a lawsuit. The mechanics depend on provincial legislation and how the contract is set up, so the protection is conditional, not automatic. But for self-employed clients and business owners, that potential creditor protection is one of the reasons the contract gets considered in the first place.

An estate planning tool, not just an investment

A segregated fund contract can also offer an annuity settlement option. If a client is concerned about leaving a lump sum behind, they can leave instructions for the beneficiary to receive a monthly payment from the proceeds for a set amount of time, or for the beneficiary’s lifetime. That kind of control over how money is passed on is something a mutual fund holding cannot do.

None of these features matter in isolation. They matter when they line up with the client’s plan. A 35-year-old single tradesperson with no dependents has a different need than a 67-year-old retiree with three grandchildren and an unincorporated side business. The advantages above are real, but they only earn their keep when the contract is matched to the situation.

Disadvantages and Real Costs of Segregated Funds

The honest answer on disadvantages starts with this. Fees without value will always feel like a fee. That is the difference between a contract that earns its keep and one that doesn’t. The disadvantages below are real, but they are conditional on the contract being matched to the wrong situation, not on the product being wrong by default.

The most common criticism of segregated funds is that they are expensive. That criticism is built on a single comparison: the highest retail MER on a seg fund versus the lowest retail MER on a bank mutual fund or an ETF. It is not a fair comparison, because it ignores that the cost of a segregated fund changes materially based on how the contract is structured.

Many seg funds are actually a hybrid cost-wise between ETFs and mutual funds, in particular in larger investment accounts. The same fund inside the same contract can look very different on cost depending on whether it sits inside a fee-based account, a no-load structure, or a traditional commission-based arrangement.

What actually moves the cost

Three structural decisions determine where a contract lands on cost

Variable 1

Sales charge option

F-class options exist for clients with fee-based or wrap accounts and exclude the embedded sales commission entirely. No-load and Professional Service Fee options unbundle the advice fee from the fund. The same fund can carry materially different costs depending on which option is selected.

Variable 2

Account size

Larger account sizes can access fee structures that smaller accounts cannot. At higher balances, the effective cost of the contract approaches the cost of holding mutual funds with comparable advice attached.

Variable 3

Guarantee tier

A 75/75 contract carries a smaller insurance fee than a 75/100 contract. The maturity-only guarantee costs less than the full death benefit guarantee. The right tier depends on the client, and so does the cost.

Here is the part most articles skip. It’s not fees that matter as much as the value you get for paying them. Are you happy with the advice you are getting? Is there added value? If a client saves thousands in taxes due to optimizing how they manage their investment accounts, if they are introduced to solutions they would not have otherwise known, if their net rate of return is higher than an investment with a lower MER but a lower net return, those are examples of why value exceeds fees every time.

That logic is the entire test for whether the fee is worth paying. Net return after fees, plus the dollar value of advice that touches the rest of the financial plan, has to beat the alternative the client would otherwise choose. If it doesn’t, the contract is wrong for that client.

The other disadvantages, called honestly

The maturity guarantee is the most misunderstood feature, and it gets miscast as a liquidity restriction. It is not. The money inside a segregated fund contract is fully liquid. A withdrawal at any time returns the current market value of the contract. What the maturity guarantee does is set a date, typically 10 years out, when the principal floor kicks in if the market value happens to be lower than what was deposited. Withdraw before that date and you take the market value as it stands. The money is available the entire time. The guaranteed floor is what has the timeline, not the access.

The fund universe is narrower than the mutual fund market. Carriers offer dozens of funds inside their seg fund contracts, but it is not the thousands available across the broader mutual fund industry. For most clients building a diversified portfolio that is not a constraint. For specific niche allocations it can be.

The contract is more complex than a mutual fund unit. Maturity dates, reset windows, beneficiary structures, guarantee tiers, sales charge options. These are real decisions, not boilerplate. The complexity is why broker guidance matters, and it is also why the contract should not be sold as a default to clients who haven’t sat down and walked through the plan first. Fees without value will always feel like a fee. That’s the difference.

Segregated Funds vs Mutual Funds vs GICs: When Each Makes Sense

The advantage of a seg fund is that you have advantages such as 100% principal guarantee at both maturity and on death, and that allows you to be much more flexible in terms of investment options, which have much more upside, because your principal is protected. That single sentence reframes the whole comparison. Most people think segregated funds are expensive mutual funds with an insurance badge on them. They aren’t. The protection is what enables the flexibility, not the other way around.

