Halal Life Insurance in Canada: What’s Actually Available

By Parvesh Benning, Licensed Life Insurance Broker

In twenty-plus years of placing coverage for Muslim families across Canada, the question is always the same, and the answer is more practical than most websites make it sound.

Updated: April 21, 2026

Halal Life Insurance in Canada: What’s Actually Available

By Parvesh Benning, Licensed Life Insurance Broker

In twenty-plus years of placing coverage for Muslim families across Canada, the question is always the same, and the answer is more practical than most websites make it sound.

Updated: April 21, 2026

There is no certified halal life insurance policy in Canada. No takaful product exists for individual buyers here. But that does not mean Muslim families are left without options. A non-participating term life policy, with no cash value and no interest component, is what most Islamic scholars who permit coverage point to as the practical path. I have placed this type of coverage for hundreds of Muslim families, and the process is no different from any other family looking to protect against premature loss.

This guide covers the scholarly positions on life insurance in Islam, explains what actually exists in Canada today, and walks through how to choose and apply for faith-aligned term coverage. If you already know what you need, start with a quote here.

Is life insurance halal in Canada?

Yes, if structured as term. A non-participating term life policy with no cash value, no dividends, and no interest-bearing component meets the criteria most permissive scholars set for faith-aligned coverage.

What qualifies: Level-premium term life from any major Canadian insurer. No savings portion. No investment subaccounts.

What to avoid: Whole life, universal life, and any participating policy. These accumulate cash value tied to interest or market returns.

The real question is not whether coverage exists. It does. The question is which carrier and term length fits your specific health profile, budget, and family needs.

See what Islamic scholars say about term life or how families are matched to carriers.

What this guide covers

- Can You Get Halal Life Insurance in Canada?

- What Islamic Scholars Actually Say About Life Insurance

- What Is Shariah-Compliant Life Insurance

- Takaful vs Traditional Life Insurance in Canada

- What Halal-Aligned Coverage Exists in Canada Today

- How to Choose a Term Policy That Aligns with Islamic Principles

- How Muslim Families Are Matched to the Right Carrier

- Foreign Travel, Hajj, and New-to-Canada Coverage

- Charitable Giving and the Foresters Charity Benefit

- Frequently Asked Questions

Can You Get Halal Life Insurance in Canada?

Protection needs are allowed in Islam, as long as there is no cash value or interest accumulated in the policy. I have worked with hundreds of Muslim families over my twenty-plus years as a broker, and the coverage they carry is straightforward non-participating term life insurance. No certified takaful product exists for individual buyers in Canada today, but that does not mean families are stuck.

The first hurdle is always the same question: is this permissible? Based on everything I have seen, and the scholarly positions laid out in the next section, the answer for term life is yes. Once we get past that, we steer right to finding the optimal solution, the same way I would with any family. We deal with almost 20 companies, and the goal is always the best coverage at the best price for that specific household.

Think of it like car insurance or home insurance. You pay premiums for protection. If something happens, you are covered. If nothing happens, you paid for that protection period. No money comes back, no interest builds up, no investment sits inside the contract. Term life works the same way. Coverage for a defined period, 10, 20, or 30 years, and if nothing occurs during that term, it simply ends.

