·

·

")

What is a Registered Education Savings Plan (RESP)?

The Registered Education Savings Plan (RESP) program was introduced by the Canadian government in 1974 as an easy way for parents, grandparents, and guardians to save for a child’s post-secondary education.

The Registered Education Savings Plan (RESP) account is tax-deferred like the TFSA and RRSP. Which makes all capital gains, interest and income earned on the account protected by being tax deferred. This is ideal as the RESP account can include investment options like mutual funds, ETFs, GICs, stocks and bonds.

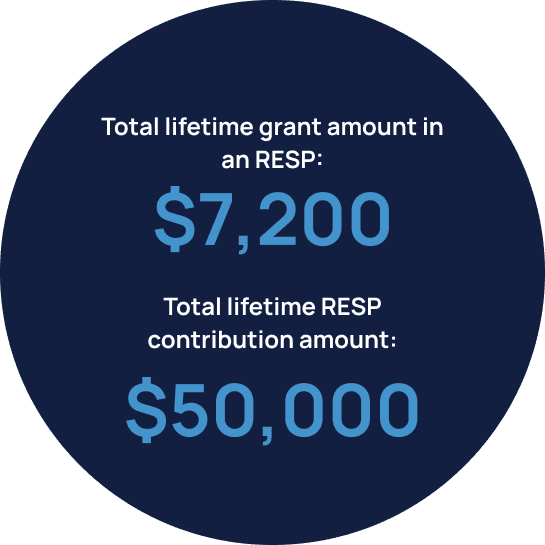

What makes the Registered Education Savings Plan (RESP) account so special is the Canadian government can pay you grants and bonds towards your child’s RESP account. The Canada Education Savings Grant (CESG) offers up to $7,200 in grants, while the Canada Learning Bond (CLB) offers up to $2,000 in grants for RESP accounts for children from low-income families.

Total RESP lifetime contribution:

$50,000*

*Per beneficiary

Grants available for RESP:

Canada Educations Savings Grant (CESG): Up to $500 per year

Canada Learning Bond (CLB): maximum of $2,000

How to open a Registered Education Savings Plan (RESP)?

Opening a Registered Education Savings Plan (RESP) is a simple process and it is an account that is offered by most major financial institutions in Canada. To find out if opening an RESP is right for you and to begin saving for your child’s education, please set up a free consultation with our financial advisors.

To open an RESP you must have:

- your Social Insurance Number (SIN)

- your child’s SIN

- the child’s birth certificate

What are the benefits of having a Registered Education Savings Plan (RESP)?

Setting aside money for your child’s post-secondary education is crucial, the RESP account is the best vehicle to make contributions, as it is tax deferred and can receive grants or bonds from the government to maximize growth to your savings.

A lifetime total contribution limit of $50,000 can secure your child’s future education plans and government program like the Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB) are government contributions that can help grow the savings yearly.

There is no yearly limit to how much you want to put into the RESP but it is worth putting in $2,500 yearly because the government will contribute 20% ($500) in grants that year. This is not mandatory, and you can claim up to $1,000 in grants per year, so if you cannot contribute $2,500 yearly to the RESP, there are still other ways to save and receive government contributions.

You can contribute to the RESP for a total of 31 years and the plan can remain open for 35 years! This is an ideal way to save for your child’s education even if they start later on, and this can be useful for those who have children pursuing post-graduate studies.

Benefits of opening a RESP:

The Canada Educations Savings Grant (CESG) and Canada Learning Bond (CLB) are great government contributions towards your RESP saving

Your savings are tax deferred, and can be withdrawn tax-free for post-secondary education payments

The RESP is flexible, as the account can stay open for up to 35 years

Essential financial investment that gives your child a financial head start in early adulthood

Financial Institutions we work with

We proudly work with Canada’s largest financial institutions for your retirement planning & investment needs

Financial Institutions we work with

We proudly work with Canada’s largest financial institutions for your retirement planning & investment needs

Frequently Asked Questions (FAQs) About Registered Education Savings Plan (RESP)

A RESP works by the sponsor of the plan (parent, family member, guardian) making contributions to the plan. The government then contributes 20% of the amount contributed by the sponsor, the maximum contribution the government will make per year is $2,500.

This is a beneficial account for those who want to save for their child’s education. This account is tax deferred, there are grants and bonds for the account, and it is flexible. It is a well rounded savings plan to save for a child’s education.

The Canada Education Savings Grant (CESG) is a grant that is provided by the government. This is the 20% that the government will contribute to the beneficiary of the RESP. This being said, the maximum CESG contribution the government will make is $2,500 per year. The Canada Learning Bond (CLB) is a bond that beneficiaries of low and middle income families are eligible to receive. For a family income of less than $45,916, the government will pay 20% on the first $500 contribution. This is a total of a 40% grant. For middle income families that make above $45,916 but below $91,831 they receive a government contribution of 30% yearly instead of just 20% yearly.