Mutual funds give you market exposure with no floor. GICs give you a floor with almost no growth. A segregated fund sits between the two and gives you both, with the trade-off being a slightly higher cost for the contract that holds it together. Choose the one that matches the job, not the one with the lowest sticker price.

| Feature | Segregated fund | Mutual fund | GIC |

|---|---|---|---|

| Principal protection | 75% to 100% at maturity or on death | None | 100% of principal |

| Upside potential | Full market exposure | Full market exposure | Fixed interest rate, often below inflation |

| Liquidity | Withdraw any time at market value, withdrawals reduce the guarantee proportionally | Withdraw any time at market value | Locked until maturity (typical) |

| Beneficiary designation | Yes, bypasses the estate | Generally no, flows through the estate | Generally no, flows through the estate |

| Reset feature | Yes, can lock in higher values | No | No |

| Cost structure | Varies by series, fee class, and account size; F-class and fee-based options available | MER varies by fund family and class | No MER, but interest rate is the cost relative to growth |

| Where you buy it | Licensed life insurance broker or advisor | Bank, mutual fund dealer, online broker | Bank, credit union, life insurance company |

When a GIC is genuinely the better choice

For a very short term, less than a year, a GIC or a high-interest savings account can make sense, and that is something I direct clients toward when liquidity is the priority. If money is needed in a short amount of time, parking it in something liquid is the right call. The seg fund’s guarantees and growth advantages don’t have time to do their work over a few months.

The longer the time horizon, the worse the GIC looks. Posted GIC rates have been below inflation for most of the past two decades. The principal is intact in nominal terms but losing real purchasing power year after year. That is the quiet cost of choosing the safest-looking option without thinking about the time horizon.

When a mutual fund is the right tool

Mutual funds work for clients who want lower fees, are comfortable with full market risk, and don’t need the estate planning features of an insurance contract. A long-horizon investor who has separate insurance coverage in place, who is contributing inside a TFSA or RRSP, and who values fund choice over guarantees has a strong case for mutual funds or low-cost ETFs.

The reason mutual funds dominate is partly historical. They were marketed to Canadian banks first and got entrenched in retail distribution. Most Canadians at a bank have been steered into mutual funds because that is what the licensed staff at the bank can sell. It is not that the seg fund was rejected for that client. It was never on the menu.

When a segregated fund earns its keep

This is where the family example comes in. A few years ago my father passed away. His seg fund portfolio was below the initial investment amount. It passed to my mother at the reset value. That is the kind of moment that proves what the contract is for. The market did what the market does. The contract did what the contract is supposed to do.

Segregated funds make sense when one or more of the following is true: the client is closer to retirement and wants principal protection without giving up market growth, the client wants beneficiary designation to bypass probate, the client is self-employed or running a business and creditor protection matters, or the client has a legacy intent and wants the death benefit guarantee to underwrite what gets passed on. The contract is rarely the right answer for someone in their 30s with no dependents and a long runway. It is often the right answer for someone in their 60s, 70s, or 80s who has built something and wants it to land safely.

Net answer: GIC for short-term liquidity, mutual fund or ETF for low-cost long-term growth, segregated fund when growth and protection both matter and the contract earns its keep through the guarantees and the estate planning. The choice isn’t ranked. It is matched to the job.

Before you decide

A segregated fund is one tool. The right tool depends on the plan it sits inside.

Most clients calling about seg funds end up in a different conversation than the one they expected. Account structure, beneficiary setup, tax efficiency across registered and non-registered, and creditor protection all sit on the same table. The contract is the last decision, not the first.

How to Choose the Right Seg Fund Contract

Not all segregated funds are created equal. Different cost structures, different fund access, different features inside the contract. The work of choosing one is matching the contract to the plan, not picking the carrier with the best brochure.

For carriers, sometimes the choice is based on actual products they offer and the features inside them. As one example, Desjardins offers a contract that includes a 100% death benefit guarantee plus an inflation adjustment, meaning worst case your money will be passed on and will at least keep up with inflation over the life of the contract. That feature is a real differentiator, and it is the kind of detail that doesn’t show up until someone has actually compared contracts side by side.

Three things that vary across contracts, and why they matter

Cost structure

Fee class and series both move the MER

Many seg funds are actually a hybrid cost-wise between ETFs and mutual funds, in particular in larger investment accounts. F-class with a fee-based advisor agreement looks very different from A-class with embedded commissions. The published MER is not the whole story.

Fund access

The fund universe is different at every carrier

Some contracts give access to 70-plus funds. Others give access to 10 or 30. The mix of equity, balanced, fixed income, and index exposure varies by carrier. Matching the fund universe to the client’s investment plan matters more than chasing the contract with the most options.

Specific features

Resets, inflation adjustments, lifetime income

Reset frequency, age ceilings on resets, inflation adjustments on the death benefit, and lifetime guaranteed income riders all vary contract by contract. These features can be the entire reason one contract suits a client and another doesn’t.

The intake is the actual work

Choosing a contract is the last step, not the first. Before any product gets named, the intake matters: what the client owns, what they owe, who depends on them, what their tax situation looks like, what they want their money to do over the next 20 or 30 years. The contract is selected to fit the answer to those questions, which is why a comprehensive client intake form, not a product brochure, is where the conversation should start.

Skip that step and the fee will feel like a fee. Do that step properly and the contract earns its keep, because it is solving a real problem the client actually has.

Is a Segregated Fund the Right Tool for Your Situation?

How well does a segregated fund contract fit your situation? Answer 5 questions for a personalized read.