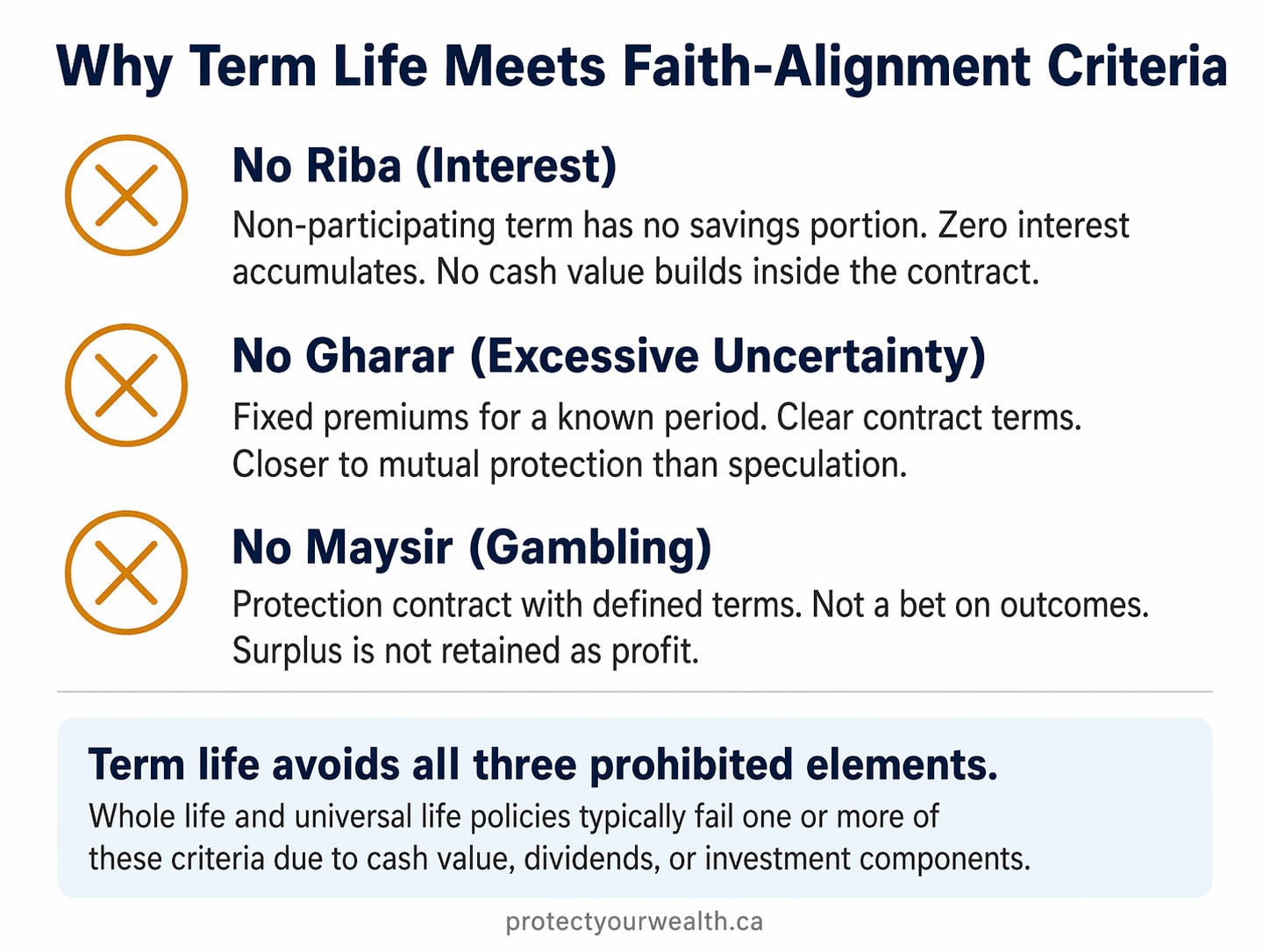

This is why scholars who permit life insurance point specifically to term. Three things matter in the analysis. First, no riba: a non-participating term contract generates zero interest because there is no savings portion. Second, the contract structure is clear and defined, known premiums for a known period, which addresses concerns about gambling or excessive uncertainty. Third, providing for your family after death aligns with the Quranic emphasis on caring for dependants.

The detailed scholarly positions, including who permits, who permits under conditions, and who prohibits, are in the section below.

What Islamic Scholars Actually Say About Life Insurance

I am not a scholar and I do not profess to be one. What I know is based on deep research and years of experience helping Muslim families who have all reached the same conclusion: term life insurance with no cash value is permissible. Not certified halal. But it meets the definition that would allow it to be permissible under Islamic principles. Below is what the scholars themselves have published.

Scholars and institutions that permit term life insurance

Ibrahim Khan, co-founder of Islamic Finance Guru, holds a BA from the University of Oxford, an Alimiyyah degree from Al Salam Institute, and an MA in Islamic Finance. He is the author of Halal Investing for Beginners (Wiley). His position: term life insurance is permissible because it is pure protection with no investment component. Whole life insurance is only permissible if the underlying investments are themselves Shariah-compliant. He treats this as a straightforward distinction. Protection contract versus investment vehicle. His full analysis is published on his Islamic Finance Guru site.

