The Tax-Free Savings Account (TFSA) is an essential account that every Canadian need, regardless of their age, income, or financial goals. There are many reasons that prove that a TFSA is not just another savings account, but is rather one of the best kinds of savings account out there since it was introduced to Canadian banks in 2009! The TFSA can be an amazing investment vehicle, deposits and withdrawals anytime you want and all management fees (if you’re investing) are tax-free as well. The TFSA is a low-maintenance account that you can customize for saving or for growing. This blog will cover the benefits of the TFSA, giving you the top 7 reasons why every Canadian should have a Tax-Free Savings Account (TFSA).

In this article:

- What is a Tax-Free Savings Account (TFSA)

- How to open a Tax-Free Savings Account (TFSA)

- Benefits of a Tax-Free Savings Account (TFSA)

- Reason 1: Tax-Free savings to maximize growth

- Reason 2: Your contribution room grows every year

- Reason 3: Access your money anytime

- Reason 4: Use your Tax-Free Savings Account (TFSA) as an investment vehicle

- Reason 5: A savings account to complement your existing savings accounts

- Reason 6: Recontribution room

- Reason 7: Designate a beneficiary

- Frequently Asked Questions (FAQs) about Tax-Free Savings Accounts (TFSA)

What is a Tax-Free Savings Account (TFSA)

The Tax-Free Savings Account (TFSA) program was launched by the Canadian government in 2009 as a brand-new type of savings account to assist Canadian save up money completely tax-free. Anyone who has a Social Insurance Number (SIN) and is interested in saving money for various life stages are greatly benefitted by this kind of savings account.

The growth of the various investment options held in the TFSA, such as cash, stocks, bonds, GICs, and mutual funds, is not tax deductible. This means that any management fees, dividends, and other forms of profit made on the TFSA are not subject to tax.

Even when withdrawn, all contributions and income earned in the account are generally tax-free.

How to open a Tax-Free Savings Account (TFSA)

The Tax-Free Savings Account (TFSA) can be opened at any financial institution or a bank. As simple as it is, you should know what to do with your TFSA, some folks want to just use it as a simple way to save their money and just contribute to it at their rate. Others, would want the TFSA to be used to drive some investments for extra income! That is why it is essential that you contact a financial expert to help you build the right kind of TFSA for you and look into your different options.

Benefits of a Tax-Free Savings Account (TFSA)

You can save money with a TFSA and use it for investments and the growth of your savings is tax-free! If you earn interest, dividends, or capital gains in a TFSA, they are tax-free for the rest of your life.

Money can be easily taken out of your TFSA account at any time! In order to avoid reductions in your annual contribution amount, you can reinvest any money you withdraw from your account the following year for a tax-free withdrawal fee. Also, if you never had a TFSA then the contribute room in 2024 is $95,000 if you were 18 or older since the program began in 2009. So with a TSFA have complete access to save up a large sum of money and it will not be impacted by taxes.

Reason 1: Tax-Free savings to maximize growth

The Tax-Free Savings Account (TFSA) is a great way to maximize the growth of your savings. Many savings accounts have fees associated with them, there are taxes added to those fees as well which just means that even though there might be interest earned on your savings, there are taxes that need to be paid. These savings accounts are not the best way to maximize your growth in terms of interest, mutual funds, stocks, capital gains, bonds, or ETFs. Rather the best way for you to maximize your savings is by minimizing your taxes.

Luckily with the Tax-Free Savings Account (TFSA), banks cannot charge tax on any management fees or the income earned with any interest, mutual funds, stocks, capital gains, bonds, or ETFs also is not taxable income. This account is legitimately a Tax-free and tax-sheltered account which will minimize the fees associated with it.

Reason 2: Your contribution room grows every year

The contribution room in your TFSA grows every year which means the government allows a certain contribution amount to be deposited into your TFSA every year. If you are someone who is already actively contributing to your TFSA then this is beneficial because you can add more money year to year to your TFSA. If you are someone who still hasn’t opened a TFSA this is even better news, this means that your cumulative contribution room could be extremely high, and completely tax-free. What this means is that since its creation in 2009, the Tax-Free Savings Account (TFSA) contribution room is in line with the age that you turned 18 years old, so if you were 18 years old or over in 2009 then you currently have a cumulative total of $95,000 in contribution room in your TFSA.

