Disability Insurance in Canada Guide

What is disability insurance? Do you need it?

12 Minute read

Originally published: Dec 14, 2021

Updated: July 14, 2023

Disability Insurance in Canada Guide

What is disability insurance? Do you need it?

12 Minute read

Originally published: Dec 14, 2021

Updated: July 14, 2023

What happens if you suddenly lose the ability to work? As with anything, it’s not completely out of the picture. Disability life insurance provides a safety net in the event that something does cause you to be unable to work.

Imagine this:

You’re about to start a new chemical engineering job at a major pharmaceutical firm in Hamilton, Ontario. You’re excited about this opportunity; you’ll be making more than you were at your previous company and the benefits package is especially generous.

Your only question is whether the disability insurance in the package is really necessary, especially since you’re in your mid-30s, physically fit, and drive carefully. It’s expensive, and you’re married with two young children. Wouldn’t that money be better used to grow college funds or invest in house repairs?

So, you opt out of it. A few years later, you are diagnosed with a serious heart condition and can no longer work.

Without disability insurance to compensate for the lost income, you are forced to sell your home, move your family into an apartment, and borrow from your parents when emergency expenses arise.

The few thousand dollars a year that you tried to save by opting out of disability insurance can’t even begin to compensate for the unprotected loss of a $175,000 salary.

Your ability to make a living is your most valuable asset. Without it, you can’t maintain your home and car, send your kids to college, or fund a retirement plan. Ergo, you need to ensure it just like you would anything else of immense value. This is where disability insurance comes in.

In this article:

- What is disability insurance in Canada?

- Benefits of disability insurance

- What is the best type of disability insurance?

- How much disability insurance coverage do you need?

- What is not covered by disability insurance?

- How much does disability insurance coverage cost?

- At what age should you drop disability insurance?

- Who are the best disability insurance providers?

- Frequently Asked Questions (FAQs) about Disability Life Insurance

What is Disability Insurance?