Dr. Monzer Kahf, former senior economist at the Islamic Research and Training Institute (Islamic Development Bank), has written that the decisive question is not the label “insurance” but whether the contract itself contains interest. He names term life specifically as the type that does not. His fatwa collection states plainly that he does not see anything impermissible in buying life insurance contracts that do not contain interest. He follows the reasoning of Shaikh Mustafa al-Zarqa, one of the most influential Islamic jurists of the 20th century, who argued that insurance fulfills a general public need and that its social benefit overrides the theoretical concerns about uncertainty.

Egypt’s Dar al-Ifta, established in 1895 and one of the oldest governmental fatwa institutions in the Muslim world, has issued the broadest institutional permission. Their published fatwa states that life insurance is lawful, that it is a contract of contribution rather than speculation, and that it aligns with the Quranic principle of mutual cooperation found in Surah Al-Ma’idah (5:2). Their ruling is available in their official fatwa database.

Shaykh Joe Bradford, an American Islamic finance scholar and founder of the estate planning platform MyWassiyah, has publicly stated that term life insurance is permissible under conditions: no cash value, no fixed returns on premiums, protection only.

Institutions that permit under necessity

The Assembly of Muslim Jurists of America (AMJA) maintains that commercial life insurance is prohibited by default, but recognizes exceptions for genuine necessity or employer-provided coverage. Their 2019 conference recommendations state that life insurance is forbidden in all of its forms, then narrow the exception to cases where a genuine need comparable to necessity exists. For a Canadian family with dependants and no realistic takaful alternative, this exception is directly relevant.

What this means practically

There is no consensus. Institutions like the International Islamic Fiqh Academy in Jeddah and platforms like IslamQA.info maintain that all commercial life insurance is prohibited. That position exists and families should be aware of it. But the scholars who permit term life specifically point to three factors: no interest because there is no savings portion, a clear contract structure with known premiums for a known period, and the absence of any realistic takaful alternative in Canada. The families I work with read the positions, consult their own scholars or imams, and make a decision they are comfortable with. My job starts after that decision. Once a family decides to proceed, I find them the best term life coverage available across the carriers I work with.

What Is Shariah-Compliant Life Insurance

Shariah-compliant life insurance is a policy structured to avoid three things Islam prohibits in financial contracts: interest (riba), excessive uncertainty (gharar), and gambling (maysir). The concept originates from takaful, an Arabic term meaning mutual guarantee. In a takaful arrangement, participants contribute to a shared pool that pays claims when a member needs support. The pool is managed under ethical guidelines that exclude interest-bearing investments and industries that conflict with Islamic values.

True takaful operates differently from conventional insurance. Conventional insurers assume risk for profit and invest premiums however they choose, often in interest-bearing instruments. Takaful spreads risk across participants, and any surplus is typically redistributed rather than kept as profit. The distinction matters because the structure of the contract, not just the outcome, determines whether it aligns with Islamic principles.

In Canada, no retail takaful product exists for individual life insurance buyers. That is the gap this entire page addresses. The practical alternative is a non-participating term life policy: no cash value, no dividends, no investment component. It is not takaful. But it avoids the specific elements (riba, gharar, maysir) that make other policy types problematic. Whole life and universal life policies typically accumulate cash value tied to interest or market returns, which is why scholars who permit term life generally do not extend that permission to permanent products.

Takaful vs Traditional Life Insurance in Canada

Takaful and conventional insurance solve the same problem, protecting against financial loss, but the money moves differently. In takaful, participants contribute to a shared pool managed under ethical guidelines. Claims are paid from the pool, and any surplus goes back to the participants. Nobody profits from someone else’s loss. In conventional insurance, the insurer collects premiums, assumes the risk, and invests that money however it chooses, often in interest-bearing instruments. Profit goes to shareholders.

That structural difference is why Islamic scholars treat them differently. Takaful avoids interest because the pool is invested ethically. It reduces uncertainty because participants share the risk collectively rather than transferring it to a profit-driven company. And it eliminates the gambling concern because surplus is returned, not retained as profit.

The problem is that no individual takaful life insurance product exists in Canada. So families looking for faith-aligned coverage work with what is available. A non-participating term life policy is the closest conventional product to takaful principles: no cash value sitting in interest-bearing accounts, no dividends, no profit-sharing component, and a clear fixed-term contract. It is not takaful. But it avoids the specific elements that make conventional permanent policies problematic.