Some years allow for higher contributions than others, but either way, this contribution room is a wonderful aspect to consider when opening a TFSA. To find out your contribution room, find out the year that you turned 18, and add up the amount of contribution room per year from that year. For example, if you turned 18 in 2015, then you just add up the annual contribution limit per year from 2015 onward. Therefore, if you turned 18 years old in 2015 then your cumulative total contribution limit is $50,500

Below you can find the table of how much the government has allowed as contribution room per year since the inception of the TFSA:

| Year | TFSA Annual Contribute Limit | Total TFSA Limit (Cumulative) |

|---|---|---|

| 2009 | $5,000 | $5,000 |

| 2010 | $5,000 | $10,000 |

| 2011 | $5,000 | $15,000 |

| 2012 | $5,000 | $20,000 |

| 2013 | $5,500 | $25,500 |

| 2014 | $5,500 | $31,000 |

| 2015 | $10,000 | $41,000 |

| 2016 | $5,500 | $46,500 |

| 2017 | $5,500 | $52,000 |

| 2018 | $5,500 | $57,500 |

| 2019 | $6,000 | $63,500 |

| 2020 | $6,000 | $69,500 |

| 2021 | $6,000 | $75,500 |

| 2022 | $6,000 | $81,500 |

| 2023 | $6,500 | $88,000 |

| 2024 | $7,000 | $95,000 |

Reason 3: Access your money anytime

Many savings accounts such as the LIRA (Locked-in retirement account) and the RRSP (Registered retirement savings plan) are savings accounts that have some penalties and conditions if you withdraw from them. With a TFSA, you don’t need to worry about any penalties or conditions when you withdraw your money. The only thing to keep in mind is if you have reached your total contribution limit then you can’t deposit that money back in until the next year. This is a minor complication but this isn’t as impactful as some of the complications when withdrawing from an RRSP.

The money in your TFSA is yours and you are totally free to access it whenever you want. This makes the TFSA a great emergency savings account or rainy day fund. When accessing your TFSA remember to ask your bank what their policies regarding their TFSA account is. Although they won’t charge you for withdrawing from your TFSA, there are fees such as management fees, or possible losses from investments.

Reason 4: Use your Tax-Free Savings Account (TFSA) as an investment vehicle

One of the most beneficial parts of the Tax-Free Savings Account (TFSA) is the fact that you can use the TFSA as an investment vehicle. Banks will encourage you to put the money in your TFSA to use by investing it in guaranteed investment certificates (GICs), bonds, stocks, exchange-traded funds (ETFs), mutual funds and options. These are some lucrative ways to earn some income in your TFSA account. By the way, another amazing thing about the TFSA is that your gains and income earned will not be taxed, plus management fees and investment fees cannot be taxed either.

If you aren’t a risky investor the best thing to do is combine your TFSA with a GIC or try to get a TFSA with a high-interest rate, this way you can sit back and not worry about any fluctuation in your account, rather it will just grow steadily. Whatever is the best fit for you, there are multiple options available for you to choose from so that you can earn some income from your TFSA.

The table below showcases the tax impact on investment gains on a non-registered savings account compared to a Tax-Free Savings Account (TFSA)

Reason 5: A savings account to complement your existing savings accounts

The Tax-Free Savings Account (TFSA) is a brilliant way to diversify your savings. If you are someone who already has a Registered retirement savings plan (RRSP), then the TFSA is definitely somewhere where you should deposit your refund from your RRSP. If you don’t have an RRSP, this is fine, the TFSA is actually aimed towards those who have a lower income anyways. This TFSA is a brilliant way to have a secondary savings account that can be used for investing or even just simply have tax-sheltered savings. You can also make as many TFSA accounts as you want, although you must be aware of your own contribution limits and room, it can be useful to make more than one TFSA for different savings goals.

Reason 6: Re-contribution room

The re-contribution room is a great reason why you should open a TFSA. This re-contribution room makes sure that you are allowed to keep your cumulative contribution amount always. If you are to withdraw money from your TFSA, that money can be deposited again if you have an available contribution room. If you do not have contribution room for the year since your TFSA is already maxed out, then you can simply put the money in the TFSA next year once the contribution amount is increased. This makes the TFSA a low-maintenance and low-commitment account if you decide to use it for the odd withdrawal. The re-contribution room is useful for returning your TFSA to the amount that it originally was, and every year you can deposit the previously withdrawn money and the contribution limit of the year will not count your re-contribution.

Reason 7: Designate a beneficiary

A unique feature about the TFSA that really stands out from other savings accounts is the fact that you can designate a beneficiary in the event of your death. The beneficiary will be granted the account and all of the holdings including the income that was earned in the account from the time of the death of the original account holder to the settlement of the estate. All of the transferred funds from the account will not affect the beneficiary’s contribution limit either. Be wary of any over contributions made by the original account holder because this can lead to a 1% tax per month for the overage amount.

Along with designating a beneficiary, it is important that you have a will to protect your estate, and to continue to protect your loved ones after you pass. To learn more about why it is important to have a will read the top 11 reasons to have a will in Ontario.

Frequently Asked Questions (FAQs) about Tax-Free Savings Accounts (TFSA)

Yes! Tax-Free savings accounts are safe and a product offered by legitimate and credible financial institutions in Canada. The TFSA is one of the safest options for saving money for both short and long-term financial plans. They have non-tax-deductible features which make the amount in your TFSA safe and secure from taxation. The TFSA is one of the best options for all Canadians to make for a safe and secure way to save.