Estimated time: 60 to 90 seconds

How Segregated Funds Are Taxed in Canada

Segregated funds are taxed similarly to mutual funds in most cases, with a few specific differences that matter at the edges. Interest, dividends, and capital gains earned inside the contract flow through to the contract holder and appear on a T3 slip the same way they would in a mutual fund. The character of the income is preserved, so dividend tax credits and capital gains inclusion rates apply the same way they would on a mutual fund holding.

The tax outcome depends on the account the contract sits inside, not just the contract itself. Inside a registered account such as an RRSP, RRIF, or TFSA, the seg fund follows the same rules as anything else held in that account. No tax on growth inside the wrapper. RRSP and RRIF withdrawals are fully taxable as income. TFSA withdrawals are not taxable. The contract being a segregated fund changes nothing about that.

| Account type | Tax treatment of segregated fund income |

|---|---|

| Non-registered | Annual T3 reports interest, dividends, capital gains. Capital losses also flow through. |

| RRSP / RRIF | No tax on growth inside the account. Withdrawals fully taxed as income. |

| TFSA | No tax on growth, no tax on withdrawals. |

| FHSA | Contributions deductible, qualifying withdrawals tax-free. |

| Death benefit | Paid to a named beneficiary, generally not taxable as income. |

The capital loss flow-through advantage

Here is the one tax difference most articles skip. A mutual fund cannot flow through capital losses to the unit holder. The losses are absorbed inside the fund and used to offset future fund-level gains, but they don’t show up on your T3. A segregated fund can. Capital losses generated inside the contract get reported to the contract holder and can be used to offset capital gains elsewhere on the tax return.

For a non-registered account in a year where the contract realizes losses, that flow-through can be the difference between a tax bill and a usable loss. It is a small structural advantage that compounds over time in a non-registered taxable account.

Switches and series transfers can trigger tax

One detail to flag for non-registered contracts. Moving between segregated fund series inside the same contract — for example, switching from an investment series into an estate series — can be treated as a disposition for tax purposes. The mechanics depend on the carrier and the specific contract structure. Inside a registered account this isn’t an issue. Inside a non-registered account it should be planned, not done on a whim.

The death benefit on a segregated fund passes to a named beneficiary outside the estate. The proceeds are generally not subject to income tax in the beneficiary’s hands. That is the same treatment as a life insurance death benefit, which is the entire reason the contract sits inside an insurance contract in the first place.

Tax rules change. The treatment described here reflects current Canadian tax rules for segregated fund contracts as of the most recent tax year. Specific situations should be confirmed with a tax advisor or accountant who knows the full picture of the client’s return.

Common Questions About Seg Funds

Most of these come up in the first conversation with a client. The answers depend on the specific contract and the client’s situation, so treat what follows as general guidance, not a substitute for sitting down and walking through the plan.

Question 01

Are segregated funds worth it?

Segregated funds are worth it when the guarantees, the beneficiary designation, the potential creditor protection, or the broker advice attached to the contract solve a real problem the client has. They are not worth it when the contract is sold without a comprehensive information gathering, the client doesn’t need any of the structural features, and a lower-cost mutual fund or ETF would do the same job. The honest test is whether the net rate of return after fees, plus the dollar value of the planning advice, beats the alternative the client would otherwise choose.

Question 02

How long do I have to hold a segregated fund?

The maturity guarantee typically requires a 10-year hold. That is the date at which the principal protection kicks in if the market value of the contract is lower than what was invested. The death benefit guarantee does not require a hold period. It applies whenever the contract holder passes away. Money can be withdrawn at any time at the current market value, but the maturity guarantee assumes the contract is held to that date for the principal floor to apply.

Question 03

Can I withdraw money from a segregated fund before maturity?

Yes. Withdrawals are allowed at any time at the current market value of the contract. The money is liquid. The trade-off is that the guaranteed amount reduces proportionally to the size of the withdrawal. If 20% of the contract value is withdrawn, the guarantee drops by 20%. The mechanism is mechanical, not punitive, but it changes the math on early withdrawals and is one of the reasons the broker conversation about timing matters before the contract is set up.

Question 04

Do segregated funds protect me from creditors?

Where a beneficiary is properly designated and the contract is structured correctly, segregated fund proceeds may be protected from the claims of creditors in cases of bankruptcy or lawsuit. The protection is not automatic. It depends on provincial legislation and how the contract is set up. The protection is one of the reasons self-employed clients and business owners often consider segregated funds in the first place, but the structure has to be right for it to hold up.

Question 05

Are segregated funds the same as guaranteed investment funds (GIFs)?

Yes. GIF and segregated fund are interchangeable terms in Canada. Some carriers brand their products as Guaranteed Investment Funds, others as segregated fund contracts, but the underlying structure is the same: an insurance contract holding investment options with maturity and death benefit guarantees. If the question is whether a specific contract suits a specific client, that answer depends on the intake. Talk to a broker directly before making the decision.

{kind=link}