Whole life and universal life policies sit on the other side. They accumulate cash value, generate interest or market-linked returns, and often include dividend participation. For families trying to align coverage with Islamic principles, these are the product types to avoid. If you are ready to evaluate specific term policies, these ten factors cover what to look for beyond price.

What Halal-Aligned Coverage Exists in Canada Today

Every major Canadian insurer offers a non-participating term life policy. Manulife, Canada Life, RBC, iA Financial, Empire Life, Beneva, Foresters, Desjardins. All of them. The product that qualifies as faith-aligned is not special or hard to find. It is the most common type of individual life insurance sold in this country: level premiums, fixed term, no cash value, no dividends, no investment component.

That means the question is not whether coverage exists. It does. The question is which carrier offers the best price for your specific health profile, age, coverage amount, and term length. I work with almost 20 companies, and rates vary significantly between them for the same person. A 35-year-old non-smoker requesting $500,000 over 20 years might see a 30% price difference between the most and least expensive carrier. The product structure is the same across all of them. The price is not.

If your health is straightforward, fully underwritten term gives the best pricing. If you have a time-sensitive need or a minor health concern, simplified issue term is a backup option that still avoids the cash value and investment elements. For a deeper look at no-medical options, that page covers the trade-offs in detail.

What qualifies as faith-aligned

Non-participating term life from any major Canadian insurer. No cash value. No dividends. No investment subaccounts. Level premiums for a fixed period. Every carrier listed above offers at least one product that meets these criteria.

What to avoid

Whole life, universal life, and any participating policy. These accumulate cash value, generate interest or dividends, and include the investment elements that create the riba concern. If a product has a savings component, it does not meet the criteria most permissive scholars set for term life.

One thing worth knowing: any term life policy from any Canadian insurer allows you to designate a charity as a beneficiary. You can allocate any percentage you choose. This is not unique to any one carrier. If charitable giving is part of your plan, it is built into the beneficiary structure across the board. Comparing across carriers is how you find the right combination of price, term length, and features for your family.

How to Choose a Term Policy That Aligns with Islamic Principles

Once the permissibility question is settled, the process of choosing a policy is the same as it is for any family. We discuss everything we would discuss normally: health, income, dependants, debts, and timeline. The faith-alignment part comes down to four things you confirm before signing.

1 Non-participating structure

No cash value accumulates, no dividends are paid, no investment subaccounts exist inside the contract. Level premiums for the full term. This is the single most important filter.

2 Term length matched to need

Ten years if you are bridging a short-term debt. Twenty years for a mortgage and young children. Thirty years for maximum simplicity across education, housing, and dependant care. Do not default to the longest term if a shorter one genuinely fits. Longer terms cost more, and over-insuring on duration is the same waste as over-insuring on amount.

3 Coverage amount based on real numbers

Start with income replacement, typically 10 to 15 times annual earnings, then add outstanding debts and education goals. Subtract existing group coverage and assets you have already built. The goal is a number that keeps your family’s life intact, not a round number that feels right.

4 Fully underwritten when possible

If your health is stable and you can complete the process (application, tele-interview, and any required medical evidence), fully underwritten term gives the best price. Simplified issue term exists as a backup for time-sensitive situations or minor health concerns, but it costs more for the same coverage amount.

One misconception I see regularly: families assume that if nothing happens during the term, all the premiums come back. That is not how term life works. It is no different from car insurance or home insurance. You pay for protection during that period. If something happens, your family is covered. If nothing happens, the term ends. Products that do return premiums are a different category entirely and typically involve the investment components that create the riba concern in the first place.

When you are ready to see actual numbers, request a few term quotes here and confirm each option meets the four criteria above before comparing price.

How Muslim Families Are Matched to the Right Carrier

I do not work for any company. I work for my clients.

Muslim families shopping for faith-aligned coverage are often steered toward a single carrier by websites that have a financial relationship with that company. I have no such relationship. I work with almost 20 carriers and my only job is to find the best coverage at the best price for the family sitting in front of me.