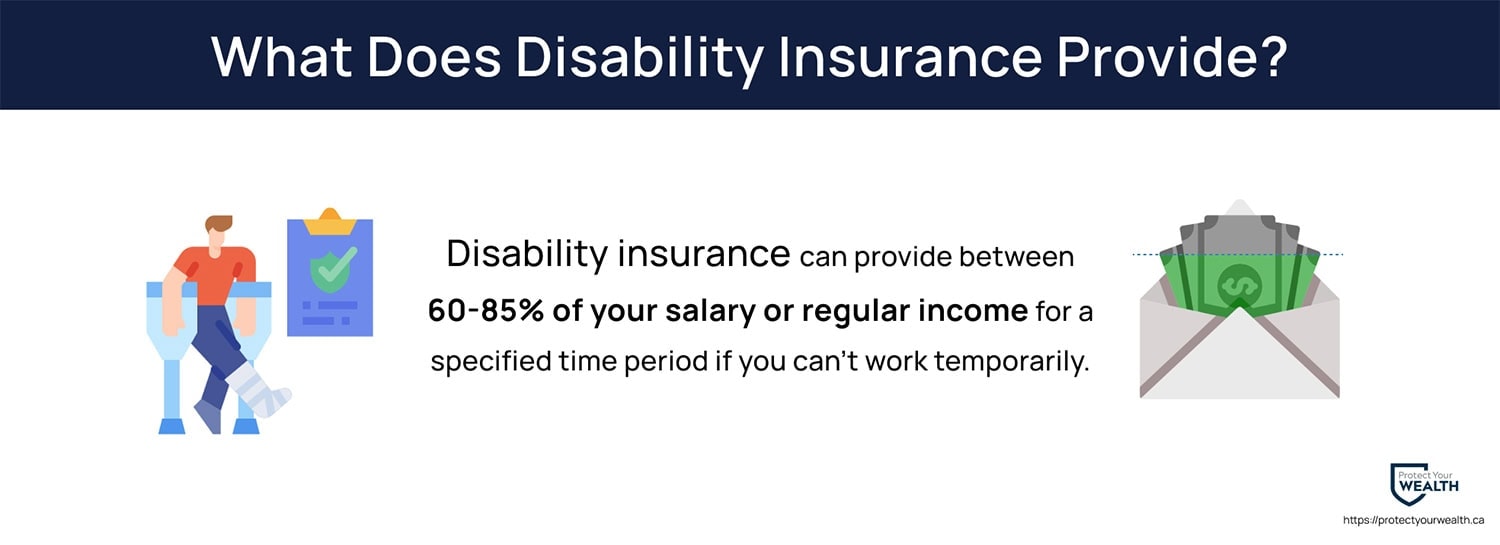

Disability insurance pays a portion of your income if illness or injury leaves you unable to work for an extended period of time. It can give you tax-free monthly income to help pay expenses if an illness or accident stops you from working. It doesn’t matter how you make your living- full-time, part-time, self-employed, freelancer- if you rely on a paycheque, protecting your income stream is one of the best decisions you can make.

Although you naturally hope that disability won’t happen to you, statistics suggest that it’s smart to take precautions. For example:

- The average 30-year-old Canadian has a four times greater chance of becoming disabled than they do of dying before age 65.

- One in six Canadians will be disabled for at least three months before they turn 50.

There are two primary policy options that cover incidents or illnesses: long-term disability and critical illness. Both types cover you financially if you become disabled or ill, but there is a difference between the critical illness and disability insurance. Notably, disability pays a monthly income while critical illness insurance provides a tax-free lump sum amount after you’ve been diagnosed with a covered illness.

Benefits of Disability Insurance

When you invest in disability insurance, you and your dependents have peace of mind knowing that income flow will continue during the period when you are unable to work. These policies will cover you for one of the following:

- Any occupation: You are protected if you are unable to perform any kind of work, even a less-demanding job.

- Own occupation: You receive payments if your disability prevents you from working at your regular job. Many employers and private insurers offer ‘own occupation’ coverage for the first two years of disability and switch to ‘any occupation’ after that.

Depending on the policy, some disabling conditions that are unrelated to illness or injury may be covered. One common example is serious complications arising from childbirth.

These benefits are usually paid for up to two years if you can’t do your regular job but if you are unable to work at all, the payments could potentially continue until you are 65.

What is the best type of disability insurance?

There are two main types of disability insurance. Both pay a benefit that replaces a percentage of your income, but they work differently because short-term financial needs differ from long-term ones.

Short-term disability insurance

Most disabilities don’t keep you out of the workforce longer than a year. Short-term disability insurance, or STD, is designed to provide you with an income while you take time off to recover from illness or injury. Depending on the policy you take out, you can collect benefits for up to six months and even take advantage of resources that help you return to work sooner.

Long-term disability insurance

There are some disabilities that are more severe and can even be permanent. Long-term disability insurance, or LTD, is for these situations because the benefits can last for years. It is often purchased as an individual policy by higher-income business owners and professionals who want to protect their lifestyle if they are no longer able to work.

Who is eligible for disability insurance in Canada?

Most providers will cover Canadian citizens and permanent residents / landed immigrants between the ages of 18 and 55 who work a minimum number of hours per week. You may still be eligible even if you have a pre-existing condition, but it may be excluded from your policy.

How much disability insurance coverage do you need?

The key is to have enough coverage to meet your living expenses, which include food, hydro, rent, transportation, taxes, and your rent/mortgage. For some people, this means at least 60% of your regular pre-tax income while those who don’t have children or who have paid off their mortgage could get by on 40% to 50%.

Bear in mind that most disability policies have a benefits cap, such as 65% of your gross income, but only up to $3,000 a month. If you’ve been earning over $70,000 a year, this coverage may be insufficient. In this case, you may want to look into a private disability policy to supplement the benefits offered by your employer.

What is not covered by disability insurance?