Wondering how much of a grant will be contributed by the government to your RESP based on family income?

| Grant | $45,916 and less | $45,916 to $91,831 | Above $91,831 |

|---|---|---|---|

| For the first $500 contributed | $200 | $150 | $100 |

| Grant on remaining annual contribution | $400 | $400 | $400 |

| Maximum grant (yearly) | $600 | $550 | $500 |

| Maximum grant (lifetime) | $7,200 | $7,200 | $7,200 |

The total lifetime grant amount that is eligible for an RESP is $7,200, this remains the same regardless of family income and includes the CESG and CLB benefits.

All you will need to have to open an RESP is your SIN card, the beneficiary’s SIN card, and the beneficiary’s birth certificate. RESPs are available at most banks.

Yes, you can make an RESP for more than one child. This really depends on who you make a RESP account for first. It is on a first come first serve basis therefore, whichever beneficiary has the RESP for first, will get the CESG benefit. If you want the RESPs to get the CESG benefit, you must start the RESP on the same date. This would then lead to the CESG grant to be split between the RESPs. You can also start a RESP family plan which will allow you to track the contributions made to each beneficiary. The annual CESG contribution remains as a lifetime limit of $7,200, and each individual RESP also has a lifetime contribution amount of $50,000.

The contribution limit is a lifetime total of $50,000 per RESP. There is no yearly limit to how much you can contribute. As stated previously, there is a maximum lifetime CESG contribution of $7,200 and there is a maximum CESG contribution of $2,500 in a year.

In most cases the financial institution where you’ve made a RESP account will automatically enroll you and you will be enrolled to receive grants within 6 to 8 weeks. This can vary depending on the financial institution, so it is always important to ask the financial advisors at your bank.

The B.C. government has introduced the B.C. Training and Education Savings Grant, a one-time $1,200 Registered Education Savings Plan (RESP) grant. If your child was born on or after January 1, 2007, he or she may be able to qualify for a one-time $1,200 deposit to a RESP after reaching the age of six. You don’t have to contribute to a RESP to receive it, but you must open one before your child turns seven.

The RESP is a great vehicle for investments, as it can allow you to invest in ETFs, mutual funds, stocks, GICs and bonds. The risk rates can vary and this is worth considering depending on the age of your child. To understand what investments are right for you it is important to contact a licensed financial advisor.

Although RESPs aren’t taxable when they are withdrawn for educational purposes, the income earned in the RESP through investments as well as grants is taxable. This being said, the withdrawals for post-secondary education payments are tax-free, but your child can be taxed when the money is in their account, this is not too concerning because students typically don’t pay too much tax, or don’t pay tax at all.

This money can be withdrawn by you but will be subjected to taxation, you will have to pay back the grants and a 20% penalty may be added as well. This amount can be transferred to another RESP as well, but it will only allow for a maximum of $7,200 in grants to one beneficiary, so be sure to track your RESP accounts.

The 5 Steps of Successful Financial Planning

An overview of 5 wealth-planning steps Protect Your Wealth takes that results in a strong financial future.

1.

Gather and AnalyzeAt Protect Your Wealth, we will work with you to create an accurate overview of your present financial situation. Using state-of-the-art software, we will complete a thorough needs analysis to assess your present expenses and project future ones while accounting for inflation. We also perform a detailed risk assessment to help ensure that you are not taking more risk in your investments than necessary.

2.

Develop Your Blueprint for SuccessAfter carefully considering all aspects of your finances and identifying ways to maximize tax efficiency, we will recommend an efficient retirement savings plan that tallies with your investment goals. You will receive a personalized Investment Policy Statement that summarizes our findings and recommends appropriate risk-managed investment options.

3.

Strategize and Implement Your PlanAfter you approve your Investment policy statement, we will present you with a Financial Planning Priorities and Strategies document outlines your financial planning priorities and your personalized wealth-building strategies that meet both your short, and long-term financial goals. Once you review and approve your plan, it will be implemented. It is important to note that this document will change over time to ensure that it always reflects your current circumstances and complies with any changes in government policy.

4.

Forecast Your Financial FutureWe use a cash flow planning analysis to create a financial forecast of your future. This analysis calculates projected outcomes, which lets you consider the consequences of financial decisions before you make them and create a stronger plan for future commitments like a child’s college fund. These forecasts are reviewed every year as your situation changes.

5.

Ongoing Monitoring and ManagementFinancial planning is a continuous process. To ensure that your investment needs continue to be met, we will remain in regular contact with you throughout the year and hold a yearly review to assess progress, make adjustments for changed circumstances, and evaluate promising new strategies. These meetings may be held in our office, by phone, or via Zoom.