When a Muslim family calls, the first conversation is about permissibility. Once a family is comfortable that non-participating term life meets their criteria, the process is identical to what happens for every other family. This is not theory. I have placed this coverage for hundreds of Muslim families over twenty-plus years. Same carriers, same underwriting, same routing logic.

Here is what that routing actually looks like in practice.

Healthy, non-smoker, build within carrier tables

The comparison runs across four or five carriers to find the lowest premium for that specific age, amount, and term length. Manulife, Canada Life, iA Financial, RBC, Empire Life, Beneva. The product structure is the same at all of them. The price is not. On a $500,000 term 20, the difference can be $15 to $20 per month between carriers for the same person. Over 20 years that adds up to thousands of dollars.

Health complications change the routing

If a client has type 2 diabetes, Foresters Financial is known in the industry to be extremely strong in this space. I would look there first. But if the concern is something else, say a cardiac history or elevated BMI, Foresters might not be the best fit, and I would route to a carrier whose underwriting is more flexible for that specific condition. That is the entire point of working with a broker who knows the differences.

New to Canada or non-permanent resident

A work permit holder at Industrial Alliance can get full coverage without any restrictions on residency status. RBC Insurance does not allow this. If I only worked with one carrier, or if I did not know which carriers accept which immigration status, that family either gets declined or pays more than they need to. It really is about knowing which path to navigate.

Foresters comes up often because other websites position them as the halal option. They are a strong company, founded in 1874, and they operate as a fraternal benefit society focused on community benefits rather than shareholder profit. From a faith standpoint, that structure aligns well. But Foresters is not necessarily the most cost-effective solution, and they are somewhat limited in the length of terms they offer. If a family needs a 30-year term and wants the lowest price, Foresters may not be where we end up. No issue recommending them when they are the right fit. But the goal as an independent broker is always to present all available options. Your peace of mind comes first. Always.

Hundreds of Muslim families

have started their coverage search with this exact conversation. Yours takes one call.

Compare across almost 20 carriers. No cost. No obligation.

Foreign Travel, Hajj, and New-to-Canada Coverage

Most Muslim families are no different from any other family in Canada when it comes to the application process. The need is the same: protect against premature passing. The underwriting is the same. Where things occasionally shift is travel.

Canadian carriers evaluate three things about foreign travel: where you are going, how long you will be there, and why. A two-week family visit abroad during a period with no travel advisories has zero impact on most applications. Extended stays in regions with active Canadian travel advisories, particularly level four “do not travel” warnings, are different. In those cases, an insurer may only offer coverage after the client returns to Canada. I handle this no differently than I would for any client travelling to a higher-risk destination. It is a timing and routing question, not a faith-specific issue.

Hajj and extended travel timing

If you are planning hajj or an extended family visit abroad, apply and complete your medical evidence before you leave. Paramedicals, labs, and the tele-interview can all be done in Canada ahead of departure. Once you are out of the country, most carriers will pause or postpone the file until you return. Getting the evidence done first keeps the application moving while you travel. If travel is already booked and departure is soon, simplified term options exist where travel itself would not have any impact on the application.

Residency status comes up regularly. I covered the specifics in the section above: some carriers accept work permit holders with no restrictions, others do not. If you are new to Canada with limited medical records here, provide whatever documentation you have, including provincial health coverage proof, immigration documents, and any overseas medical records. The more complete the file, the more carriers I can access for you.

Foreign Travel, Hajj, and New-to-Canada Coverage

Most Muslim families are no different from any other family in Canada when it comes to the application process. The need is the same: protect against premature passing. The underwriting is the same. Where things occasionally shift is travel.

Canadian carriers evaluate three things about foreign travel: where you are going, how long you will be there, and why. A two-week family visit abroad during a period with no travel advisories has zero impact on most applications. Extended stays in regions with active Canadian travel advisories, particularly level four “do not travel” warnings, are different. In those cases, an insurer may only offer coverage after the client returns to Canada. I handle this no differently than I would for any client travelling to a higher-risk destination. It is a timing and routing question, not a faith-specific issue.

Hajj and extended travel timing

If you are planning hajj or an extended family visit abroad, apply and complete your medical evidence before you leave. Paramedicals, labs, and the tele-interview can all be done in Canada ahead of departure. Once you are out of the country, most carriers will pause or postpone the file until you return. Getting the evidence done first keeps the application moving while you travel. If travel is already booked and departure is soon, simplified term options exist where travel itself would not have any impact on the application.