Not all conditions are covered by disability insurance. They include serious illnesses like cancer or a history of experiencing heart attacks. If you are approved despite having a pre-existing condition, it will probably be listed as an exclusion on your policy. Common exclusions include:

- Opportunistic illnesses characteristic of HIV or the AIDS virus

- Subjective conditions like chronic fatigue syndrome, fibromyalgia, and Epstein Barr syndrome

- Psychiatric or psychological disorders (unless they were caused by head trauma, a stroke, or a similar condition)

What you should know before you buy disability insurance

When you’re investigating options for disability insurance, you’ll want to take the following factors into account.

- How much is the benefit? With most insurers, the amount rarely exceeds 66% of your gross annual income.

- How long is the waiting period before benefits begin? Depending on the policy, you may have to wait 0 days, 30 days, 60 days, 90 days or 180 days.

- How long are benefits paid? Typical terms are two years, five years, and to age 65.

Disability insurance riders to consider

While you’re reviewing the various disability insurance policies, you’ll notice that there are a number of optional add-ons to choose from. Known as riders, they add to the overall cost of your premiums but let you customize your policy to suit your individual needs.

Examples include:

- Cost of Living: Your disability benefit is later increased by a percentage (normally between 3-8%) or based on the consumer price index (CPI).

- Future Insurability Option: You can purchase additional insurance in the future without having to qualify first.

- Return of Premium: You receive a refund of 50% of your premiums approximately every seven or eight years if you are not disabled and your claims have been minimal.

How much does disability insurance coverage cost?

Generally speaking, you can expect to pay between 1-3% of your yearly income in premiums, but the actual cost of your disability insurance policy will depend on factors like the following:

- Age: The older you are, the higher your premiums are likely to be due to an increased risk of experiencing a disability.

- Gender: Women have historically filed more disability claims and, once benefits start coming in, stopped working for longer than men. As a result, insurance rates for women can be substantially higher.

- Health: Your recent medical history can have an impact on how much you pay. If you have more health problems, you’re more likely to have higher premiums.

- Occupation: Those who work in a high-risk occupation may have to pay higher premiums.

- Smoker status: If you smoke, your premiums are guaranteed to be higher.

At what age should you drop disability insurance?

If you have disability insurance, a good rule of thumb is to maintain it until you retire. In general, 65 is the maximum age insurance companies will allow coverage, although some will cover you until age 70.

Who are the best disability insurance providers?

Three of the top disability insurance providers in Canada are listed below, along with an outline of their offerings.

RBC Insurance

Founded in the 1960s, RBC Insurance is the largest bank-owned insurance organization in Canada. It provides insurance products to over five million people, including short and long-term disability insurance.

- RBC Simplified® Disability Insurance: Recommended for self-employed individuals, contractors, and part-time or seasonal workers that work a minimum of 30 hours a week, between the ages of 18 and 55. If you become disabled, it pays benefits for up to two years. Optional illness coverage is available. No medical exam is necessary.

- The Professional Series® Policy: If you are a high-income executive or work on a fee-for-service basis (e.g. doctor or lawyer), this policy covers professionals aged 18-60. Depending on the terms, you can receive benefits for two years, five years, or until age 65. Total, partial, and residual disability are all covered.

- The Foundation Series™ Policy: If you are between the ages of 18 and 60, own or manage a small business, have a trade (includes farming), or are a middle-income earner, the Foundation Series™ policy pays total disability benefits for two years, five years, 10 years, or until age 65.

- Bridge Series® Policy: This product is aimed at the same demographic covered by the Foundation Series™ policy but pays total disability benefits for two years, five years or until age 65. Special underwriting guidelines are in place for farmers.

- The Fundamental Series™ Policy: This policy provides most employees and professionals with total or partial disability coverage and pays benefits for two years (illness coverage), five years, or until age 70. A medical exam is required for illness coverage only.

- Quantum: This product protects the same demographic as the Professional Series® Policy when an illness or injury reduces your ability to work and causes at least a 20% loss of earnings.