To be eligible to open a Tax-Free Savings Account (TFSA) in Canada, you must be a Canadian resident who is over 18 years of age, and you must have a valid Social Insurance Number (SIN). A non-resident of Canada who has a valid SIN is even eligible to have a TFSA but they will be subject to a 1% for each month their contributions stay in the account.

A TFSA is simply a savings account. With that being said, it is up to you if you want to just put money aside in it and leave it at that, or if you want to pair it with various forms of investments that can provide growth, and have different levels of direction (investments managed by your or by your financial institution).

No, currently you can’t have a joint TFSA. One person can only hold A TFSA, therefore you and your spouse can open your own individual accounts.

Yes, the only requirements to open a TFSA are to be over 18 years of age and have a valid social insurance number.

No, currently you can’t have a joint TFSA. One person can only hold A TFSA, therefore you and your spouse can open your own individual accounts.

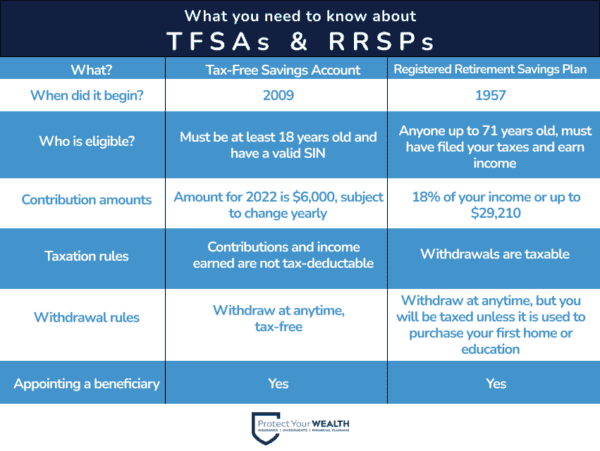

Here is a comparison to give you some basic information about TFSAs and RRSPs:

Yes, you can lose money on a TFSA, but it is easy to avoid losing your money. Typically, people who lose their money on a Tax-Free Savings Account are people who are using it for more volatile investments or people who are over-contributing. With high-risk investments, it is possible that you will lose money in your TFSA but this is based on your risk tolerance and you can avoid it by purchasing a low-risk investment instead of going with a GIC. On the other hand, if you’re over contributing to your TFSA you will be taxed at a rate of 1% for every month that there is an over-contribution in your account.

This breaks down to the yearly contribution amount, as well as the cumulative contribution amount.

- Cumulative TFSA room

- This all depends on what age you were in 2009. If you were age 18 or older in 2009, then in 2024, the contribution limit for the Tax-Free Savings Account (TFSA) in Canada has increased to $7,000, up from $6,500 in 2023. This means that if you have been eligible for a TFSA since its inception in 2009 and have never contributed, your cumulative contribution room would be $95,000 as of 2024

- Yearly TFSA room

- You are only eligible for a certain amount of contributions in your TFSA yearly, this amount can change year by year. For 2024, the annual contribution limit for the Tax-Free Savings Account (TFSA) is $7,000. This increase from the $6,500 limit in 2023 allows for a greater amount of tax-free savings. If you do not contribute the full $7,000 in 2024, or if you make withdrawals, the unused contribution room will carry over to the next year. This means that you can make up for missed contributions in subsequent years. Please refer to our graph to see the yearly contribution amounts since 2009.

The TFSA total contribution limit for 2023 is $7000.

The TFSA total lifetime limit for 2024 is $95,000. For 2023, the TFSA total lifetime limit was $88,500.

Wondering if the Tax-Free Savings Account is right for you?

No matter what your financial situation or financial goal is, whether it be short-term savings or long-term capital growth from investments, the Tax-Free Savings Account is an excellent option for saving. The top benefits of the TFSA include but are not limited to tax-sheltered growth, growing contribution room, access to your money anytime, investment possibilities, re-contribution room and designation of a beneficiary. If you want to learn more about the Tax-Free Savings Account check out our TFSA page which has answers to all of your questions about TFSAs.

At Protect Your Wealth, we’ve been providing expert advice for all types of life insurance, and retirement and investing planning, since 2007. As your Life Insurance broker and financial planner, we work with you to create a personalized plan for your family or business that covers and meets your needs.

Contact Protect Your Wealth or call us at 1-877-654-6119 to talk to an advisor today. We’re proudly based out of Hamilton, and service clients anywhere in Ontario, including areas such as Guelph, Kitchener, and Barrie.

![Top 5 Best Disability Insurance Companies in Canada [2024]](https://sp-ao.shortpixel.ai/client/to_webp,q_glossy,ret_img,w_500,h_383/https://protectyourwealth.ca/wp-content/uploads/2022/12/Top-5-Best-Disability-Insurance-Companies-500x383.png)

{kind=link}

Leave A Comment