Residency status comes up regularly. I covered the specifics in the section above: some carriers accept work permit holders with no restrictions, others do not. If you are new to Canada with limited medical records here, provide whatever documentation you have, including provincial health coverage proof, immigration documents, and any overseas medical records. The more complete the file, the more carriers I can access for you.

Charitable Giving and the Foresters Charity Benefit

Any term life policy from any Canadian insurer lets you name a registered charity as a beneficiary. You choose the percentage. You choose the charity. This is not a special feature and it is not limited to any one company. If giving back is part of your plan, the mechanism already exists inside the standard beneficiary structure of every policy.

Where Foresters Financial adds something different is their Charity Benefit. On select term products, Foresters pays 1% of the basic death benefit (up to a stated cap) to a registered charity of your choice. That donation comes from the insurer, not from your family’s payout. Your beneficiaries still receive the full death benefit. You pick the charity, and you can change it later with a simple request.

It is a genuine value-add for families who want charitable impact built into the contract without any extra cost or complexity. But it is one factor among several. Foresters is a fraternal benefit society, founded in 1874, focused on community benefits rather than shareholder profit. From a faith standpoint, that structure aligns well. But as I covered above, Foresters is not always the most cost-effective option or the best fit for every health profile and term length. The charity benefit should not be the reason you overpay for coverage when you could designate a charity on a less expensive policy from another carrier and achieve the same outcome.

If you want to explore how other faith communities approach life insurance and charitable giving, this guide on Christian approaches to life insurance covers similar principles from a different perspective.

Frequently Asked Questions

Q1

Is takaful life insurance available in Canada?

No individual retail takaful life insurance product is available in Canada at this time. Takaful is a cooperative model where participants share risk through a common pool managed under ethical guidelines. While takaful products exist in parts of the Middle East, Southeast Asia, and the UK, Canadian regulators and insurers have not developed an equivalent. The practical alternative for Muslim families in Canada is a non-participating term life policy that avoids the specific elements (interest, cash value, investment returns) that make conventional permanent policies problematic.

Q2

Is term life insurance halal or haram?

There is no single answer. Scholars and institutions are divided. Those who permit it, including Ibrahim Khan of Islamic Finance Guru, Dr. Monzer Kahf, and Egypt’s Dar al-Ifta, point to three factors: term life generates no interest, the contract is clearly defined with known premiums for a known period, and no realistic takaful alternative exists in Canada. Institutions like the International Islamic Fiqh Academy in Jeddah maintain that all commercial insurance is prohibited. Most families I work with consult their own scholars or imams, review the positions, and make a decision they are comfortable with before proceeding.

Q3

Is disability insurance halal?

The same reasoning applies. A disability policy that pays a monthly benefit if you cannot work, with no savings component or investment return, follows a similar protection-only structure to term life. Many scholars who permit term life extend that permission to disability and critical illness coverage under the same logic: the contract is for protection, not profit or speculation. As with life insurance, consult your own scholar or imam if you are uncertain.

Q4

Does the Foresters charity benefit reduce what my family receives?

No. On eligible Foresters term products, the insurer pays the charitable donation separately. Your beneficiaries still receive the full basic death benefit. The 1% donation (up to a stated cap) comes from Foresters, not from your family’s payout. You select the charity and can update the designation later.

Q5

What if I have health issues or take medication?

The underwriting process is the same as it is for any Canadian applying for term life. Your health history, medications, build, and lifestyle factors determine which carriers offer the best outcome. Some conditions route better to specific carriers. That is exactly why working with a broker who knows the differences across multiple insurers matters. If fully underwritten term is not an option, simplified issue products exist that still avoid the cash value and investment elements.

Q6

Should I consult my imam or scholar before applying?

Yes, if you are uncertain. A scholar who understands Islamic jurisprudence and is familiar with how Canadian insurance contracts work can help you confirm that a non-participating term policy aligns with your values. Many families I work with have already had that conversation before they call me. Others read the scholarly positions, make their own decision, and proceed. Either approach is fine. My job as a broker begins once you decide to move forward.

{kind=link}