You can read our full review on RBC Insurance and their products here.

Canada Life

Founded in 1847 as the Canada Life Assurance Company, Canada Life was this nation’s first domestic life insurance company. Today, it provides disability insurance products and services in Canada, the United Kingdom, Isle of Man, Germany, and Ireland.

Canada Life’s disability insurance product helps to replace your income and cover your expenses if injury or illness keeps you from maintaining gainful employment. Premiums range from 1-9% of your salary and you’ll receive benefits until age 65.

- Lifestyle Protection Plan: This policy is conditionally renewable every year until age 65 as long as you continue to work full-time.

- Independence Plan: Available to a wide range of professionals, the Independence Plan pays a monthly benefit until age 65 if you become totally disabled and up to nine months of benefits during periods of partial disability. Base coverage is for injury only, although there is an optional sickness rider available.

- Overhead Expense Plan: If you own a business, this plan provides overhead expense protection should you become totally disabled. It is renewable until age 65 if you continue to work full time and have an ownership interest in the business.

- Buy/Sell Plan: This plan acts as a funding mechanism for a buy/sell agreement if one of the business owners becomes totally and permanently disabled. Premiums remain level until age 65.

You can read our full review on Canada Life and their products here.

Manulife

Manulife started in 1887 as the Manufacturers Life Insurance Company. Today, it provides disability insurance solutions to individuals, groups and institutions across the world. Available products include:

- Proguard Series®: Designed to help executives and professionals replace their income in the event of illness or injury, the Proguard Series® provides coverage to age 65 with no rate increases or reduction in benefits as long as premiums are paid on time.

- Venture Series®: This Manulife product provides income protection for small business owners and employees up to the age of 65. Every year, your policy amount automatically increases by 3% to ensure that you get the coverage you need.

- ExpenseComp®: If you own a small business, ExpenseComp® disability insurance covers expenses like salaries, benefits, and rent. Coverage is available until age 65 and you can convert your policy to an income replacement plan if you no longer need protection for business expenses.

You can read our full review on Manulife and their life insurance products here.

Frequently Asked Questions (FAQs) about Disability Life Insurance

Term life or permanent life insurance policies do not cover disability by default. You can add disability riders to many insurance policies to cover circumstances where you are injured or ill and no longer able to earn an income.

Your insurance costs will depend on several different factors, but in general, you can find most term life insurance policies available for less than $100 per month, whereas disability insurance policy premiums average 1-3% of your annual income.

You should look to have enough coverage to meet your living expenses, which include food, hydro, rent, transportation, taxes, and your rent/mortgage. For some people, this means at least 60% of your regular pre-tax income, but for those who don’t have children or who have paid off their mortgage may only need 40% to 50%.

Find a solution for what you’re looking for

Disability insurance is a lot like life insurance in that you hope you’ll never need it, but if your health takes a downturn, you’ll be glad you made the investment. Protect Your Wealth will help you identify and secure the disability insurance or critical illness protection coverage you need to create financial stability if your health takes a downturn.

To schedule a consultation about your income protection goals, or if you have any questions about disability insurance in Ontario or Canada, please contact Protect Your Wealth or call us at 1-877-654-6119 to talk to an advisor today! We’re proudly based out of Hamilton, and service clients anywhere in Ontario, Alberta and British Columbia; including areas such as Stoney Creek, Coquitlam, and Airdrie.

![TD Canada Life Insurance Review Canada [2024]](https://sp-ao.shortpixel.ai/client/to_webp,q_glossy,ret_img,w_500,h_383/https://protectyourwealth.ca/wp-content/uploads/2022/02/TD-Life-Insurance-Review-500x383.png)

![BMO Life Insurance Review Canada [2024]](https://sp-ao.shortpixel.ai/client/to_webp,q_glossy,ret_img,w_500,h_383/https://protectyourwealth.ca/wp-content/uploads/2022/01/BMO-life-insurance-review-500x383.png)

{kind=link}

Leave A Comment